THE WEEKLY TOP 10

I’ll be away next weekend, so I will send-out an abbreviated edition of “The Weekly Top 10” on Thursday evening. Thank you very much.

THE WEEKLY TOP 10

Table of Contents:

1) When inflation is induced by a lack of supply (rather than stronger demand), it’s not good for asset prices.

2) The complacency in the U.S. markets surrounding Evergande (& China in general) is astonishing.

3) China is clamping down on “risk taking”…other powers are considering the same thing.

4) The 50-DMA on the S&P 500 is more than just a key support level for technicians in today’s market.

5) Sentiment is not anywhere near as bullish as it usually is at important tops in the stock market.

6) Natural gas has become extremely overbought, so don’t chase it (or natural gas-related stocks).

7) The XLI (industrial ETF) has been a key leading indicator for the economy…& it’s now testing key support.

8) After a quick dip, the U.S. 10-year yield is already retesting its key resistance level!

9) Washington DC is still clueless about what Americans are feeling & thinking today.

10) Summary of our current stance.

1) During the first quarter of the year, some experts started to say that the supply chain problems would persist into the first half of 2022. That has now become the base-case scenario for everybody…with more and more pundits expecting it to be a problem throughout ALL of next year. In our minds, this means that inflation will not be very transitory at all…and given that supply-induced inflation is MUCH different than demand-induced inflation, these problems will likely cause complications for economic growth and create headwinds for the stock market going forward.

As we moved towards the end of the first quarter this year, we started hearing some alarming comments from the global chip makers and their customers. They said that the supply for chips would not only be a problem in the months ahead, but that the situation could likely persist into 2022. NOW, we hear companies like 3M (MMM), Sherwin Williams (SHW) and many others say that this is going to be a problem throughout 2022. Some experts are now saying the problems will last another two years or more! Therefore, there is little question that this supply chain problem has only gotten worse. Just look at the port of LA and Long Beach. Three weeks ago, the number of ships waiting outside the LA and Long Beach ports stood a 40. Now, the number has jumped to a new record of 60…in less than one month!!!

Also, the problem is now much more far reaching than just semiconductors. We’ve heard for months how car makers like Ford and Toyota cut their production plans due to a lack of chips, but this has spread to many other areas. We just highlighted the comments from MMM & SHW, but manufacturers of all stripes cannot get the components to manufacture their products. There are also supply problems for things like coffee, jet fuel, clothing products…you name it! (How are the kids going to play basketball this winter without their Nike’s???) Almost everything is being impacted by this pandemic-induced supply chain problem. .

