THE WEEKLY TOP 10

THE WEEKLY TOP 10

Table of Contents:

1) Don’t blame the Fed if that stock market corrects at some point this year.

2) “Supply constraint” inflation is much different (and much worse) than “demand led” inflation.

3) Economic data could be more important than Jackson Hole this week.

4) Watching the chip stocks…especially TSM and NVDA.

5) The DXY dollar index stands at a critically important resistance level.

6) Dollar strength? Emerging markets look more vulnerable than commodities.

7) Looking at the charts of some ETFs. (HYG, SPAK, ARKK.)

8) Retailers earnings look good, but the charts on their stocks? Not so much.

9) Updating the charts on the SPY, QQQ and IWM.

10) Summery of our current stance.

1) Let’s start this week’s piece by commenting on the U.S. Federal Reserve. The Fed’s “minutes” caused a hiccup in the stock market last week…and the Jackson Hole Symposium takes place this upcoming week… so we want to review our stance on what we believe the Fed will do going forward and how it will impact the markets…….We do not necessarily believe that a “taper” move will cause the markets to correct. However, the lower level of liquidity that will result from a taper move will make is more probable that some other catalyst will finally cause the stock market to experience a 10% correction or more. Even if the stock market corrects, the Fed will be doing the right thing by pulling back on their stimulus.

First and foremost, if we see any weakness in the stock market in September and/or October (like we usually do)…and even if we see a correction before the end of the year (like we do almost every year)…we are all going to have to avoid blaming the Fed. The economy is no longer in an emergency situation, so we no longer need the kind of massive stimulus that the Fed has been providing for the past 17 months. Even if the variants cause many renewed curbs/restrictions…and it causes the economy slows a bit…the system will still no longer need the kind of stimulus the Fed has been providing since Mach of 2020.

It’s not the Fed’s job to keep the stock market rallying. In fact, if they keep the stock market keeps rallying even after it has become extremely expensive (like it has today), they will actually raise the risk of bigger problems down the road. It would create a bubble…and given today’s historic levels of corporate debt in the U.S. and around the globe…the bursting of a major bubble would create a crisis that would be even worse than the one we faced in 2008.

Sure, earnings are improving nicely, but they’ll never be able to take things to a fairly-valued level if the market keeps on rallying. A continued stimulus-fueled rally would merely generate a bubble. Besides, when a market has become as expensive as it is today, history tells us that the fundamentals have never been able to catch up to the market. The market has always fallen to make up the difference.)

Don’t get us wrong, we think it’s great that the Fed has considered the impact what a tapering move might have on the markets. (That’s why they have moved towards this decision in such a gradual way.) However, we cannot blame the Fed for fact that stock investors have not taken their obvious change in policy to heart. Bond investors actually have taken it to heart…at least somewhat. (Even though long-term rates are well below their highs for the year, they’re still much higher than they were a year ago…and higher than they were at the start of the year…when the talk of taper began.)

Last week, President Biden said that he knew all along that the American exit from Afghanistan would cause chaos in that country. Thankfully, the people at the Fed are smarter than President Biden, so they’ll never say anything that stupid. However, the Fed KNOWS that a tapering back of their massive levels of liquidity will likely pave the way for a correction in the stock market at some point in the coming months (even if it doesn’t happen until next year). Their taper move is very unlikely cause chaos…and the Fed can easily pivot if things start to get out of hand. (They’ll be smart enough to have a contingency plan…unlike the Biden Administration in Afghanistan.)

Therefore, we believe investors should also be prepared. Those who have a plan in place for what they’ll do if we see a correction in the coming months will be the ones who will be able to control their emotions when it takes place……..Either way, if we do indeed see a correction in the weeks/months to come, those who blame the Fed will really have nobody to blame but themselves.

2) Even if the economy slows down over the last four months of the year, it does not necessarily mean that inflation will also come down very quickly at all. The reason for this is that much of the inflation that exists in the system today has been induced by a lack of supply, NOT by an increase in demand. Therefore, a drop in demand will not give us as much relief on the inflation front as it has over the past four decades. In other words, the odds that we’ll get stagflation are higher than they’ve been for a long, long time.

