THE WEEKLY TOP 10

THE WEEKLY TOP 10

Table of Contents:

1) The stock market: Bullish near-term, cautious for 2021.

2) Many global stock markets look great near-term as well.

3) One concern is that sentiment is starting to get quite bullish.

4) A break above 1% on the 10yr note will confirm a change in LT rates.

4a) That will be bullish for banks...not so much for utilities.

5) Bitcoin: More upside potential, but it will see more very deep corrections.

6) We see more upside potential for the energy stocks.

7) Gold...Sitting at a key near-term technical juncture.

8) Tesla...Don’t forget that volatility is its middle name.

9) 2021 earnings estimates are not enough to fuel a further rally.

10) Summary of our current stance.

Short Version:

1) We are still bullish on the stock market for a year-end rally. We believe that the Fed will keep the liquidity spigots wide open during this new waves of lock-downs, BUT we want to make sure we reiterate that we are much more cautious for most of 2021. Once we get past this most recent wave of the pandemic, we believe the Fed will lighten up on their stimulus (to avoid another major bubble)...and we think new fiscal stimulus (besides the upcoming relief package) will be back-end loaded in future years. With the stock market as expensive as it is, the lower levels of stimulus will create headwinds for stocks much of next year.

2) The liquidity that should be provided during this newest wave of lockdowns will not be isolated to the Federal Reserve. Other global central banks will also continue to do the same...which will help many overseas markets rally further as well. Looking at Japan, India and South Korea, they’ve already made nice “higher-highs”...and Germany, the UK and China are close to doing the same. Therefore, investors do not have to concentrate on the U.S. for gains going forward.

3) Even though we’re bullish on the short-term potential for the stock market, we do need to point out that sentiment is getting quite bullish...and if gets much more extreme, it will create a warning signal for the market. Sentiment polls like the II, AAII and DSI are either extremely bullish or getting close. Thus if sentiment becomes too extreme, we’ll turn cautious sooner than we’ve been thinking recently.

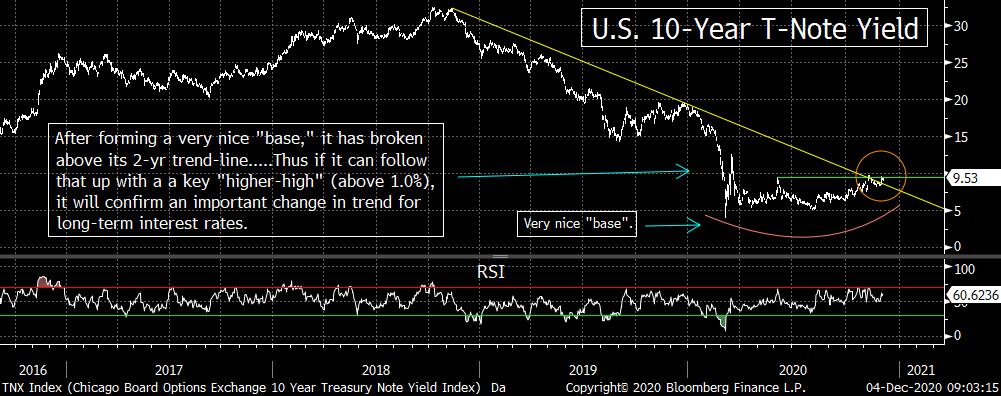

4) The yield on the U.S. 10yr T-Note stands at a key juncture. If (repeat, if) we see a break above 1.0%...that will take it above its trend-line from 2018 and give it a key “higher-high.” In other words, a move above 1.0% will confirm a very important CHANGE IN TREND for long-term interest rates!!! That should have an important impact on several equity groups in the weeks ahead.