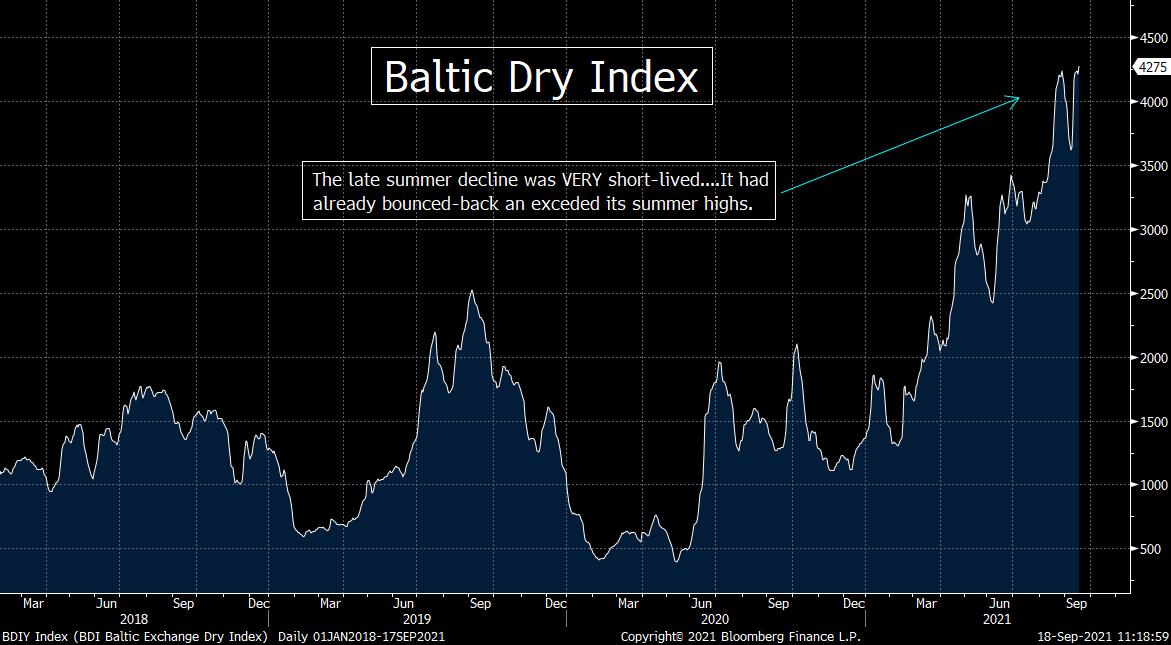

Needless to say, this is having a big impact on shipping costs. We’ve highlighted the huge rise in the cost of containers several times in recent weeks…and this has not abated. Sure, the Baltic Dry Index dipped a little bit earlier this month, but it has already jumped back to its late August highs. These costs are going to be passed-on, so those who are looking for inflation to ease off any time soon are relying on “hope”…and “hope” is a lousy investment strategy.

The big problems with supply-induced inflation is that CAUSES a drop in demand. This is much different than when demand-induced inflation (which is much more common) takes place. When demand-induced inflation kicks-in, it’s not a problem. In that case, more people have jobs…and those who already have jobs make more money…so a rise in prices does not have a negative impact on the economy. (It’s the rising demand that CAUSES higher prices…so that’s not a problem.) However, when it’s supply issues that create the higher prices, it’s a totally different story. In other words, instead of rising demand CAUSING the prices to rise (thus making the higher prices quite affordable), it’s the declining supply that CAUSES demand to fall (as the higher prices makes things LESS affordable).

When a decline in supply…rather than an increase in demand…causes inflation, it becomes a big significant problem. Not only does make it harder on the consumer to buy products, but it shrinks the profit margins for companies. That causes layoffs…and the whole thing feeds on itself. That’s when “stagflation” comes-in…….Of course, the economic textbooks do not spell describe this concept in such a simple manner, but this IS how works in the real world. (It’s actually quite plain and simple.)

The Fed (and many others) keep trying to tell us that this “lower supply-induced” inflation in only transitory. However, it has already lasted a lot longer than they said it would…and it is becoming quite obvious that it’s going to stay with us for quite a while longer. (If you read the newspapers from the 1970s, they said that THAT period of “lower supply-induced” inflation would not last very longer either. Look how that turned out.)

So this is the situation we’re facing: Higher prices due to supply problems. That creates lower demand. Higher production/shipping costs combined with lower demand creates lower profits for companies. Lower profits for companies leads to layoffs. That, in turn, leads to lower even lower demand, but since the higher prices are related to shrinking supply…instead of rising demand…prices to not come down. They stay elevated…and the whole thing feeds on itself……..…That’s a scenario for slowing growth and a slower rate of earnings growth. That’s not good for a stock market that is trading at 22x 2021 earnings and more than 20x 2022 earnings (whose estimates are now starting to look too high).

No, this does not mean that the situation will spiral into major bear market…or a situation where we return to the level of stagflation that we saw in the 1970s. However, it IS the kind of situation that will make it VERY difficult for the stock market to rise in a significant way in the months ahead.

2) The problems facing the China Evergrande Group have been around for many months, but that have received very little attention in the U.S. until the past few days. We don’t know how much of an impact this issue will have on the U.S. markets, but the complacency surrounding this issue has been unbelievable…at least until now.

We have been talking about the problems facing the massive real estate developer, China Evergrande Group, for several months now. Even though their stock has fallen 85% since January and their bonds have fallen at a steady pace all year (to 80 cents on the dollar…to 60 cents…to 30 cents), almost nobody in the U.S. has batted an eye lash. The assumption that this company was too big to fail has kept investors in this part of the world focused on other issues.

However, this past week, it was announced that this company that has $300bn in debt outstanding is going to miss its interest payments next week has finally grabbed some attention in other parts of the world. The company said that their onshore bonds were suspended from trading on Thursday…and existing holders are finding it incredibly difficult to hedge these losing positions. The CDS’s for Evergrande barely trade at all and brokers are not making the kind of markets that would enable investors to hedge themselves in any material way.

The company has already sold some assets at fire sale prices. This has rippled through the already shaky real estate market in China…as those sale prices has impacted the price of other properties in that country. It has also caused construction on many projects to stop. These moves are hurting other developers and we’re starting to some stress in China’s credit markets…with their repo rate rising to a three month high last week. Junk bond yields bounced to an 18-month high last week and there are signs that Chinese banks are starting to hoard yuan over concerns over a possible liquidity squeeze…..In other words, some sort of a contagion is not out of the question in the coming weeks.