The variants of the coronavirus are definitely having an impact around the globe. New Zealand announced a three-day full lockdown last week. NYC announced that you will need proof of vaccination to do just about anything in the public arena going forward. China has closed 25% of the third largest port in the world. President Biden is urging companies to institute mandatory vaccine policies. The CDC is advising at-risk people to avoid cruises. The list grows by the day. Heck, even the Fed just turned the Jackson Hole even into a virtual event late Friday afternoon.

These new lockdowns/curbs are raising concerns that economic growth here in the U.S. and around the globe will slow as we move through the rest of this year and into next year…..Of course, when growth slows, it usually means that concerns over inflation will decline. However, the key word in that last sentence was “usually.” This does not always happen. Growth and inflation “usually” rise and fall together because prices “usually” rise and fall due to DEMAND issues. HOWEVER, every once in a while, prices rise due to SUPPLY issues! When THAT happens, we get stagflation. When you consider what is going on in the world right now, we’re believe that stagflation is becoming the biggest risk to this bull market run right now.

Look at what took place in the 1970s. Oil prices shot through the roof. However, this had nothing to do with a big increase in demand (economic growth). It had to do with the decrease in the supply of oil (with OPEC’s oil embargo back then). Since oil price rose sharply even though there was not a big pickup in demand, it CAUSED growth to slow down!

When a big pick in economic activity causes prices to move higher, that’s fine. (It can be described as a healthy rise in prices.) If, however, the rise is prices is caused by a slowing of supply, it is not good at all. It actually CREATES lower demand….and results in a slowdown of economic activity.

We’re seeing a similar situation to what we saw in the 1970s right now. Instead of an oil embargo causing oil prices to rise (and thus the price of almost everything to rise) like it did in the 1970s, this time it’s pandemic and the disruptions in global supply chains that is causing a “supply-led” rise in prices. (It has been particularly pronounced for chips. If “chips are the new oil” the way some people say it is, our comparisons become even stronger.)

Many experts will say that these supply chain issues will subside soon, so we won’t have to worry about a “supply-based” increase in inflation for very long. However, the supply chain problem had already remained VERY elevated for a lot longer than people thought was possible BEFORE this most recent “wave” of the pandemic hit the world. Now, with China shutting down a major portion of the third largest port in the world, the supply chain disruptions are getting worse again. Therefore, it is very hard to know when these “supply” induced price increases will subside in a significant way. (Hope is not a good strategy to follow.)

Yes, we know, we know…a lot of commodity prices are falling right now. However, the drop in commodities overall has actually been rather muted. (More on this in point #6.) Besides, due to the supply chain issues, the decline in commodity prices is not going to lower prices for thousands of products as much as they usually would.

Okay, we do admit that there is a lot more that goes into explaining what takes place when we go through periods of “stagflation” than the simple description we have just provided. However, it is important to distinguish between a period of time when prices rise due to rising demand…and when prices rise due to declining supply. The latter periods tend to be tough ones for stock prices.

We do agree that this “supply chain” induced rise in prices is not likely to last as long as the oil embargo did in the 1970s. However, given how stretched valuations are right now, it won’t take a multi-year strain on the supply chain to keep inflation elevated enough to cause a correction in the stock market. It is likely that it will merely take the realization that supply chains will remain a problem well into 2022 to create enough concerns about stagflation to cause such a correction.

Going back to what we said in the previous bullet point, we can spend a lot of time blaming the Fed if the markets finally pullback this year. However, cutting back on emergency levels of stimulus after the emergency has passed is the right thing to do! (A correction in the stock market is NOT something that falls into the definition of an emergency!)

It is not the Fed’s job to keep the stock market rallying without a correction. Instead, we have to face that fact that SOME of the problems that were caused by the pandemic are going to linger for a long time. We have to stop looking to place blame on one person or one group if the stock market does not rally in a straight line. Instead, it is important that we face the realities that exist today…and are likely to exist going forward…and adjust our investment strategy accordingly.

