2 Under-Valued, Financially Sound, Strong Growth Stocks to Consider

Sponsored by the Dr Stoxx Options Letter

In my most recent blog post, I highlighted 3 "strong stocks" to watch. All three came through my growth-value-technical strength hybrid scan. The stocks were: TEX, GPRE and CSIQ. All three stocks are up nicely since then, with GPRE making the most sizable move.

Another scan I like to run is one that keys in on fiscally sound companies (dividend payers, strong balance sheet, low debt) that are also showing decent growth metrics and are ready for a price breakout. Today I have two such stocks to bring to your attention.

Again, if you want to trade any of these suggestions, I strongly recommend doing your own analysis and setting a reasonable stop-loss on each position to protect against any unforeseen change in investor sentiment. See my analysis below.

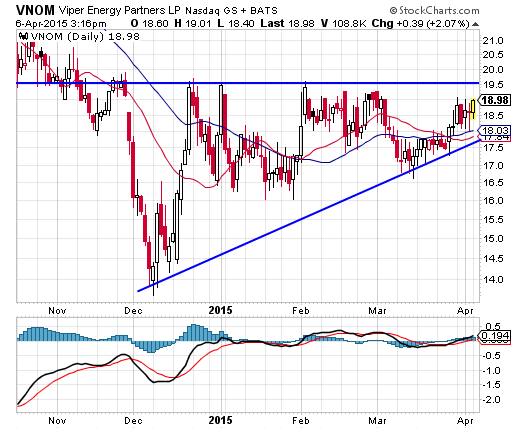

- Viper Energy Partners (Nasdaq: VNOM)

Energy stocks have been hard hit on the record-setting drop in oil prices, but they may be ready for a turnaround into the 2nd quarter as the price of crude finds a bottom. Weakness in the sector has one key advantage: it makes the stronger players stand out. One such company is Viper Energy, an MLP subsidiary of DiamondBack Energy, which aims to distribute cash to shareholders as it maximizes income from energy producing properties in the Permian Basin (Texas). The stock pays a 5.4% dividend, grew eps a whopping 850% this year, has no debt, trades at a low price-to-book, and is expected to double earnings this year. The chart is nicely coiled up in an extended bullish base. If it can climb above $19.50 this could really gain some traction and move into the mid-20's:

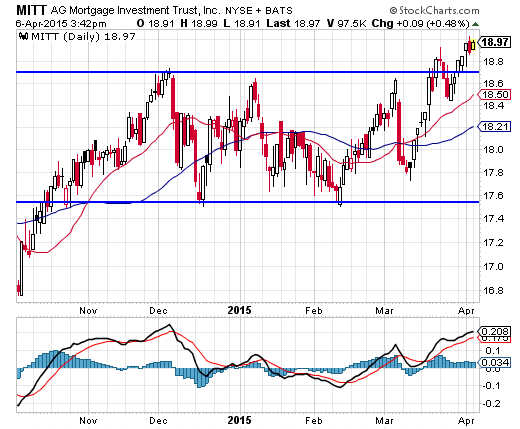

2. AG Mortgage Investment Trust (Nasdaq: MITT)

While this stock is not as exciting as VNOM on a price performance basis, it does sport an enormous 12.7% dividend. This is a REIT managed by Merrill Lynch & Co. so you know it is sound and conservative. The company grew eps over 300% last year, and shares trade at a tiny price-to-book of 0.94, meaning that the company is worth more than its current market cap. The chart shows a clean break upwards from a bullish rectangle pattern which, according to chart pattern expert Bulkowski, is the most reliable of the bullish chart patterns. We should see another $1.50 to $2 in upside over the next year or so, even as you collect those nice $0.60 paydays each quarter.

As always, it is strongly suggested that you do your own due diligence on any suggestions made here. I may or may not be invested in any of the companies written about in my blog. My subscribers always have first access to my proprietary research before being published; but there is also no guarantee being made that anything published here was already sent to subscribers. Sometimes a stock idea is just an idea!

Blessings, TC

Recent free content from Dr. Thomas Carr

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464