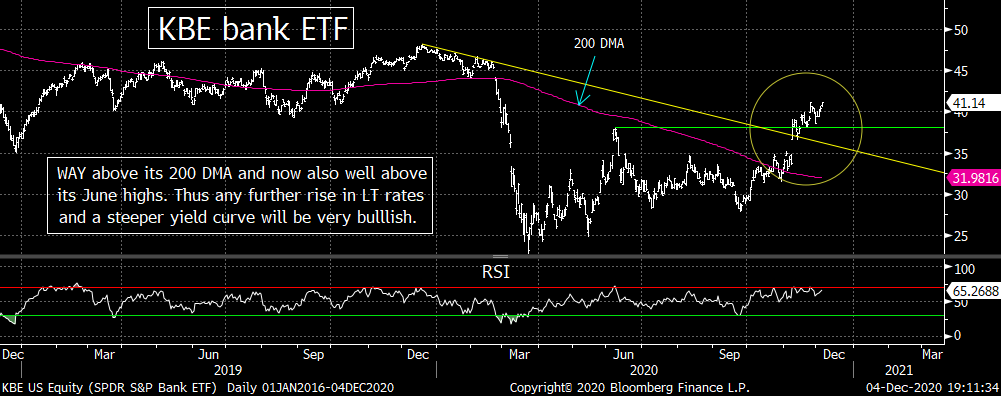

4a) A change in trend for long-term yields should be bullish for the banks stocks...and help them continue to rally further as we move through December. This will be especially true if the yield curve continues to steepen.....On the flip side, it will likely be negative for the utility stock...with the XLU testing two key support levels right now.

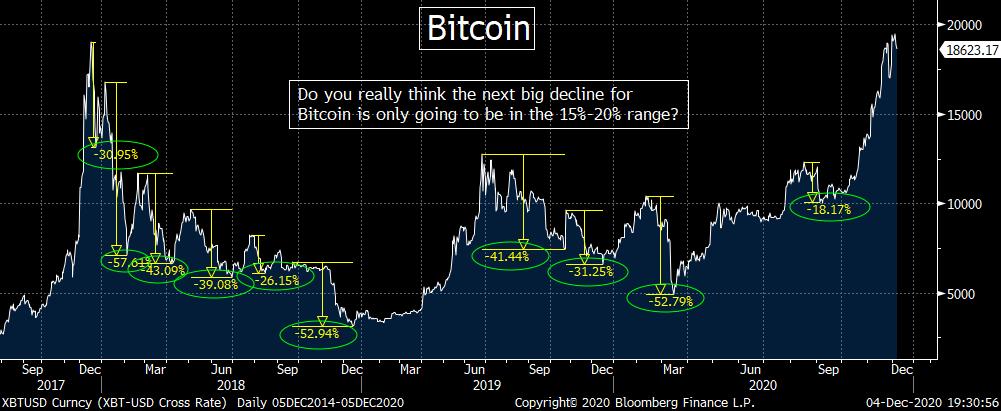

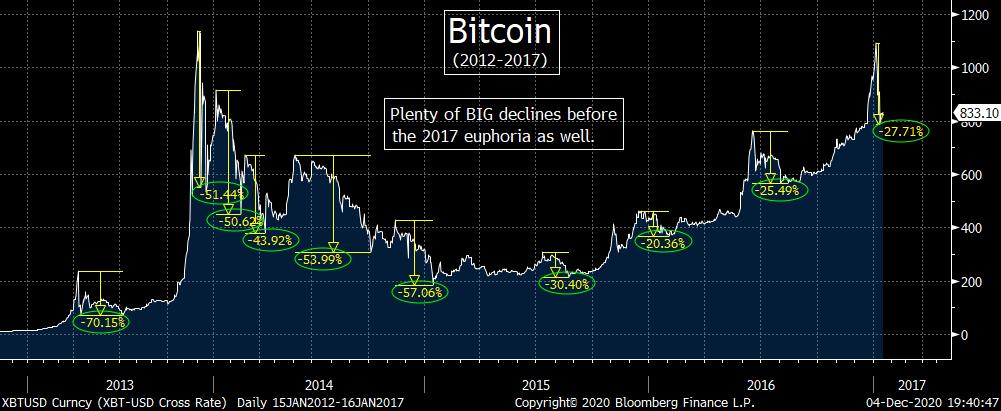

5) We are bullish on Bitcoin for the near-term and the long-term, but we’re cautious on the intermediate-term. It could/should reach $22k or so before it tops out near-term, but we believe that a lot more of the recent rally has been fueled by central bank liquidity than investors realize. Therefore, when the liquidity becomes less plentiful at some point next year, it should lead to another deep correction in Bitcoin. (Something it has seen 20 times since 2013.)

6) We think the energy stocks have more upside potential. Most people still hate this group, so its negative sentiment should help crude oil rally further. Also, both the XLE and XOP energy stock ETFs have broken slightly above key resistance levels. Therefore, if they can see anymore upside follow-through, it should give them even more momentum.

