Cup & Handle Weekly Macro - August 19, 2014

Click here for Cup & Handle's Weekly Letter - August 19, 2014

Greetings,

The Financial Times hit the nail on the head with a front page article from last Thursday succinctly titled “Eurozone economy fails to grow in second quarter.” In this case, the FT is referring to Q/Q GDP growth, as the economy did actually grow a measly 0.7% Y/Y, but Europe remains alarmingly sluggish and things could be getting worse. Germany, long considered the economic workhorse of the EU, declined -0.2% Q/Q in the second quarter. France, Europe’s second largest economy, registered no growth at all. But the real problem child of Europe is Italy, which declined -0.2% Q/Q in the second quarter, and has now fallen into its third recession since 2008.

At this point, it might be more accurate to say that Italy is in the midst of a depression since GDP is now at the same level it was in 2000, and has declined in 11 of the last 12 quarters. Similar to Japan, it appears as though the Italians are caught in a nasty deflationary trap, although Japan has managed to grow 13% since 2000.

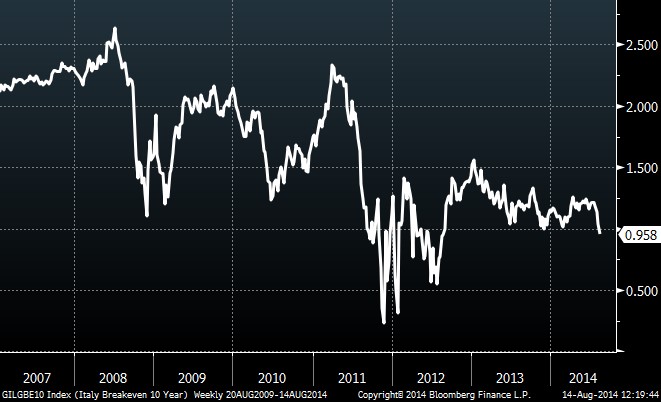

Italian 10-Year Inflation Breakevens

Italian 10-year inflation breakevens are now at their lowest levels since 2011 when the European sovereign debt crisis threatened to spiral out of control. Eventually Mario Draghi ended that crisis by saying he would do “whatever it takes,” but apparently “whatever it takes” isn’t enough. Some of these charts and data points are downright ugly. Germany’s ZEW indicator of confidence among professional investment analysts sagged to a 20-month low in August. Spain, where the unemployment rate is 24%, saw consumer prices drop sharper-than-expected to -0.4% Y/Y in July.

All of these negative data points and the elevated tensions in Ukraine have pushed investors into safe-havens, notably German debt. For the first time in history, 10-year German Bunds yields fell below 1.0% last week, and 2-year Bunds are offering a negative nominal yield. It might seem like selling EUR is the obvious move here, but the deflationary forces are actually boosting real yield across the continent – making EUR more attractive in the process. We believe the best way to play this theme is through equities in select markets, on both the long and short side, and it’s reflected in our portfolio.

Again, if you’d like to monitor our portfolio and receive real-time updates and trade alerts, please check out our Marketfy page. Our portfolio has been up and running for three weeks, and we’re already up 2.5% since inception. Also, we should be publishing our next monthly investment recommendation within the next week. These investment recommendations are now premium subscriptions, and if you haven’t signed up already, please check out our newsletter package on Marketfy.

Today’s letter will cover several topics, including:

- Trouble in Turkey

- Japan is shrinking

- Brazilian opportunity?

- QE Anomalies Part VII

With that, we give you this week's letter:

As always, if you have any questions or comments or just want to vent, please send me an email at mike@cup-handle.com.

Until next time, tread lightly out there,

Michael Lingenheld

Managing Editor – Cup & Handle Macro

Recent free content from Michael Lingenheld

-

The Finale - April 21, 2016

— 4/20/16

The Finale - April 21, 2016

— 4/20/16

-

The Spring Freeze - April 6, 2016

— 4/05/16

-

Dependent on Friday's Data - March 30, 2016

— 3/29/16

-

Money For Less Than Nothing - March 23, 2016

— 3/22/16

-

Avoid the Crowds - March 16, 2016

— 3/15/16

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464