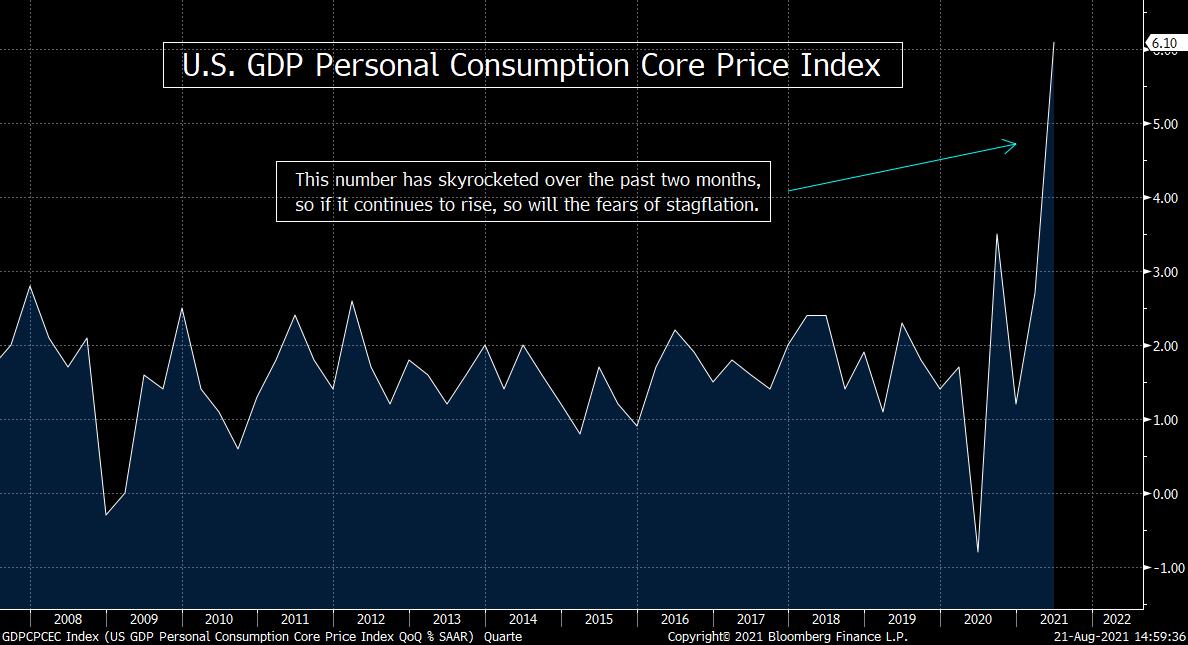

3) Okay, let’s wrap the first two points together in this third point…..Even though all eyes are going to be on the Fed’s big symposium in Jackson Hole next week, we’ll actually be watching two key data points. These data points could end up being much more important to how the markets react than anything that is said in Wyoming next week.

All eyes will be on the Kansas City Fed’s Jackson Hole symposium next week. However, we’re no so sure that there will be any market moving developments from that meeting. The Fed has already paved the way for an official tapering move, so although a further push in that direction is likely, it’s hard to think we’ll get any substantial “new-news.” Besides, it will be the last week of August…and thus the markets will be quite “thin” next week. The Fed does not like to create spikes in volatility…and any big “new-news” could create an outsized move in the marketplace…so we don’t expect many surprises from Chairman Powell & company.

This does not mean, however, that we won’t get any volatility. We do get a couple of key data points on the economic side of things next week. On Monday, we get the Markit U.S. Manufacturing PMI data. This number has been moving steadily higher all year, but they are expecting a mild dip this month. If the number comes-in even weaker than that (which is not out of the question with some of the lower-than-expected other recent data), it’s going to raise further concerns about economic growth going forward.

Then, on Thursday, we get the Core PCE (personal consumption core price index). This inflation gauge has spiked higher in a powerful way of the past two months. If it remains high…and especially if it rises even further…it’s going to fan the inflation fears substantially.

Needless to say, there are a lot of “ifs” in this scenario. However, there have certainly been several other numbers recently that have pointed to a continued rise in prices and a slowdown in growth. Therefore, if we get more indications that stagflation is gaining more steam, we could still see some volatility in the marketplace next week….no matter what takes place in Jackson Hole.