7) Our calls on gold continue to go well...as its drop below $1,850 did create another down-draft. However, it is now at a key juncture and thus whichever way it moves over the next week/10-days should be important. If it breaks back above $1,850, it’s going to be bullish...and if it fails, it will be bearish. We’re leaning towards the bearish side...thinking it will see one more decline before it bottoms...which is likely to be fueled by a near-term bounce in the oversold dollar.

8) Tesla should be able rally further over the near-term. Although it getting overbought, its weekly RSI usually moves above 80 before the stock tops-out. However, since it has seen 20 deep corrections since 2013, the odds that it will see another one at some point next year are quite high. In other words, more deep corrections are likely...even if the stock is going to go a lot, lot higher over the very-long-term.

9) We totally understand why people believe that the economy in 2021 will be A LOT better than has been in 2020...and that earnings growth next year will be A LOT better than this year as well....However, if you take away the “level of YOY growth”...and measure the absolute condition of the economy next year...and the absolute level of earnings in 2021...it is VERY difficult to argue that a justifiable earnings-based rally of substantial size can take place in the stock market next year...when those earnings estimates are no better than the actual earnings of 2018 or 2019.

10) Summary of our current stance.....The stock market is getting a bit overbought, but the RSI chart on the S&P 500 index is still below levels that have signaled tops over the past two years. Thus the S&P should rally further going forward...and the banks & energy (as well as some more speculative assets like Bitcoin and TSLA) should continue to outperform for a while. However, we believe that central bank liquidity will become less plentiful next year, so it will make this expensive stock market vulnerable to some more rough times. This is especially true given the fact that earnings are expected to be no better next year than they were in 2018 & 2019...when the stock market was trading a much lower levels.

Long Version:

1) In one of our “Morning Comments” this past week, we highlighted how several overseas markets were acting just as well (or even better) than the U.S. stock market. We will review those comments...and add some new ones to this issue in the next bullet point (#2). However, after speaking with one of the smartest people I’ve ever known on Wall Street, I realized that part of what I was saying could have led people to think that I had changed my view for 2021...and had turned quite bullish. With this in mind, we thought we’d review our stance on the market for most of 2021...because we are quite cautious about the market next year...even though we remain quite bullish on it for the near-term (next month or two). (Besides, it will be good to review our stance...given the fact that we did not put out a note last weekend due to the holiday.)

There are several reasons why we are cautious about 2021...even though we think this year-end rally might spill over into next year...but there are two that stand out to us. First, we believe that the Fed will begin to pull-in its horns a bit...early in the New Year. No, they will not completely turn off the liquidity spigots by any means, but we believe that as the cold weather season gets near its peak early next year, the Fed will turn the temperature down.

They should keep the spigots wide open for now...because they do not want this newest wave of the coronavirus (and the lock-downs that are going with it) to shut down the economy in a meaningful way. No, this new wave will not lock things down to the same degree that it did in the spring, but the given the MASSIVE amounts of corporate debt in the system, they want to work hard to limit the defaults that we’ll see next year. (Remember, the Fed’s focus right now is the credit markets, not the equity markets.) So the liquidity should keep flowing for a while...and the stock market should be an indirect beneficiary of that stimulus for a while longer.

However, the Fed also knows that the stock market is very expensive. It is now trading at 22x consensus forward earnings (for 2021). If they keep the pedal to the metal on liquidity, it will only push the stock market into bubble territory. (“Further” into bubble territory if you listen to some people.) With the formation of this massive corporate bond bubble, the Fed cannot afford to let another huge stock market bubble form. If they do, they will not be able to control the fall-out once it eventually and inevitably bursts.......Yes, they wereable to stabilize things after the tech bubble burst in 2000, but they were only able to do it by the skin of their teeth during the credit crisis in 2008...so they won’t be able to do it if it happens again (given the massive increase in the level of debt & leverage in the system since 2008).

Besides, they won’t need the stimulus next year as much as they have this year. Once we get past this newest wave of the pandemic, the weather will get warmer and the economy will re-open again. Also, when the weather finally turns colder once again (next fall), we should have the vaccines to combat it in a way that will avoid major lock-downs from taking place again........Therefore, as their stimulus becomes less essential, it should become less plentiful...and thus THAT will create some pretty strong headwinds for this very expensive market.

