THE WEEKLY TOP 10

THE WEEKLY TOP 10

Table of Contents:

1) Stagflation IS here…and it IS going to get worse.

2) On a technical basis, we sit at a CRITICAL juncture for the S&P 500 and NDX 100.

3) A “re-rating/re-valuation” process in the U.S. stock market was inevitable…and it will continue.

4) People still can’t make themselves believe that the “Fed put” is still at a much lower level.

5) Credit spreads continue to widen. God help us if we’re headed for a “credit event.”

6) Get ready for a lot more volatility in the currency markets!

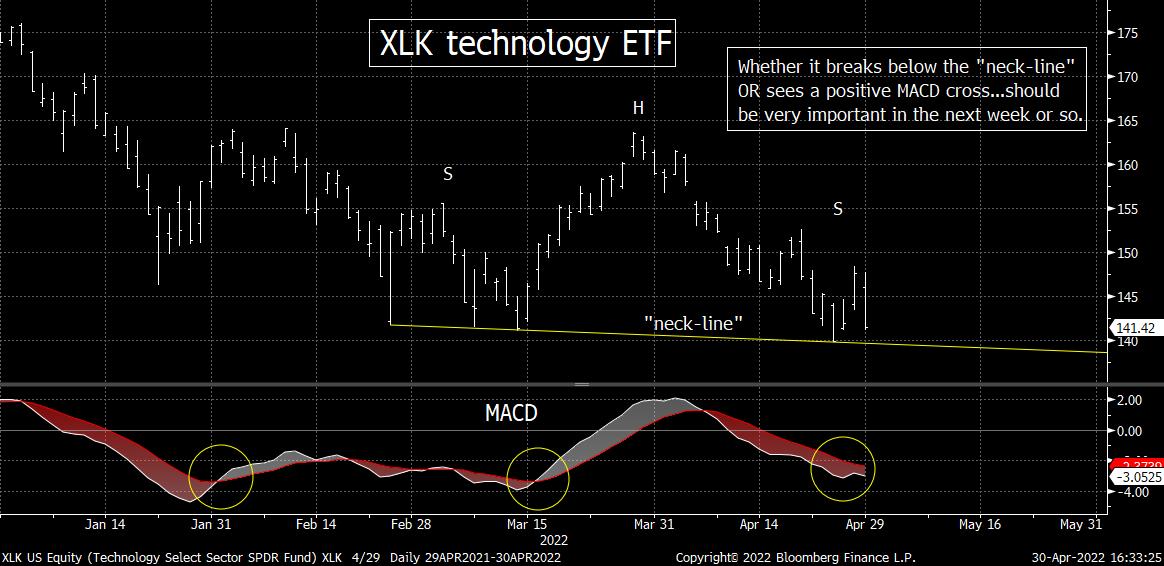

7) Believe it or not, the XLK tech ETF is still above its March highs.

8) We tend to need an important change in policy to create a bottom in the stock market.

9) Will the “curse of the cover story” claim Elon Musk as a victim?

10) Summery of our current stance…....The Mork & Mindy syndrome.

1) The majority of Wall Street does their best to avoid discussing the issue of stagflation. No, they don’t completely ignore it, but they are not giving this issue the due it deserves. The war in Ukraine…and the way it has played-out thus far…has raised the odds substantially that we will indeed get a meaningful bout of meaningful stagflation over the next year or more.

It’s interesting to see how little attention the war in Ukraine has been getting over the past two weeks or so. In our opinion, the development that took place in the Russia/Ukraine War during April are just as important (or even more important) than any other issue facing the markets right now…..The war has shifted from one that was supposed to be a short-term “blitzkrieg” type of takeover of Ukraine…to one that has become a “war of attrition.” This means that the inflation is going to be a problem that will be bigger…and last longer…than anyone (including the Fed) was thinking at the beginning of the year.

Economists have a way of making everything sound complicated. However, the thrust of the issue of stagflation is actually pretty darn simple. It takes place when inflation is driven by a lack of supply…rather than an increase in demand. (Supply driven inflation also tends to be more severe than demand-driven inflation.) When (mild) inflation is driven by demand, individuals and businesses can afford the price increases. Everybody wins. However, when inflation is driven by a lack of supply (which tends to be more severe inflation), the result almost HAS to be “stagflation.”

When inflation is supply driven (like it was in the 1970s…with the OPEC embargo)…people and businesses cannot afford the higher prices. They are not making more money…like they are when the inflation is demand driven. Therefore, stagflation becomes a self-fulfilling prophecy. At some point, the higher prices CAUSE a decline in demand. The problem is that when higher prices are driven by supply issues, a drop in demand does NOT cause those higher prices to reverse and come back down…because the lack of supply keeps them elevated!