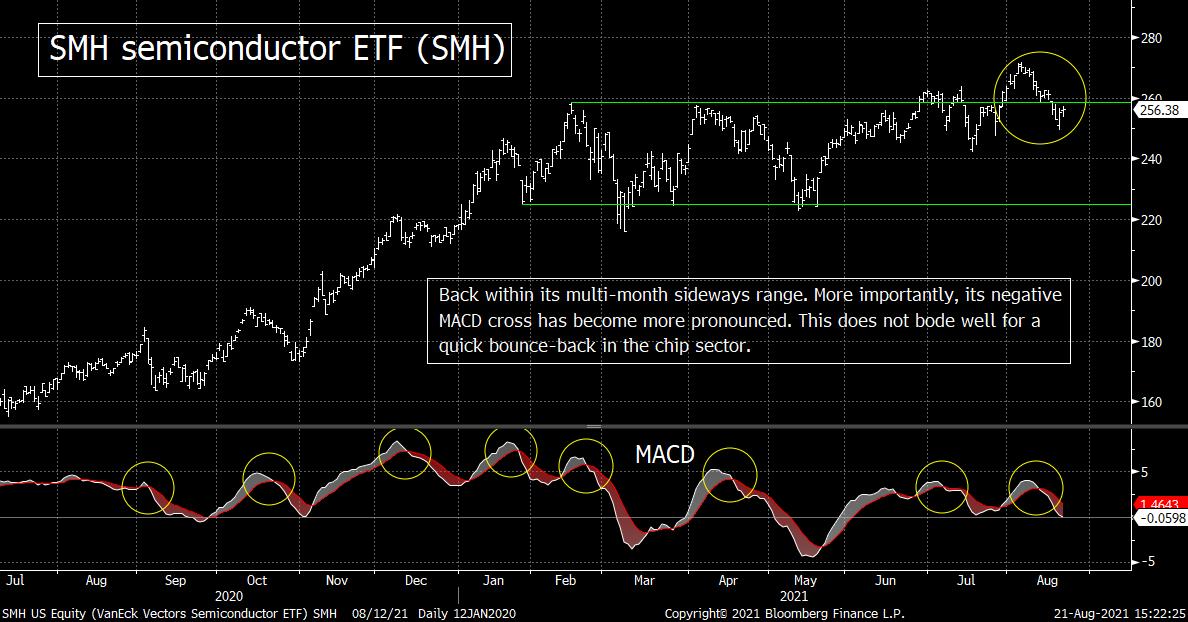

4) The SMH semiconductor ETF was able to bounce late last week, but it still remains more than 5% below its early August all-time highs. We are concerned about the fact that if it were not for one stock (Nvidia), this group would have fallen by more than it already has so far….NVDA didreport great earnings last week, so there are a lot of reasons to think that this stock can continue to hold up. However, given that many of the other important names in the group (like TSM, AMD, QCOM, INTC, LRCX, MU) are all down 11%-25% from their 2021 highs, it’s not a lock that NVDA can carry the full load going forward for this all-important leadership group.

We heard assurances from several experts in the semiconductor field last week that the chip shortages we are experiencing right now (and are causing loads of problems for so many industries) is going to wind-down by the end of this year. Although some (high end) chips will continue to have shortages, former Cypress Semiconductor CEO (TJ Rogers) says the shortage for most products will be over by the end of this year……However, other CEO’s (like the heads of Intel, Taiwan Semiconductor, Infineon, STMicroelectronics, etc.) say that the problem will remain a one for 18-24 months.

Given the increased curbs, restrictions/lockdowns that we highlighted in early points above…and stories over the weekend that say, “Science can’t keep up with the virus”…we wonder how anybody can really know when this issue will be pushed behind us……(Of course, some will argue that this will lead to higher prices for chips and that will be bullish for the semiconductor companies. However, if they don’t have the products to sell, the price increases are not going to help as much as some people believer right now.)