We are not experts on China or their real estate market, so we cannot possibly know how this will playout. We certainly understand why many people around the world think that China’s government does not want this situation to get out of hand. They have been in a real estate bubble for some time now, so it’s hard to think that China would not step-in to keep the bubble from bursting all at once. This is especially true given that this crisis is beginning to cause social unrest…and if there’s one thing China wants to avoid, its social unrest.

Therefore, maybe the western markets are correct. Maybe the fact that Evergrande’s securities have crashed…and Hong Kong’s stock market has fallen 19% since February (to another new “lower-low”)…means nothing for the U.S. markets. One thing is for sure, the U.S. stock market has not priced-in ANY problems that might come from this situation, so we had better pray that it doesn’t become a contagion that spreads outside of China.

3) As investors in Japan learned all too well thirty years ago, the authorities sometimes do things in an attempt to subdue unhealthy risk-taking by their citizens. Most of those attempts by authorities do not cause their markets to move lower for two full decades, but they can and do still cause problems for markets for a shorter period of time. We’re seeing signs that the authorities in certain parts of the world want to slow the amount of risk taking in their markets today…..Caveat emptor.

We have seen many signs this year out of China…especially over the past several months…that they want to clamp-down on risk taking. It actually started last year, but their crack downs on technology companies this year have accelerated in recent months. It has also spread to other industries…as China’s government basically took over the education industry…and this past week, they started going after the gaming industry.

What started out as something that people thought was merely an attempt by the Chinese government to rein-in Jack Ma…who was getting too big for his britches…has turned into an incredibly wide-ranging clamp-down. It could also be seen as a wide-ranging clamp-down on risk taking in China. This is not just something people is deducing by looking at China’s actions. It’s also something that President Xi and other key officials have strongly insinuated many times over the past few months. Xi has called his crackdown as a campaign to “crackdown the irrational expansion of capital”…and something that is being used to rein-in the “barbarous growth” in China’s tech sector.

We can debate all we want about why there have embarked on this crackdown, but there is no question that it IS taking place. When you look at the situation we just covered in the previous point regarding Evergrande, you can also see that Xi wants people to feel some pain when they take too much risk. Therefore, even if it’s just a power play on his part, President Xi and his government is still making a concerted effort to clamp down on risk taking in China.

We’re seeing and hearing a similar situation here in the U.S…with some recent comments from several FOMC members. Of course, the U.S. Federal Reserve is not going to try to clamp-down on risk-taking to anywhere near the same extent that China is on this front. However, there ARE some signs that they want to slowdown some of the risk taking here in the U.S. as well. Dallas Fed President Kaplan said recently that he is worried about “excessive risk taking”…and Cleveland Fed President Mester has signaled the same concern (although she focused on the high yield market).

In other words, if you read between the lines, the Fed is now telling us that one of the reasons they want to taper back on their bond purchases is because their massive liquidity program has moved “risking-taking” to a dangerous level and they want to rein it in going forward. No, we’re certainly not saying that the Fed’s only reason for tapering soon is to slowdown risk taking. We’re not even saying it’s the most important reason. We’re just saying that the Fed is now telling us that this issue IS playing a role surrounding their upcoming decision on the QE program.

This is another reason why we believe the Fed will go ahead next week and give a strong signal that they’ll make an official announcement about tapering back on QE in November…and they’ll begin in December. Again, the number one reason that they’ll make this move is because we have moved well beyond an emergency situation in the economy, so there is no reason to continue providing emergency levels of stimulus. Therefore, even though we got a weaker than expected employment report a couple of weeks ago…and even though we got a SLIGHTLY lower CPI number, we believe the Fed will not lead people to think that they’ll hold-off on their “tapering” move. It will come this year.

We realize that what we’re saying is sacrilege. How could anybody think that the authorities of any country would actually WANT to rein-in asset prices (especially after what happened in Japan 30 years ago)????? Well, maybe it IS a crazy thought, but if you look at what Xi is doing in China…and what some at the Fed have been saying recently…it’s not out of the question. (Let’s face it, the Fed has taken away the punch bowl in the past. BTW, that is exactly what their intentions were with their tightening cycle of 2018.)

4) We’re guessing that people are getting a bit tired of hearing about the 50-day moving average on the S&P 500 Index. However, it IS a VERY important support level for the stock market right now. We’d also note that it’s not merely an important level for technicians. It’s also an important level for many momentum-based (aglo) strategies. Thus, if (repeat, IF) the S&P 500 finally breaks that 50-DMA in any meaningful way, it could/should cause a quicker and sharper decline than most people expect.