The second reason deals with politics. As we have said many times in the past, there is a REASON why the first year of a presidential cycle is usually a tough one for the stock market. (In other words, it’s not a coincidence.) The first year is tough because the new president tends to take care of the tough issues first...and they tend to back-end load their economic stimulus. This way, they can get the tough (but needed) issues done and out of the way...and then have the economy growing nicely in the 3rd & 4th years of the term...just as they begin running for re-election.

President Trump did not do this. He front-end loaded most things...and he did not get re-elected. The same is true for George HW Bush. In 1990, he broke his promise and actually RAISED taxes....just in time for the last two years of HIS term. Of course, he lost his bid for re-election...even though he had won a HUGE military victor just 12 months before (in the First Gulf War)!!!.......Ronald Reagan & Bill Clinton had recessions early in their first administrations...and George W. Bush and Barak Obama had to deal with bad bear markets early in their own administrations. However, in all four cases, the economy was doing well when they came up for re-election...and all four of them won.

Given these historical precedents...what do you think President-Elect Biden is going to do??? Even if he doesn’t run in 2024, he’ll want his legacy to be a good one. To insure that, he will want to make sure that the Democrats hold the White House four years from now. Therefore, it is our opinion that he’ll make some tough decisions in his first year. Through Executive Orders, he’ll raise the level of regulations in the U.S. This will create more headwinds for our economy and for our expensive stock market. Yes, he will also announce some big new spending plans...but even if they’re passed, they are very likely to be back-end loaded...for the reasons we just discussed. (They won’t tell us that the spending is back-end loaded, but that is almost certainly how it will play out.)

There are many other reasons to be concerned about next year...with U.S./China relations at the top of the list. There are also many items on the bullish side of the bull/bear ledger, so we cannot count-out a good year for stocks next year. However, since we believe that both monetary stimulus and fiscal stimulus will be much less plentiful than the consensus is looking for right now, we believe our (very expensive) stock market will become quite vulnerable at some point in the first half of 2021 (likely in the first quarter).

2) However we DO remain bullish for the rest of this year...and we do expect the rally to spill over into early next year as well. That said, the rally will likely not be isolated to the U.S. The simple reason for this is that it has not been isolated to the U.S. since March either...and many/most of the global stock markets are being helped by the massive stimulus being provided by the global central banks. We will look at the longer-term (2021) picture for these markets next weekend.

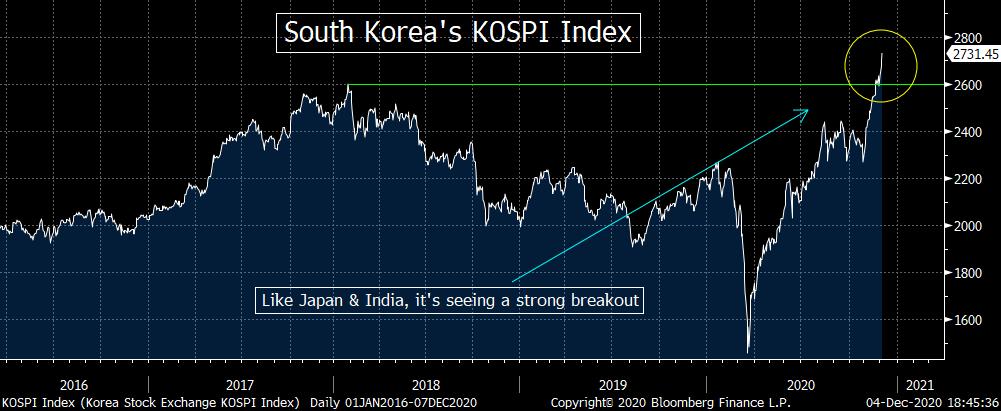

However this weekend, we’d like to focus on the technical picture for several of the key global market for the next 4-8 weeks...and the picture is a bullish one. The markets in places like Germany, the UK, South Korea, China, and India are all testing key resistance levels. (We’d also note that the stock markets in Japan and India have already broken above their own key resistance levels. This now has Japan’s Nikkei index trading at a 30-year high...and has India’s SENSEX index trading at all-time highs!!!)