Actually, we should say that a downturn of demand in a supply-driven period of inflation doesn’t cause prices to fall…UNTIL demand become significantlyweaker…and that usually take a long time. Therefore, we get a situation where higher prices create a slowdown in growth…but the slowdown in growth does not cause price to come back down as easily as it would if the price increases had been driven by demand……..So, we have lower growth, but still high inflation (stagflation).

This is what took place in the 1970s…when the OPEC oil embargo caused oil prices to skyrocket. In other words, a HUGE cut-back in the supply of oil from the Middle East caused those prices to jump, NOT a big increase in demand back then. As people and companies had to pay more for oil & gas, it caused them to pull-in their horns in other areas. However, the “pulling in of their horns” did not cause oil to drop. Instead, it remain extremely high for a long time…due to the supply issues created by OPEC.

Today, we have a similar situation. This time, the “supply driven” inflation started with the under-investment in fossil fuels. THEN, the covid-created supply chain issues for many, many commodities and products exacerbated the problem. However, most people thought that many of the supply chain issues would disappear by late-2021/early-2022. Even when that opinion became impractical as we moved into the fall of 2021, the consensus still thought a lot of the supply chain problems would dissipate by the end of the first half of 2020. (No, it would not have helped the supply/demand equation for crude oil, but it would have helped for MANY other products.)

Then came Russia’s invasion of Ukraine. As we highlighted above, this was supposed to be a blitzkrieg-styled (very quick) takeover of Ukraine by Russia. Of course, it didn’t workout that way…and now it has become quite obvious so most military and geopolitical experts that Russia is now engaged in a “war of attrition.”

THIS DEVELOPPMENT JUST MIGHT BE THE MOST IMPORTANT ONE FO THE MARKETS THIS YEAR!!!!.....Now that the war in Ukraine will last a very, very long time, it means that the sanctions on Russia will remain for a very long time. This means that the supply of oil and gas from Russia (and food from Ukraine) is going to REMAIN low for quite some time…and thus prices will remain high. It ALSO means that the supply chain issues that were created by Covid are not going to be resolved anywhere near as quickly as people were thinking at the beginning of the year.

All of this means that inflation is going to be stronger…and last longer…AND be tougher to combat…that anybody (including the Fed) had been thinking at the beginning of the year. As those prices remain high (even if they fall from their highest levels of the year), it’s going to cause growth to slow. However, since the higher prices will be supply-driven, they will remain with us…even as the growth slows…..Voila, we have stagflation.

Investors need to stop wondering if we are going to fall into a period of stagflation or not. Unless the situation in Ukraine changes soon…and the sanctions on Russia are lifted (which seems VERY unlikely)…stagflation IS going to become a bigger problem than it already is today…as we move through the rest of 2022. Those who ignore this probability are very likely going to get burned.