We have been talking about the importance of the 50-DMA on the S&P 500 for some time now. Many others have joined-in in recent weeks…and rightfully so. The S&P has bounced nicely off that line on each of the previous eight occasions this year, so it has become rock-solid support for the stock market in 2021. The problem with “rock solid” support levels, however, is that once they are eventually broken in a meaningful way, it is almost always followed by a severe decline rather quickly. (The opposite is true with rock-solid resistance levels.)

One of the reasons why we’re worried that the 50-DMA won’t “hold” this time is because it has been hanging around this line for more than a week now. On the other previous tests of the 50-DMA, the market has bounced almost immediately. It took one day…or two (at the most) before it bounced back quite strongly. This time, however, it has tested that line four days in a row…without bouncing strongly. (In fact, we could easily say that it has been hanging near the 50-DMA for the past six trading days.) The fact that is has not been able to bounce quickly…like it has so many other times in the past…leads us to believe that investors are stepping in to buy the market this time around. In other words, they’re losing confidence in this rally.

As we said, whenever any stock (or any other asset) tests a support or resistance level many, many times…like this one has in 2021…the move that follows a meaningful break of that support/resistance level is almost always a substantial one. However, in today’s markets, the moves could be even bigger than usual. With the billions of dollars that are invested in momentum-based algo trading funds, the odds are high that the reversal of the trend will be even bigger than usual.

When you have billions of dollars of buying power…that has bought stocks in a mindless fashion every time the S&P tests its 50-DMA for over 2/3 of a year…the exit of that buying power can have an outsized impact on the market. However, given how most of these strategies work, that sizable pool of money will not just “stop buying” stocks. They’ll quickly start selling them in a meaningful (and mindless) way! In other words, we’re looking at a scenario where a major force in the marketplace could quickly turn from being a huge buyer in the stock market…to a big seller…rather quickly.

Therefore, we worry that when the S&P finally does beak below that key support level in any material way (whether it happens next week…or many weeks from now), it is likely going to cause a very quick (further) sell-off.

Having said this, we do need to point out that the 100-DMA did provide support for the S&P back in both September and October of last year. That line is only 2.4% below where the index closed on Friday. Therefore, this might be another level where algos will try to buy stock. That, in turn, could keep a rout from taking place immediately. However, it the 100-DMA of 4327 doesn’t hold, there really isn’t any good support until you get down to the 200-DMA of 4100.

This is a long-winded way of saying that in today’s machine-driven trading market, we could see some unbelievable volatility over the coming weeks. If the 50 DMA is broken, the declines could/should be fast and furious…but the bounces could be quite similar…so hold on to your hats.

5) We need to point out that the level of bullishness is not anywhere near where it usually is when the stock market is forming a top…that is followed by a full correction. Don’t get us wrong, investors are ACTING in a very bullish way, but they sentiment is not wildly bullish, so this is something that puts a chink in the armor of our bearish stance right now.

When the stock market is making a significant top, it usually happens when sentiment is very bullish. (If there are too many bulls, there’s nobody left to buy stocks!) This does not mean that every correction or every pull-back begins when the consensus is extremely bullish, but it is certainly common to have a heightened level of bullishness before an important top.

This is certainly not the case right now. The Investor’s Intelligence data (which measures the bullishness of investment newsletter writers) saw its bullish level drop below 50% last week. We usually see that number well above 60% at tops, so the fact that it is well below that level shows that bullish sentiment is far from extreme. We’re seeing the same thing with individual investors. The AAII poll of individual investors has a bullish reading of only 22.4%! That compares to a bearish reading of 39.3%, so you can see that the retail investors is not even close to being extremely bullish right now……Finally, when you look at the DSI data, it shows that futures traders is 59% for the S&P and 65% for the Nasdaq. No, that’s not low, but it certainly isn’t high either. You’d want to see that number in the 80s (at the very least) if you were trying to describe that group of traders as overly bullish.

Having said all this, even though investors are telling pollsters that they’re not very bullish, they are certainly ACTING in a bullish manner. According to the BofA flow of funds analysis, investors pulled $62 billion dollar out of money market accounts last week and put $51 billion of that money into stock funds…the largest inflow since March! Therefore, even though investors are “talking” in a bearish manner, they’re investing in a VERY bullish one!