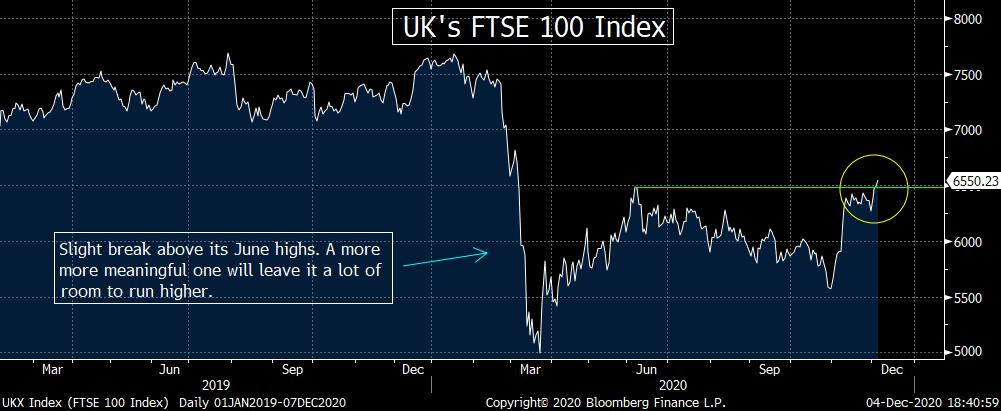

To be more specific, the German DAX has rallied slightly past its September highs...giving it a nice “higher-high.” (This was important because it made a “lower-low” in November, so the fact that it was able to avoid following that up with a “lower-high” is positive.) The DAX is still below its all-time highs from February, but if the break above its September highs becomes a more meaningful one, it will make a test of those old record highs soon quite likely.....As for the UK, it is bumping up against its June highs. Given all the issues surrounding Brexit, this market is still well below its February highs, but the most recent problems they’ve face did not keep their stock market from rallying in November...and if it breaks those June highs (giving it a key “higher-high”), it’s going to leave it with some room to run.

In Asia, China’s Shanghai index, it is bumping up against its 2020 highs (from July)...and very close to its early 2018 highs as well. Therefore, if (repeat, IF) their market can see some more upside follow-through over the coming weeks, it’s also going to be quite bullish for this important global stock market on a technical basis as well......South Korea’s KOPSI index has broken meaningfully to new all-time highs. Japan’s Nikkei Index, and India’s SENSEX Index have both done the same. Therefore, they might have to pull-back a little bit over the short-term. In other words, any “breather” we see from time to time over the next month or so in Japan & India could take a bit longer than it could be for other markets near-term. Therefore, they might not provide the same kind of short-term opportunities the other markets could/should provide.)

Either way, our main point is that as strong as the rally has been in the U.S. market, there are many other opportunities in other parts of the world as well. Therefore as investors and traders are looking for opportunities to maximize their performance for 2020, they should not be looking solely within the U.S. borders. They should be looking overseas for opportunities as well

3) Of course, even though we’re still quite bullish on the stock market for a year-end rally (and slightly beyond), it is essential that we keep a close eye out for signs that the stock market will top-out sooner than we’re expecting. One fly in the ointment right now is sentiment. It is getting quite bullish. Bullishness is not bad at all for the stock market...UNTIL it starts to get extreme. When that happens, its leaves too many people on one side of the boat...and it makes it difficult for the market to rally a lot further. (There’s simply fewer people left to buy, buy, buy.) This is why the rally in December is unlikely to be as strong as it was in November, but we also have to be wary of any signs that it will actually top-out soon.

First of all, the sentiment reading in the Investors Intelligence data shows that bullishness has risen to 64.8% among financial newsletter writers. That’s even higher than the 61.5% number we got in early September (just before the S&P dropped 11%) and also more than the 61.8% reading we saw at the beginning of Q4 2018 (just as a 19% drop in the S&P 500 was beginning).

We’d also note that the AAII data for individual traders shows that bullishness is at 49%. That’s slightly below its recent highs from two weeks ago, but the 8-week moving average (of 42.5%) is the highest level we’ve seen since the very beginning of 2018....On top of this, the “Dumb Money Confidence” reading put out by “Sentiment Trader” shows that bullishness is the highest they’ve ever since. (Their data goes back to 1998.).....Finally, the Daily Sentiment Index data shows that bullishness among futures traders has moved just above 80%. That is not a major extreme, but it still shows that bullish sentiment is getting strong.

The point is that sentiment is getting quite bullish. Sentiment can remain bullish for a while before the market actually rolls-over...especially when the central bank liquidity is plentiful...but it does tell us that our 3,800 target level on the S&P 500 might not be exceeded by much. This is only a small crack in the bullish foundation, but if it grows, it will be something that will lead us to become cautious sooner than we’re thinking right now.