As we discussed last weekend, the SMH semiconductor ETF has developed a few cracks in it…and those cracks grew a bit larger last week after falling 4.5%. This decline took the SMH back within the sideways range it had been in since the first quarter…and its negative MACD cross became more pronounced. (That negative cross indicates a key loss of momentum…and it has been followed by material losses in the SMH on seven other occasions in the last year. That’s why we said last week that the group has formed some “cracks” even though it was very near its all-time highs.)

Since this group has been an important leadership group for the tech sector…and for the broad market as well…we’re worried that any further weakness (after the fall back into its sideways range) will be a signal that we’ll see a decent sized pickup in volatility going forward.

Last weekend, we highlighted Taiwan Semiconductor (TSM). Well, that stock did fall below its 200-DMA this past week…and is now testing its key support level of 108 (the lows from March and May and the bottom line of a “descending triangle” pattern).

It is getting oversold on a very-short-term basis, but if it breaks below 108 in any significant way (either now or after a short-term bounce), it’s going to be VERY negative for the stock. The fact that TSM makes up about 13% of the SMH, a breakdown in this name would not be good for the group either. (This is especially true given that several other important chip stocks have been very weak…with names like AMD, QCOM, INTC, LRCX, MU already down by 11%-25%!) Therefore, TMS breaks below that support level, it’s going to be tough for the rest of the group to gain any traction.

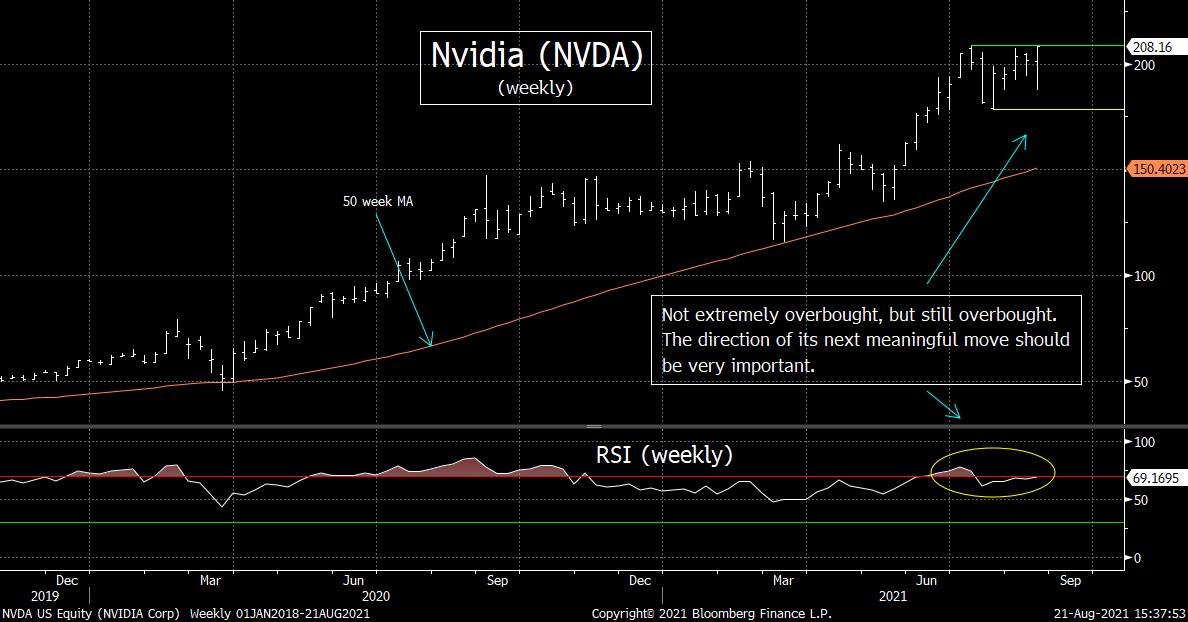

However, thankfully, another important stock (NVDA) continues to act very well. (NVDA has the second highest weighting in the SMH…at 10%.) They reported fabulous earnings last week. Therefore, even though it pulled back about 9% recently (from a very overbought condition), it was able to bounce back late last week and close at a new all-time high.