We’d also note that the global shut-down of the economy…and the massive stimulus that followed that shut-down…has made the investment world a very different one from any other time in history. Therefore, maybe some of inverse correlations between sentiment and the stock market do not work any longer. However, sentiment indicators have been very good ones in the past, so we do need to acknowledge that are some developments that are working against our bearish stance right now.

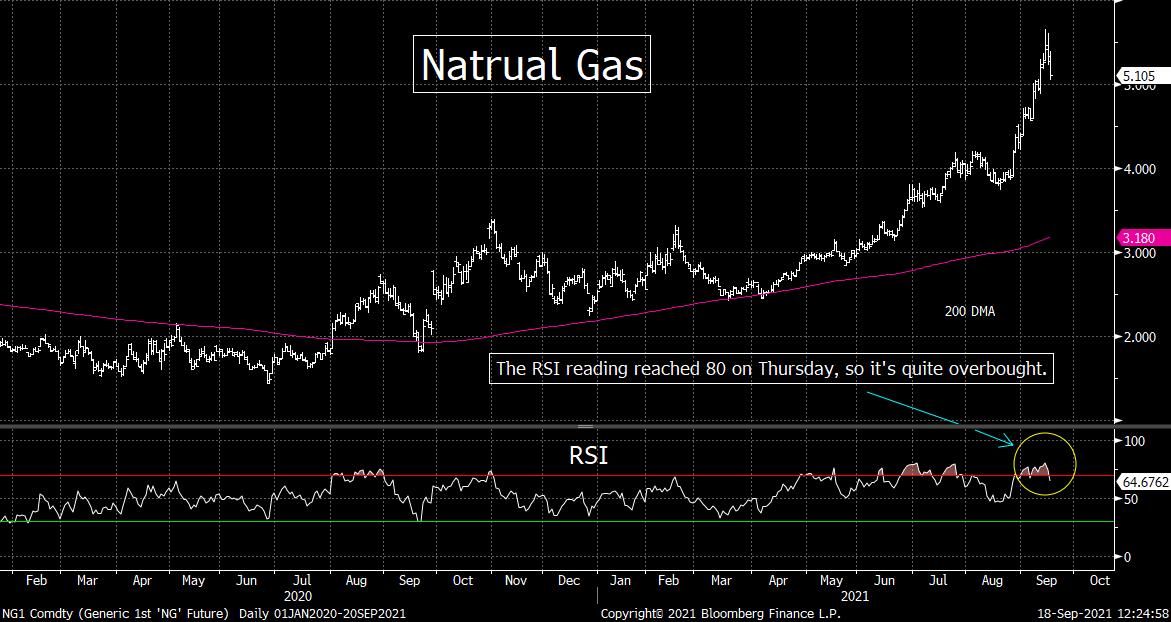

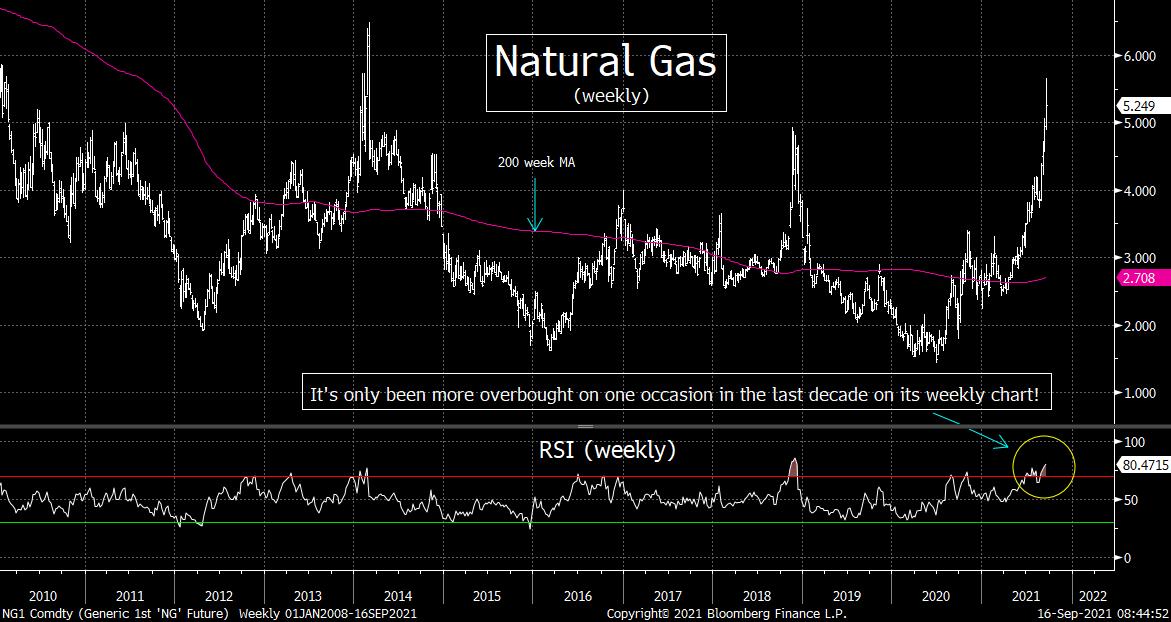

6) Between the lows of May and the highs of last week, natural gas had rallied over 130%! This was a spectacular rally, but now the commodity has become extremely overbought on a short-term basis. Therefore, even tough we are bullish on natural gas over the longer-term, we believe it will see a pull-back over the near-term…and thus investors should wait for a further decline before they buy the commodity or the nat gas related stocks before they add to positions.

Natural gas saw another big spike in the first half of last week. At its intraday highs on Wednesday, nat gas was about 130% higher than it was in early April…and more than 50% higher than it was just one month ago! Needless to say, this is a spectacular rally, but lets face it, natural gas is a commodity…not a tech stock!