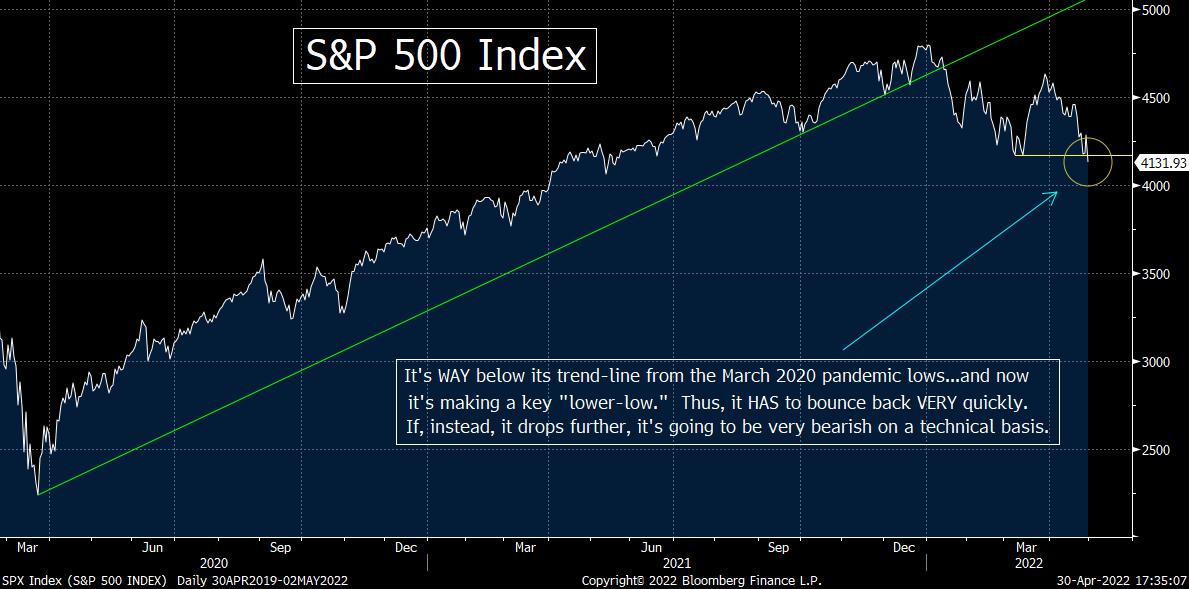

2) The stock market made a new low for the year last week…and it now sits at a critical juncture on a technical basis. Very simply, if it doesn’t bounce back early next week, we could/should be in for a scary decline over the near-term.

Both the S&P 500 Index and the NDX Nasdaq 100 Index made new lows for the year last week. This is a negative development, BUT we also have to guard against an important “head fake” in both of these indices. If they can bounce back sharply and quickly next week, we could stave off a move into official bear market territory for a while. (Maybe even several months.) However, if we see any more downside follow-though will not be good at all for the stock market at all.

We do need to point out that the stock market is getting somewhat oversold, BUT it’s not an extreme condition. However, given that sentiment is quite bearish, the market just might be oversold enough to give us a bounce very soon. Thus, it is not out of the question that the stock market might be able to bounce-back very quickly…and regain the lows from March. If that can happen, it will give the stock market some MUCH NEEDED relief (at least for a short while).

Put another way, if the S&P and NDX can regain their March lows quickly…and see a nice bounce in the very near future…last week’s lows could still be seen as a “double-bottom”…and that would be quite bullish. That kind of strong bounce could create the kind of momentum unwinding that could lead to an outsized rally….as a lot of shorts would need to be covered…and a lot of bearishness would need to be worked-off. (Of course, FOMO would also likely play a key role if the market can finally see a sustained advance.)

If, however, the S&P and NDX break meaningfully below their 2022 lows, it will not only confirm a key “lower-low,” but it will also take them below the “neck-line” of a “head & shoulders” pattern. Therefore, this would be a clear signal that the stock market has not “priced-in” all of the headwinds that the face the marketplace today (like the bond market has)…and it should lead to another significant leg lower for the broad stock market…and push us into bear market territory for the S&P 500.

You might ask why we could think that the stock market could fall a lot more if it’s already getting somewhat oversold. Well, the problem is that there is still a massive amount of leverage in the marketplace today. (More on this issue in a later bullet point.) When there is a lot of leverage in the system, markets CAN fall A LOT further…EVEN when they’re oversold.

You see, margin calls are not implemented when the market is down by only 5%. It’s only when the market gets hit particularly hard that a broad wave of margin calls (“forced selling”) hits the marketplace…and thus this only happens when the market is already oversold! Therefore, it is not out of the question (at all) that the SPX and NDX could see a significant decline if they break below the March/April lows in a more meaningful way next week. In fact, given the level of leverage in the markets, it is PROBABLE that we’ll see a lot more downside movement before we see an important bottom (if, repeat IF, we move materially lower early next week).

Of course, things could get REALLY ugly…very quickly…so it’s not out of the question that a lot of the selling could be done by the time the Fed makes its announcement about their newest rate hike…and their plans further rate hikes…on Wednesday afternoon. (So, it is possible that we’ll get a “sell the rumor, buy the news” reaction of the Fed’s rate hike next week….……Either way, if the market does not bounce immediately early next week, things could get very ugly (in terms of price)…even if a key bottom comes just a few days later (in terms of time).

3) We heard many times in the last week about how the stock market was being “re-rated”…or that valuations are in the process of being “reset.” We’re glad a lot of people have jumped on this band wagon, but it would have been a lot more helpful to many investors if those people told us that this would happen before the S&P fell 14% and the Nasdaq dropped more than 22% (like we did).

We’ve heard the term “re-rating” a lot when it comes to the stock market over the past week or so. In other words, many pundits are now saying that investors are re-evaluating the proper valuation levels for the today’s stock market…and the tech stocks in particular. It’s great these pundits are finally coming to this conclusion, but it’s a conclusion we drew many, many months ago……Ever since the Fed starting strongly hinting that they were going to end QE…and especially after they started saying they were going to hike short-term interest rates…we’ve been saying that the 2021 valuation levels could not possibly hold. Put another way, we don’t understand why it has taken most pundits so long to understand that the stock market would HAVE to be “re-rated” in 2022.