4) The bond market......Friday’s employment report was weaker than expected, but the bond market did not rally. Instead, it sold-off...which, in turn, led 10-year yields to rise within a whisker of their November highs...and very close to 1.0%. Some of this unusual reaction to weaker-than-expected economic data seems to have taken place because the market believes that this number will get Congress to move more quickly on the Covid relief package......Whatever the reason for the surprising reaction to the weaker data, the yield on the U.S. 10-Year note is now closing in on the all-important round number of 1.0%. However, this 1.0% level for the 10yr Treasury note is much more important than just a round number. A meaningful move above that level will take it above two VERY important resistance levels. Therefore, if (repeat, IF) that takes place, it will be a very important development.

Ok, let’s look at the chart, but we want to set up the entire picture...so let’s step back a little bit and look at it from a multi-year angle. First of all, the yield on the 10yr note formed a very nice “base” on its long-term chart during the spring and summer months...by bouncing around in the 0.5%-0.7% range for six months. It did spike up to 0.95% in June for a few days, but immediately rolled back over and fell back within that range. Even though it failed to breakout of that range in June, the fact that it did not drop below that sideways range over the next few months showed that it was still building a nice “base” (and thus not breaking down...and dropping towards zero).

As we moved past Labor Day, the yield on the 10yr note began to rise again...and tested the top-end of the above-mentioned range. More recently, it has again broken above that sideways range. This time, instead of rolling back over very quickly, it has held above the range for the past 4-5 weeks. The fact that it has held above the 0.7% level for several weeks raises the odds that the breakout is sustainable...and gives it more upside potential.

Of course, it is important to see a “meaningful” break above the 1.0% level before we can say that a breakout is taking place. Therefore, if it ticks at 1.02% or something like that, we won’t get too excited. However, a material move above that round 1.0% will do the trick. We’re not there yet...and, as always, we HAVE to wait for that “meaningful” break before we can get too excited about the development. However there is no question that the “set up” we’ve seen over the past 6-9 months...AND over the past 4-5 weeks...is very constructive for an upside breakout in yields before long.

We believe that a move above 1% would be even more important than most people realize. A move above 1.0% will not just give it a nice “higher-high”...but it will also take the 10yr yield significantly above its trend-line going back more than two years!!! All of this would be taking place AFTER it had built up a very nice base for many months. Therefore, it would be a very compelling event. In other words, if (repeat, if) we see a break above 1.0%...one that holds for more than a few days...it will confirm a very important CHANGE IN TREND for long-term interest rates!!!!!

Some people will argue that a change in trend for interest rates will be negative for the broad stock market...while others will say it would be quite bullish. (The majority would probably said it would be bullish.) Either way, it WILL have important implications for interest rate sensitive stocks, so we will be watching how things develop in the Treasury market over the coming days and weeks like a hawk.

4a) The two groups that would stand out the most from an important change in trend for interest rates would be the bank and the utility stocks. We’ll start with the bank stocks. We turned much more bullish on this group several months ago (after years of remaining cautious on it). The KBE bank ETF has rallied a whopping 45% since just late September (and +77% since the March lows). This allowed the KBE to break above its trend-line from late 2019...and move significantly above its June highs (giving it a key “higher-high”). Therefore, if longer-term yields continue to rise any time soon, its should create an even stronger leg higher for this group into the end of this year and early next year.

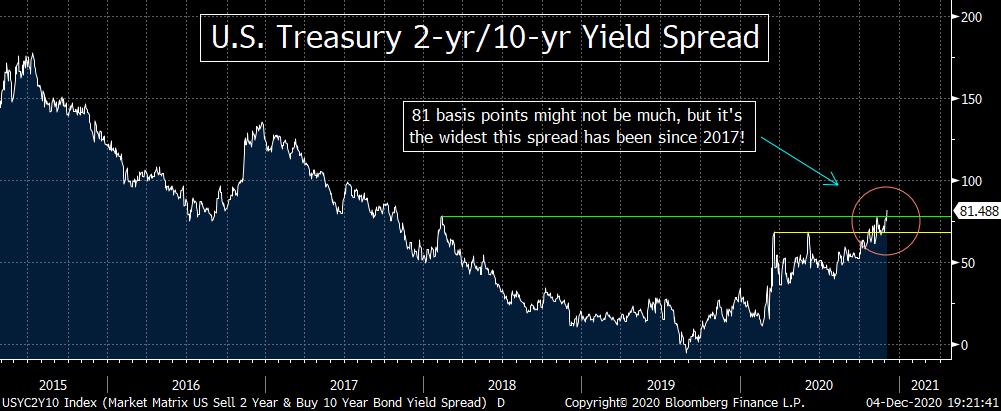

(We’d also note that the yield curve also continues to steepen. The U.S. 2yr/10yr spread has widened out to 81 basis points. That might not sound very steep, but it’s the widest spread we’ve seen since 2017! Thus this is another reason to think that the bank stocks can rally further going forward.)