Our concern is that it’s going to be difficult for NVDA to carry all/most of the water for the group if those other stocks continue to slide lower. We’d also note that although NVDA was able to work-off some of its overbought condition earlier this month, it’s weekly RSI chart is still sniffing overbought territory. (It’s just not as extreme as it was a couple of weeks ago.)

Therefore, if it rolls-over any time soon, we’ll be watching its intraday lows from last week. If it breaks below 187.50, that will also take it well below its 50-DMA…and it could/should create some further weakness in the stock. NO, that kind of move would NOT raise a big warning flag on NVDA, but it could create the kind of weakness that would cause some further problems for the SMH…given how so many other important stocks in that ETF have been acting so poorly in recent weeks.

Of course, if NVDA can rally further…and break more meaningfully above its July highs…it will be quite bullish for the stock. So, we don’t want get too concerned about this situation…too quickly. However, we will continue to watch the SMH, TSM, and now NVDA…very closely as we move through (and past) Labor Day. How this group acts should be very important for the rest of the market during the seasonally tough months of September and October.

5) The dollar closed RIGHT AT its KEY resistance level on Friday. Any further significant strength will give us an important signal that the downward sloping trend that the dollar has been in since March of 2020 has changed.

The DXY dollar index was able to hold its January lows back in May…and this created a nice “double-bottom” for the greenback. Since then, the dollar has risen in a slow and steady fashion and that has taken the DXY above its trend-line from the March 2020 highs. Now, it has broken slightly above its highs from early April of this year. So, if the DXY can rally further, it will follow the upside break of its trend-line with an important “higher-high.”

Therefore, the equation for the dollar looks like it’s adding up to bullish very one: A double-bottom + upside break of a key trend-line + an important higher-high = confirmation of a change in trend.

HOWEVER, the “higher-high” has only been a very slight one so far, so we need to be careful. The daily RSI chart on the DXY is getting near overbought levels. That said, its weekly RSI chart has not yet reached an overbought level, so the dollar could still rise further over time.

In other words, we could see a pullback or a breather in the greenback soon, but if the DXY is able to break above the 93.5 level in any significant way over the coming days and weeks, it’s going to be a very compelling development. We’re merely trying to say that we don’t want to get ahead of ourselves. We HAVE to wait for a meaningful break above that key resistance level before we can confirm that the trend for the dollar has indeed changed to the upside…but the potential is definitely there.

6) Needles to say, if the dollar breaks-out and confirms a change in trend to the upside, it’s going to be very bearish for emerging markets…and for commodities as well. (The problem is that an important part of the concerns over inflation don’t have a lot to due with the price of commodities. Inflation could remain high even if commodity prices do not rise in a material way.)

Since the vast majority of commodities are priced in dollars…and since many/most emerging market economies are commodity based…there is a strong inverse relationship between the dollar and emerging markets and (most) commodities. Therefore, if the DXY dollar index confirms a change in trend, it’s going to be bearish for these two asset classes.

Back in July, we highlighted the chart of the EEM emerging markets ETF, showing that it has been range-bound since February. However, over the past couple of weeks, the EEM has broken well below that sideways range (and well below its 200-DMA), so this asset class is already seeing some seriously negative action. We do need to note that the EEM is getting oversold on a short-term basis, so it could bounce on a very-short-term basis. However, a lot of damage has already been done, so if the dollar climbs further in the coming days or weeks, this asset class should be avoided.

In other words, we do not think investors should be buying emerging markets on weakness right now. When you get the kind of change in trend that we’re seeing in the EEM right now, it usually signals a change in trend that will last for a while.

The situation for commodities is similar, but not as severe (at least not yet). If you look at the Bloomberg Commodity Index, it has definitely seen some weakness over the past three weeks. However, even though a few commodities (like lumber) have seen dramatic declines, this broad index has only dropped 6.5%. This commodity index also remains above its trend-line from the March 2020 lows, so the decline in commodities has not been as significant as it might seem to most investors.