In other words, this extraordinary rally was so strong that it took the commodity to a very overbought level on BOTH its daily and weekly RSI charts. Its daily chart closed at a reading above 80 on Wednesday…and so did its weekly RSI chart! It is trading a bit lower this morning, but we believe it has further to fall before it can digest the huge gains of the last month. Okay, natural gas has already dropped almost 8% since we originally made this call Thursday morning, but it still a LONG WAY from working off its overbought condition. Therefore, we still believe that it has further to fall…and thus investors should avoid chasing the commodity or the natural gas related stocks.

Again, we’re still bullish on natural gas on a longer-term basis. However, as our friend Nancy Tengler points out, there is still time before the winter demand increases (especially in Europe…who relies on imports). Therefore, we think investors and traders alike will be able to add to positions (or buy back the profit-taking shares) at lower prices in the coming weeks….once these extreme overbought conditions are worked-off much more than they have been over the last couple of days.

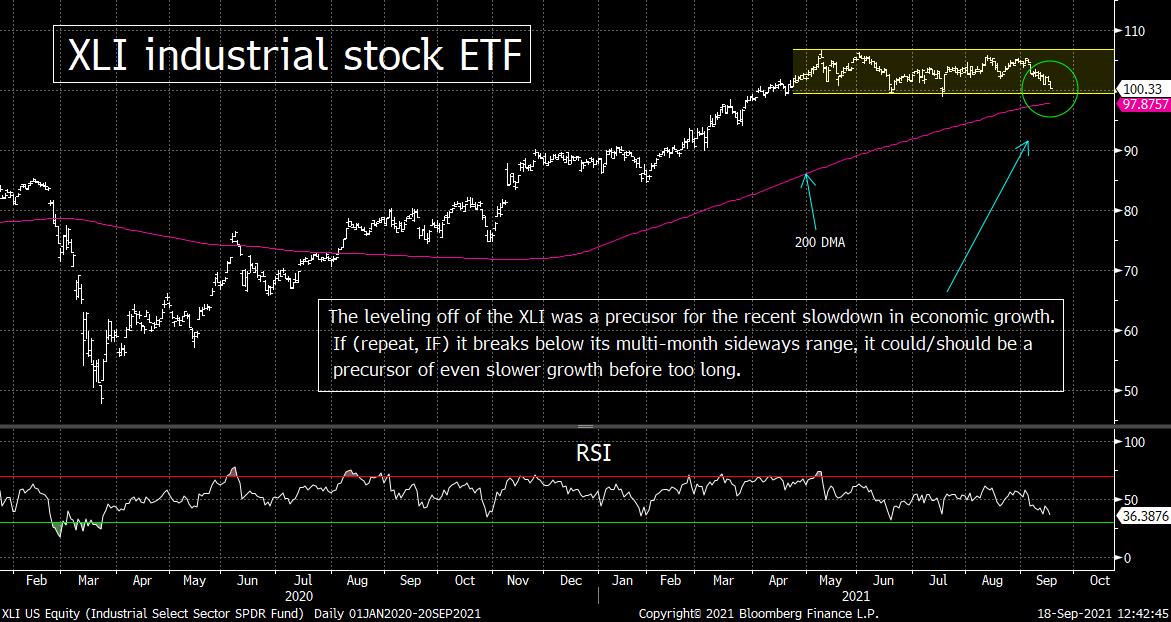

7) There has been a lot of talk about how any slowdown in growth over the rest of this year will reverse rather quickly once the delta variant dies down (soon). This might be true. We saw some better-than-expected data last week out of the Empire Manufacturing data, the Philly Business Survey, and Retail Sales. However, the industrial stocks are painting a different picture. If the XLI industrial stock ETF falls much further, it’s going to signal a change in trend for this key sector (and thus maybe for the economy).