When the Fed starting confirming (in mid-November) that they were not only going to end QE, but they were also going to start raising short-term interest rates much sooner than anybody had been thinking, we started saying that the upside in the stock market was limited…and then it would have to decline before too long. Well, the market did rise a bit more in late December…and exceeded its mid-November highs by almost 2% by the first day of trading in January. However, it has been falling steadily ever since. (And we never got the year-end “melt-up” in late 2021 that some were calling for either.)

There have been two issues at play with our negative call. First of all, we made the simple argument that ultra-low interest rates allowed for higher than the historical average on valuation levels, a rise in those rates would move the “fair value” for the stock market down to more in-line with historic levels……Sure, interest rates are still low compared to the past 50 years, but we still believed valuation levels had to come down as rates moved higher…at it sure looks like we were correct. (Heck, we remember when 17x earnings was considered very expensive.)…….No, we’re not saying that the market has to fall to (or below) 15x earnings to make valuations attractive, but it was quite evident that they had to come down….and down they have come.

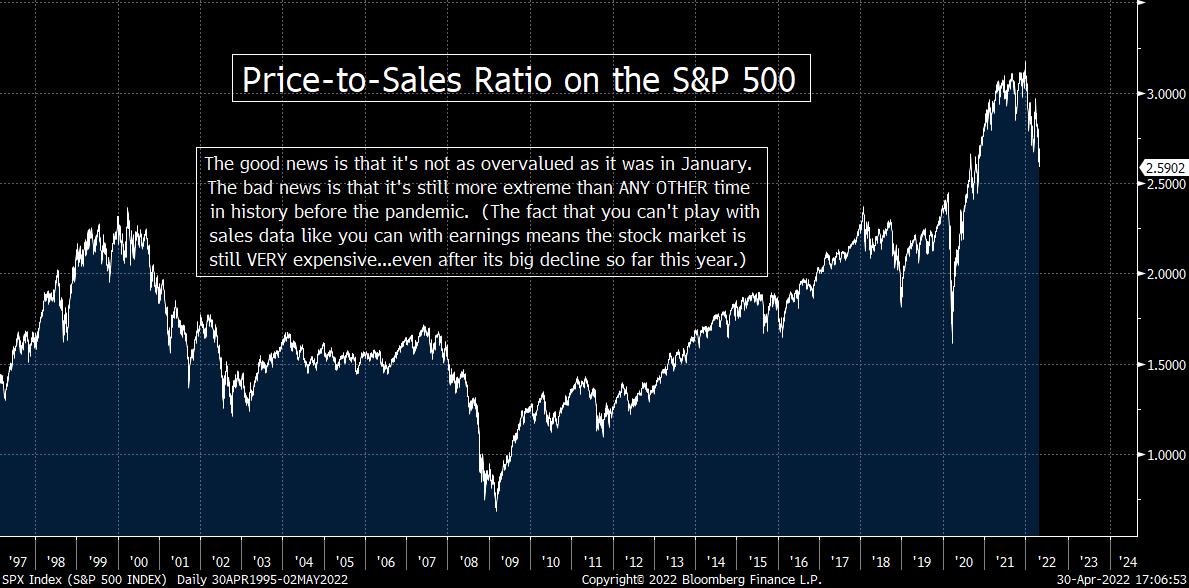

The second issue is that the emergency levels of liquidity that was being provided by the Fed…especially when they kept providing it long after the emergency in the economy had passed…was a key reason why valuations had become so extreme. (It wasn’t just the P/E on the S&P 500, but it was also the ALL-TIME record levels of overvaluation on the “price-to-sales” readings and “market cap-to-GDP as well.”)…..In other words, once the emergency in the economy had passed, much more of the excess liquidity moved into the markets instead of the economy.

When the member banks HAD to sell bonds to the Fed during their massive (emergency) QE program, the banks had to do something with that money. (As “member banks,” they cannot say no when the Fed comes in to buy bonds from them.)…..As the economy improved, the banks put more of that money into risk assets and less into the economy. That, in turn, pushed the stock market to artificially high levels…..It was like the banks were engaged in the opposite of “forced selling” from margin calls. With the liquidity still flowing in a massive way…and the economy humming along nicely…it was almost like they were engaged in “force buying”…because the had to do SOMETHING with the money!

The problem was that human nature came into play. Instead of understanding that the artificial stimulus was playing an important role in pushing valuation levels to extremes, they thought 100% of the high valuation levels were due solely to the low level of interest rates….Don’t get us wrong, we understand that lower interest rates theoretically justify higher valuations, but investors couldn’t bring themselves to believe that the excess liquidity had taken valuation levels to heights that could not be justified by low interest rates alone. (And therefore, they couldn’t be justified by a rise in those rates…even though they were still low compared to history.)