However, this rise in rates is having a negative impact on the utility stocks. The XLU utility ETF has broken slightly below its trend-line from March...and is very close to making its first “lower-low” since the spring as well. So if it sees much downside follow-through in the coming days and weeks, it’s going to be negative for this group on a technical basis.

5) Bitcoin continues to get a lot of attention...and rightfully so. It’s almost 300% rally off of its March lows has everybody talking about it once again. It’s euphoria is not as extreme as it was in late 2017...and there are a lot of reasons to think that the cryptocurrency will head a lot higher over the very-long-term. In fact, there are a lot of reasons to think that it will continue to rally further over the very-near-term as well. (We have been calling for a rise to the $20k-$22k level in recent weeks.)

Not only are there several reasons to think that Bitcoin could/should rally further...but there are also (obviously) several reasons why it has already rallied so strongly since March. However, one of those reasons why it has rallied so strongly is not being talked about (at all) by the Bitcoin bulls...and we’re afraid that their inability to acknowledge this one “reason” will cause many of them to get clobbered at some point next year.

The reason we’re talking about is a very simple one: liquidity. The massive levels of liquidity that are being provided by the global central banks is playing a key role in the rally in Bitcoin this year in our opinion. No, we are NOT saying that it’s the only reason by any means. We’re not even saying that it’s most of the reason. However we ARE saying that it has played a very important role this year. In other words, the liquidity that is being provided by the global central banks...and will continue to provide over the next two months or so (in order to offset the Covid-related lockdowns) has provided another material “risk-on” interval...and it has lifted the prices of many risk assets...including stocks and things like Bitcoin.

This is very similar to what happened in the spring. The liquidity was massive...and it took pretty much ALL assets higher. However, after the initial rally subsided (by May), the liquidity began to move into a much more narrow number of securities. The liquidity began to concentrate in the assets that had the most momentum. Over the summer, that concentration was the FAANG stocks. However, after the September correction, the momentum shifted away from the FAANGs and is now following the assets with the most momentum...like Bitcoin.

As we stated in an earlier bullet point, we believe that the liquidity spigots will likely begin to shut down at some point in the first half of next year (likely in the first quarter). When that happens, Bitcoin will become quite vulnerable to a deep correction. (Again, the liquidity will not disappear, but it should become less plentiful...and when an asset shoots powerfully higher due in large part to one reason or another...it tends to fall quite hard when that one reason becomes less powerful.)

We want to repeat that we are very bullish on the long-term potential for Bitcoin...AND we still believe it can rally further over the near-term. However, we strongly believe that not enough people realize that although there are many reasons to like Bitcoin on a fundamental basis, a lot of the recent rally has been fueled by central bank liquidity. If (we think when) that liquidity becomes less plentiful, it will have an outsized impact on this asset class. It has had an outsized impact on the upside...so it should have an outsized impact on the other direction as well.

Therefore, we are a lot more cautious about this asset class on an intermediate-term basis. Ride the wave for now, but we’ll be looking to take profits in Bitcoin at some point early in the New Year...with the expectation that it will see another deep correction (just like it has a full 20 times since 2013!!!).