We have talked a lot about the odds that “stagflation” will become a problem going forward. We believe that the supply chain driven jump in inflation will cause growth to slow…and we’re not as sure as others that the pandemic issue is going to move behind us quite soon. Of course, we discussed the supply chain-driven inflation issue in an early bullet point. As for the pandemic issue, we are not doctors. We have heard some experts say that the delta variant is peaking, but we’re heard others say that this variant (and/or other variants) will almost certainly create further problems as we move into the fall and winter months.

Again, we’re not doctors or scientists, but everything we’ve seen over the past year tells us that the situation gets worse as the weather gets colder. (We saw that again this summer…in the southern hemisphere…where it’s winter during our summer months.) Therefore, it’s very tough for us to think that the problems surrounding the coronavirus are going to move behind us…just at the weather STARTS to get colder. We’re not experts, but that scenario seems a big ridiculous to us.

One thing that we DO know, however, is that the XLI industrial stock ETF has been stuck in a sideways range since May. In other words, the fact that these stocks leveled-off in the spring and summer was a great leading indictor for the slowdown in growth we’ve seen recently. We do admit, the XLI only leveled off, it did not roll-over. Therefore, that move in the group was only indicating a mild slowdown…and that’s all we’ve seen so far.

However, the XLI is now testing the bottom line of the sideways range it has been in for the past five months. If (repeat, IF), if breaks below the bottom end of that multi-month sideway range, it will signal an important change in trend. This will be especially true given that this economically sensitive ETF has already broken below its trend-line from the March 2020 pandemic lows.

If the flattening out of the XLI was a good precursor for a mild slowdown in growth, it’s not out of the question that an actual breakdown in the XLI will be a good leading indicator once again. If it happens, it might just be telling us that we’ll see even weaker growth as we move towards the holiday season and into next year.