A “re-rating” or a “re-valuation” process in the stock market has been inevitable ever since the Fed decided to end QE and (especially) when they found it necessary to raise short-term rates to fight inflation. Both of these moves ARE the right move to be making this year. (The mistake came when then kept the emergency level of stimulus flowing long after the emergency had passed.) Yes, it has been…and will continue to be…painful as we move through 2022. Luckily, we’ll get periods of relief from time to time (and we might get one soon). However, the inevitable “re-rating/re-valuation” process is upon us…and it will likely last longer than most people are expecting right now.

4) It is amazing to us how so many people keep trying to say that the Fed will bail out the markets soon. They do admit that the “Fed put” is further out-of-the-money than it used to be, but they keep trying to tell us that they won’t let the markets fall much further than they already have so far. They don’t seem to understand that the Fed is not as “market dependent” as they have been for the 14 years (nor that the Fed CANNOT be as “market dependent” as they have been…because inflation is now a problem).

For many, many years, we have been saying (and have shown) that the Fed is much more “market dependent” than they are “data dependent” when it comes to their monetary policy. However, we believe this has changed to a certain degree in recent years. (No, it hasn’t disappeared, but it has changed to a certain degree in our opinion.)…..We all agree that there has been a “Fed put” under the market for a very long time…and we all agree that this “Fed put” is now further out-of-the-money than it used to be. However, few people seem to realize WHY this is so.

In our opinion, the reason the Fed put is further out-of-the-money than it used to be is quite important…because it means that they will let the markets fall further than many people are thinking right now…..One of the reasons that the “Fed put” is further out-of-the-money today is that the financial system is more stable than it was from 2008 into the middle of the last decade. Every time the Fed ended QE back then, the stock market rolled over. Given that Ben Bernanke’s Fed was using the stock market (and other asset markets) as a tool to help stabilize and grow the economy (something he stated publicly on many occasions back then), any deep decline in the stock market caused that financial stability to wobble considerably (it was still a very shacky financial system back then). Therefore, they HAD no choice but to keep their “Fed put” at a level that was just underneath the markets in the half dozen or so years following the crisis.

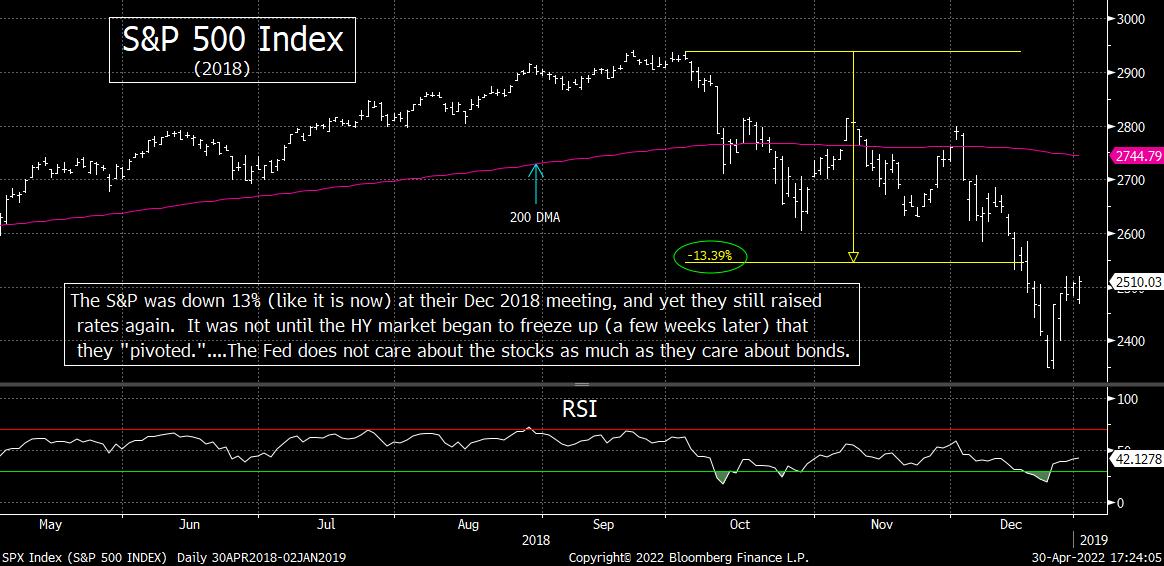

However, as the global economy stabilized, they felt that they could “normalize” (raise) interest rates once again…which they KNEW would “normalize” (lower) stock prices. So, in the second half of the last decade, they started to tighten monetary policy. When it eventually started negatively affecting the stock market, the Fed DID NOT care! In fact, when the S&P was down 12% at their mid-December 2018 meeting, they STILL raised rates once again. It was not until the credit markets (especially the high yield market) began to break-down badly…that they decided to “pivot”…and end their tightening policy. Therefore, it was NOT the stock market that made them “pivot,” it was problems in the fixed income markets that did it. In other words, it was not until they realized that the financial system was still not on the kind of firm footing as they thought it was…that they decided to save the day.