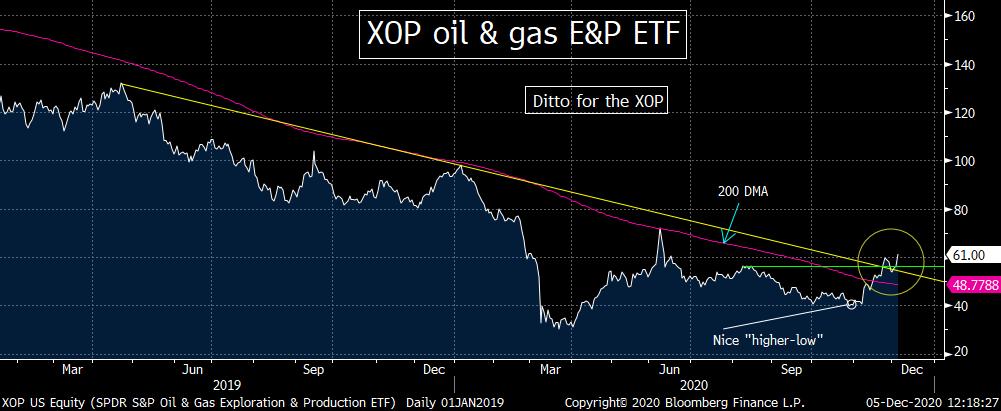

6) In an earlier bullet point, we talked about one group that had been lagging the broad stock market for a very long time, but has started to outperform quite nicely more recently...the bank stocks. Another one that is seeing a similar trajectory is the energy sector. There are A LOT of non-believers out there. It seems like every energy analyst we read about says that the supply/demand picture will not provide the kind of fuel to help the underlying commodity rally much in 2021 (despite the fact that the economists at most of those firms are bullish about next year’s growth). We’d also note that despite the almost 30% rise in WTI over the past five weeks, bullishness amongst futures traders is still only 53%. (That number doesn’t get concerning at all until it gets above 75 or 80.)

Therefore, we think the skepticism around this rally actually bodes quite well for the commodity. (We’d also add that BMO announced last week that they were getting rid of their U.S. oil & gas investment banking unit. We wish we had $100 for every time a Wall Street firm exited a business at EXACTLY the wrong time over the past 30+ years!!!)

Anyway, on a much shorter-term basis, we’ll be watching some key levels on the energy stock ETFs...to see if they can gain even more upside momentum as we move into the end of this year and early next year. On the XLE, we’re watching the November highs of $40. It actually broke very slightly above that level on Friday. However, as we ALWAYS say, we’re going to have to see a more meaningful break above that level before we can confirm the move.

The XLE was already able to break above its 200 DMA (in mid-November), so that’s quite positive. It’s also positive that it has been able to hold above that line during its recent month-end pull-back. (The XLE had become quite overbought on a very-short-term basis in late November, so last week’s mild pull-back has been normal and healthy). If the XLE can continue to hold above that moving average...and can then make a more meaningful “higher-high” above its November highs of $40 than it did on Friday, it should give it the kind of renewed upside momentum that will take it surprisingly higher over the coming weeks.

We do need to point out that the more important resistance level for the XLE on a longer-term basis is the June highs of $46.85. That kind of rally would give it a VERY important “higher-low/higher-high” sequence. THAT would be VERY bullish on a longer-term basis. For now, however, a break above $40 should still help the group outperform as we move into the end of the year.

The situation is very, very similar for the XOP oil & gas E&P ETF. It has also broken above its 200 DMA...and it has also broken slightly above its key resistance level of $60. So if it can break above those November highs of $60 in a more significant way...it should give is another jolt of upside momentum. (The June highs of $71.85 is the more important longer-term resistance level for the XOP as well...but a break above $60 should still be quite bullish on a near-term basis.)

The energy sector is still incredibly under-owned, so if these ETF’s break above the key short-term resistance levels, it should lead institutional investors to reweight their holdings for this sector. That is something that could take this (still hated) group to outperform in a way that most people thought was impossible just a few short weeks ago.

7) Gold.....We must admit that we’re a bit torn about the yellow metal right now. We would have liked to see gold see one more wash-out move this past week...down below $1,750...to really wash it out. That would have made it a screaming buy...as it would have made it extremely oversold and over-hated. However, assets do not always become completely washed-out before they see important bottoms, so this week’s bounce could be something that has legs........Anyway, we’ll give you some comments on both the bullish side and the bearish side...and then I’ll give you our take on which way it will go.

Recent free content from Matt Maley

-

THE WEEKLY TOP 10

— 10/23/22

THE WEEKLY TOP 10

— 10/23/22

-

Morning Comment: Can the Treasury market actually give the stock market some relief soon?

— 10/21/22

-

What Do 2022 and 1987 Have in Common?

— 10/19/22

-

Morning Comment: Which is it? Is stimulus bullish or bearish for the stock market?

— 10/17/22

-

Morning Comment: Peak Inflation is Becoming a Process Instead of a Turning Point

— 10/13/22

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464