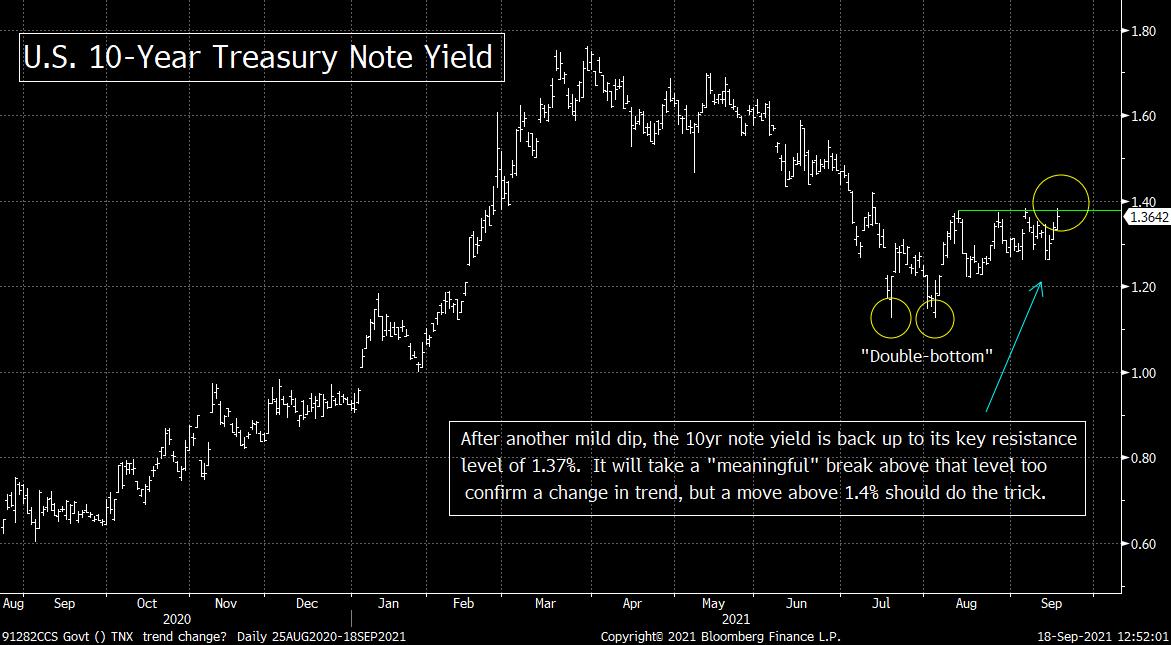

8) If the XLI falls further and it correctly signals that growth will slow even more, won’t that mean that interest rates will fall again? Well, in theory that’s true. However, if inflation turns into “stagflation,” we could easily see interest rates rise EVEN if the economy slows. (Besides, interest rates are already being kept artificially low due to the massive buy program of the Federal Reserve.)…..Either way, the yield on the 10yr note closed right at its key resistance level, so any further rise will confirm a change in trend for long-term interest rates on a technical basis.

To a certain extent, it’s silly that we on Wall Street try to determine the direction of interest rates based on the economic data in today’s world. Everybody knows that interest rates are lower than they would be if they were allowed to trade freely…without outside interference. If the Fed was not such a massive buyer (with zero price sensitivity), interest rates would almost certainly be higher. Therefore, unless the economy slows down in a major way, it should be considered LIKELY that long-term interest rates will rise EVEN if the economy slows down a bit over the coming months.

Another reason that long-term rates could rise would be if inflation turns out not be transitory. Interest rates rise during inflationary periods. We learned that in the 1970s, but history if littered with example of this. In other words, this is one of the few issues where economic theory and real-world history actually tell us the same thing. In fact, as we noted above, the higher rates that go along with inflation cause growth to slow. Therefore, those who think that slower growth will be bullish for bonds just might be misguided.

Either way, the yield on the 10-year note closed right at the key resistance level of 1.37% we’ve been harping on recently. It will take a “meaningful” move above that level to give us the confirmation we need to declare a change in trend for long-term interest rates. Therefore, it will likely take a move above 1.4% before we’d get too adamant about a “breakout” call on interest rates. However, there is no question that got back to that level very quickly. Thus, the sharp dip we saw after the CPI number was completely erased in just 3 trading days. So, this is something we all will need to keep a close eye on as we move into next week’s trading sessions.

One final comment: We don’t want to get too bearish on the bond market (bullish on rates) too quickly. If the stock market sees a deep correction like we think it likely will, it should cause a “flight-to-safety” trade. That will create some strong buying power for the U.S. Treasury market…at least for a while. However, a break above 1.4% will be a strong sign that the lows we saw in interest rates last year is going to be THE low for a very long time.

9) Politics: It’s becoming more and more evident that people from both sides of the political aisle have lost touch with what is going on in America today.

In our “Morning Comment” on Friday, we highlighted how former President Obama’s birthday bash and AOC’s appearance at a $35,000 a plate “gala” showed that the Democratic Party still doesn’t understand why they lost in 2016. The situation has not changed. Millions of Americans are sick and tired of the establishment in DC…and yet the Democrats keep following the same script.

However, we believe the GOP is making the same mistake. President Trump was considered an outsider back in 2016. Now, however, he is acting like an insider. His ridiculous vendettas against Republican who don’t kiss his ass make him look just as bad as all of those other DC “lifers” that he campaigned against in the last two elections. Besides, his past is littered with examples of what Obama is doing today. They both have shown us many times that our leaders in Washington believe that the rules don’t apply to them.

It’s funny, back in the summer of 2020, we asked the following question: We live in a country that has SO many smart, successful leaders. How in the world is it that the best we could do for our choice for President was Donald Trump and Joe Biden?

Leaders from both side of the political aisle (from both government and business) are guilty of following the mantra that the rules don’t apply to them. However, since the Democrats try to portray themselves as being the “party of the people,” they look much more hypocritical when dopes like Obama and AOC do stupid things. However, they are both guilty.

I am old enough to remember Vietnam, Watergate and the Iran Hostage Crisis. However, I was quite young, and thus I don’t remember how most adults felt about their elected officials back in those days. (We were more concerned sco

Recent free content from Matt Maley

-

THE WEEKLY TOP 10

— 10/23/22

THE WEEKLY TOP 10

— 10/23/22

-

Morning Comment: Can the Treasury market actually give the stock market some relief soon?

— 10/21/22

-

What Do 2022 and 1987 Have in Common?

— 10/19/22

-

Morning Comment: Which is it? Is stimulus bullish or bearish for the stock market?

— 10/17/22

-

Morning Comment: Peak Inflation is Becoming a Process Instead of a Turning Point

— 10/13/22

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464