The same thing took place in 2020. It was not until the credit markets all but completely froze-up in March of that year (and after the S&P had fallen 35%)…that the Fed came to the rescue. They were not trying to save the stock market…they were trying to save the financial system…which was about to collapse due to the shut down of the entire global economy. (YES, we WERE on the brink in 2020…almost as much as we were in 2008!!!)

Therefore, the question now is whether the financial system is stabile enough to withstand a further decline in the credit markets. If they can, the Fed will not care how much the stock market falls…unless or until it has an impact on the fixed income market (which would impair financial stability). Credit spreads have yet to widen out as far as they did in 2018, so it is likely that they’ll let things fall quite a bit further over time. (They might try to jawbone things higher from time to time…so that the market adjustments do not take place all at once…but they’ll likely let market fall further over time.)……If the financial system is in the kind of good shape that most pundits believe, the Fed will be able to let the fixed income markets fall even further than they did in 2018 before they come to the rescue……..THAT is not a great scenario for the stock market!

Of course, there are some who believe that the financial system is still VERY delicate. Given the record levels of total debt in the U.S. and around the globe, it’s hard to argue with them….However, we also have the issue of inflation to contend with now…which is something that was not problem at all in the first half of the last decade…or in 2018 or 2020. With inflation at its highest level in 40 years…and with it very likely going to stabilize at a very high level (even if stabilizes at a lower than it stands now)…it’s going to make it much tougher for the Fed to “pivot” as quickly as they have in the past.

Don’t get us wrong, if it becomes evident that the financial system is in trouble again, we are confident that the Fed will do whatever it needs to do to come to the rescue. However, if something like that happens, the stock market will be a lot lower than it is now…….Therefore, we believe that those who say the Fed will “pivot” in a material way in the next few months have a problem. If they’re right, it will only be due to the fact that the markets are a lot lower than they are now…and thus it’s not a good reason to be bullish.

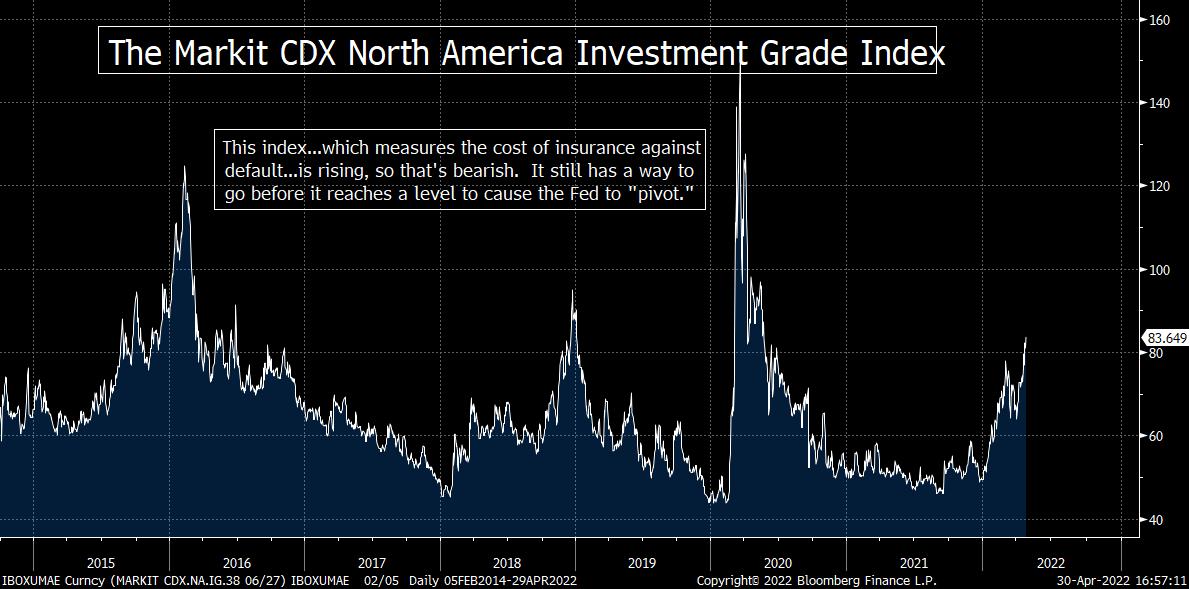

5) Credit spreads continue to widen out. Our concern is that they present a “lose/lose” situation for the stock market. If they don’t widen further, the Fed is unlikely to “pivot” soon (because they care much more about the credit markets than the stock market). However, if they DO widen out significantly, the stock market will fall a lot further before the Fed changes course.

Credit spreads continued to widen last week. On the one hand they’re still below the serious levels they reached during the financial crisis…during the European crisis of 2011/12…in 2016, 2018 or 2020. On the other hand, they’ll probably have to widen out a lot further before the Fed becomes concerned enough to “pivot” their policy. Therefore, the situation with credit spreads is a precarious one. It’s almost a lose/lose situation. We’re not going to get help from the Fed unless credit spreads widen out further (because as we highlighted above, they really only care about the credit market, not the stock market), BUT if credit spreads DO widen out further, the stock market is going to fall a lot more BEFORE the Fed comes to the rescue.

We have harped on the issue of credit spreads many, many times this year, so we won’t bore you by re-hashing the issue to death. We’ll just show you a couple of charts (below) that show you were the spreads stand for investment grade and high yield spreads…..HOWEVER, we DO want highlight one more point involving this issue…and we’ll make it short and sweat: If credit spreads continue to widen…and if they widen in a significant way…it’s going to raise the odds that we’ll see another “credit event.” If (repeat, IF) THAT happens, things are going to get even uglier…and they’re going to get “uglier” very quickly after such an “event” takes place.

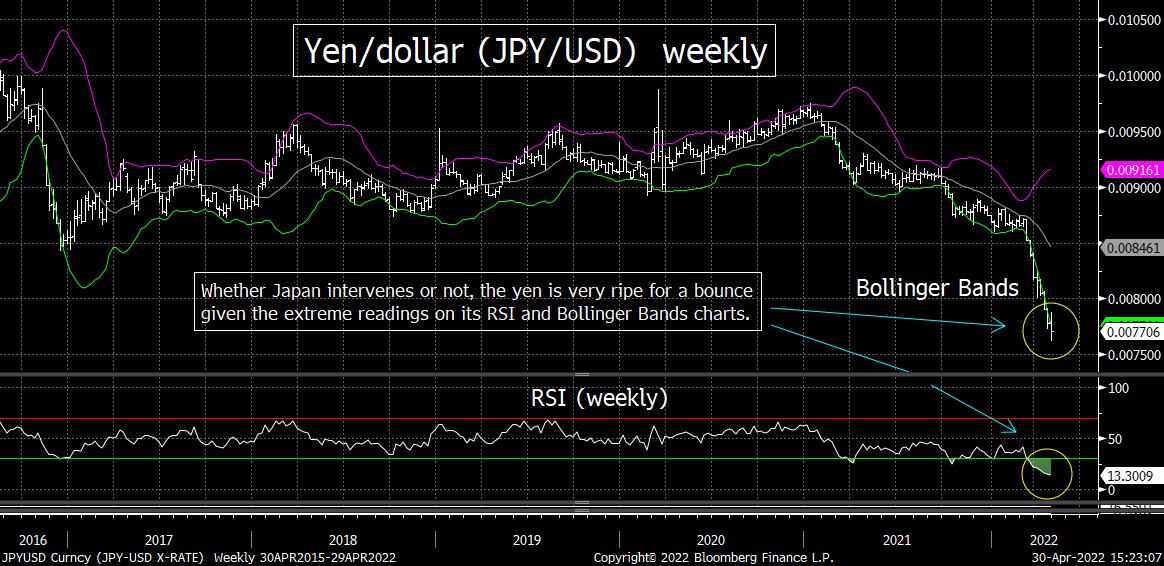

6) This past Thursday, we highlighted how with all of the focus on the tech stocks, the lockdowns in China, etc., the big moves several global currencies were not getting the attention they deserved. We said that the currency markets could suddenly become one of the most important issues of the financial world very quickly in the coming days and weeks.…..We have several currencies that are reached extreme levels on their charts…AND have reached extremes that is likely going to force some governments to act to defend their currencies.

There have been several HUGE moves in the currency markets during the month of April…with the dollar rallying very strongly…and the euro, yen, and yuan all falling in a significant fashion. As we highlighted this past Thursday, the extreme moves we’ve seen in these currency markets could become VERY important issues in the coming days and weeks for market participants.

The incredibly drop in the yen this year is particularly interesting to us. The authorities in Japan did release a strongly worded statement late last week warning about the decline in the yen…saying they would respond “appropriately” to their currency’s big decline. However, they also said that they would not make a move to devalue their currency. That’s great, but as the old saying goes, “Never believe a rumor until it is officially denied.”

Looking at the chart on the DXY dollar Index, it shows that it’s the most overbought it has been since 2015. It is also testing its highs from 2017 (which were also almost reached in 2020). Whenever an asset tests an important resistance level at a time that it has become extremely overbought, it almost always rolls back over in a material way over the short-term. Therefore, those who are looking for a breakout move in the dollar over the near-term should be very careful. It is much more likely that it will have to pullback and digest its recent (very large) gains before it takes a run at a key higher-high. (This analysis has NOTHING to do with the intermediate and long-term prospects for the dollar. We’re just saying that on a technical basis, it has become ripe for a pullback.) (First chart below.)

Japan’s yen has been under significant pressure for the past two months…with the BOJ sticking with its ultra-easing policy (in the face of tightening by many of the global central banks). The yen has become the most oversold it has been vs. the dollar since 2015 on its weekly RSI chart…and its Bollinger Bands chart shows that it is more than 2 standard deviations below its 20-week moving average. Therefore, even if the authorities in Japan don’t do anything so support their currency, it has become ripe for a short-term bounce. If, however, they DO implement a plan to support their currency (which we think is almost unavoidable), the bounce could be something that lasts longer than most people realize right now. (Second chart below.)

China’s yen has also been incredibly weak…after the renewed lockdowns to fight the most recent surge in Covid. Its weekly RSI and Bollinger Bands charts are similarly extended vs. the dollar as the yen (if not more so). Therefore, we believe it is likely that they’ll do something to support their currency as well. (Third chart below.)

What we’re trying to say this morning is that the extreme technical readings in the dollar (overbought), the yen and yuan (oversold) make them ripe for at least a short-term reversal. (The euro is quite oversold as well.)…….More importantly, any short-term move could turn into a surprisingly big one if Japan and/or China does indeed make a move to support their currency……This does not mean that we are approaching a major long-term reversal in the currency market, but it could be one that is big enough (and lasts long enough) to catch people off guard. This is something that investors should be keeping a close eye on in the days ahead…especially since history tells us that when the currency markets become extremely volatile, so do the stock and bond markets.

7) As rough of a week as it was for the tech stocks last week, the XLK technology ETF did not make a new low for the year. That means that it has not broken below the “neck-line” of its “head & shoulders” pattern that we highlighted last week yet. Therefore, if (repeat, IF) this group can gather itself…and bounce back quickly…it could be the kind of catalyst the broad market needs to give it a stay of execution.

Needless to say, you don’t have to be a market professional to know that the action in the tech sector is vitally important to the broad stock market. The tech stocks have obviously been weak, so this has been one of the most important headwinds for the broad stock on a technical basis all year……It is interesting to note, however, that despite weakness in the sector on Friday, the XLK technology ETF did NOT make a new low for the year. Don’t get us wrong, it won’t take much downside follow-through to break to new lows for 2022, but it’s not there yet.

If you look at the chart on the XLK technology ETF below, you can see that it is forming a “head & shoulders” pattern. If the XLK rolls-over and takes out the “neck-line” of that pattern, it’s going to be very negative for the sector (and very negative for the broad market as well). HOWEVER, if it can bounce immediately, it should be enough to give it a positive cross on its MACD chart…and THAT would be quite positive…and help it avoid breaking its all-important “neck-line” of that “H&S” pattern. One of the old sayings in technical analysis is that there is nothing more bullish than a failed “head & shoulders” pattern, so there is still a glimmer of hope for the market as we move into next week.

8) The odds that we’ll see some a “washout/capitulation” move before the stock market sees a sustainable bounce is high. However, we also think we’ll need to see an important “change” take place before we make THE bottom for this correction/bear market. In our opinion, the “next bounce” will come after a round of some sort of “capitulation,” but THE bottom won’t come until an important change in policy takes place (which means it might not come until after further declines).

A lot of people are looking for a “washout” move (what some would call a “capitulation” move) before we see a sustainable bounce. We agree with this opinion. There are some who say that we won’t get a “washout” move before we bounce, but that is VERY unlikely in our opinion. There is just WAY too much leverage in the system for a “washout” move not to take place. At some point (maybe soon), a lot of investors (both individual and institutional)…from both the equity and

Recent free content from Matt Maley

-

THE WEEKLY TOP 10

— 10/23/22

THE WEEKLY TOP 10

— 10/23/22

-

Morning Comment: Can the Treasury market actually give the stock market some relief soon?

— 10/21/22

-

What Do 2022 and 1987 Have in Common?

— 10/19/22

-

Morning Comment: Which is it? Is stimulus bullish or bearish for the stock market?

— 10/17/22

-

Morning Comment: Peak Inflation is Becoming a Process Instead of a Turning Point

— 10/13/22

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464