The level we’ll be watching on this commodity index is 90. A significant break below that level would take it below that 17-month trend-line AND give it a key “lower-low.” Therefore, a break below 90 would be quite bearish for this asset class.

So as you can see, the situation facing the emerging markets is more acute than it is for commodities right now…as the EM’s have already seen some important technical damage. That said, a confirmed change in trend for the dollar will still be negative for both asset classes.

7) We thought we’d use one of the bullet points in the middle of this weekend’s piece to highlight the charts on three different ETFs. This bullet point will be less on words and more on pictures, but we’ll touch on the charts of the HYG high yield ETF, the SPAK Next Gen SPAC ETF, and the ARKK Ark Innovation ETF…..They are all either testing or close to testing key support levels.

The HYG high yield ETF has fallen below its trend-line from last September this month. It did the same thing in July for two days, but it quickly regained that line. This month, however, it has stayed below that trend-line…and it is now flirting with an important support level. If the HYG breaks below the 87 level, it will take it below its 200-DMA…and (more importantly) give it a key “lower-low.” (It has bounced off the 87 level three times in the past month, so if it finally breaks below that level, it will be a compelling technical development.)……Don’t get us wrong, a break below 87 will not be a major warning signal, but it will begin to raise some concerns about the direction of this important asset class.

The SPAK Next Gen SPAC ETF rallied 55% from the 2020 election until mid-February. However, it has given back all of those gains over the past six months. It is now testing the $22 level…which provided strong support for this ETF in October of last year and in May of this year. This ETF has been around for less than a year…and it’s getting oversold…but if it breaks below that $22 level in any meaningful way over the coming weeks, it’s going to raise some serious questions about the intermediate-term prospects for the SPAC vehicle.

The ARKK Ark Innovation ETF has had a rough year. It does stand 15% above its May lows, but it is also down 7% YTD and down more than 25% below its February highs……Back in the spring, the ARKK fell below its trend-line from March 2020. It got RIGHT UP to that line this summer, but it failed to break back above it. Instead, it has rolled-back over.

It is now testing its July lows, so any further downside movement will give it a mini “lower-high/lower-low” sequence since failing to regain that trend-line. Also, it recently made a negative cross on its MACD chart at a “lower-low”…which tells us the momentum it was trying to regain late in the spring and early in the summer is waning…….It will take a break below the May lows of $100 to raise a major red warning flag on ARKK, but it won’t take much more weakness to raise a yellow one.

8) Last week was a big week for earnings out of the retail sector. For the most part, those earnings were quite good. However, both the XRT retail ETF finished the week lower than they started. The reason for this seems to be concerns over the Covid variants and inflation. We talked about this in previous points, but we want to look at the technical picture of this important consumer related group.

Just over a week ago, the University of Michigan Consumer Confidence number came out and it was MUCH weaker than expected on Friday…and the Covid and inflation concerns seem to be the main culprits. This past week, we got the earnings reports from many different retailers…and most of them were quite good. (Some of them were excellent.) However, it was not enough to give the retail stocks as a whole much of a boost. In fact, the XRT retail ETF actually declined last week.

We need to point out that last week was not the first mediocre week these stocks have seen in recent months. One thing that might surprise a lot of people is that despite all of the talk about the strong U.S. consumer, the retailers have badly underperformed the broad stock market over the past five months! No, the XRT retail ETF has not declined…but it has only rallied 1.3% since mid-March…while the S&P 500 has rallied over 12%!!!

This action has led the XRT to form a “rising wedge” pattern. Therefore, if this group sees any further material weakness, it will take the XRT below this pattern…which would be quite bearish on a technical basis. (That’s right, even though the term “rising wedge” has the word “rising” in it, those wedges tend to have bearish outcomes. The exact opposite is true for “falling wedges.”)

In other words, the consumer has been strong all summer…but we don’t want to get ahead of ourselves. Even though the XRT has been underperforming for several months, it has been doing so by trading sideways…while the rest of the market has been rallying. However, it’s disappointing that last week’s news was not enough to give the retailers a lift. When you combine this with the previous week’s consumer confidence number…it has raised our concerns this key economically sensitive group material way.

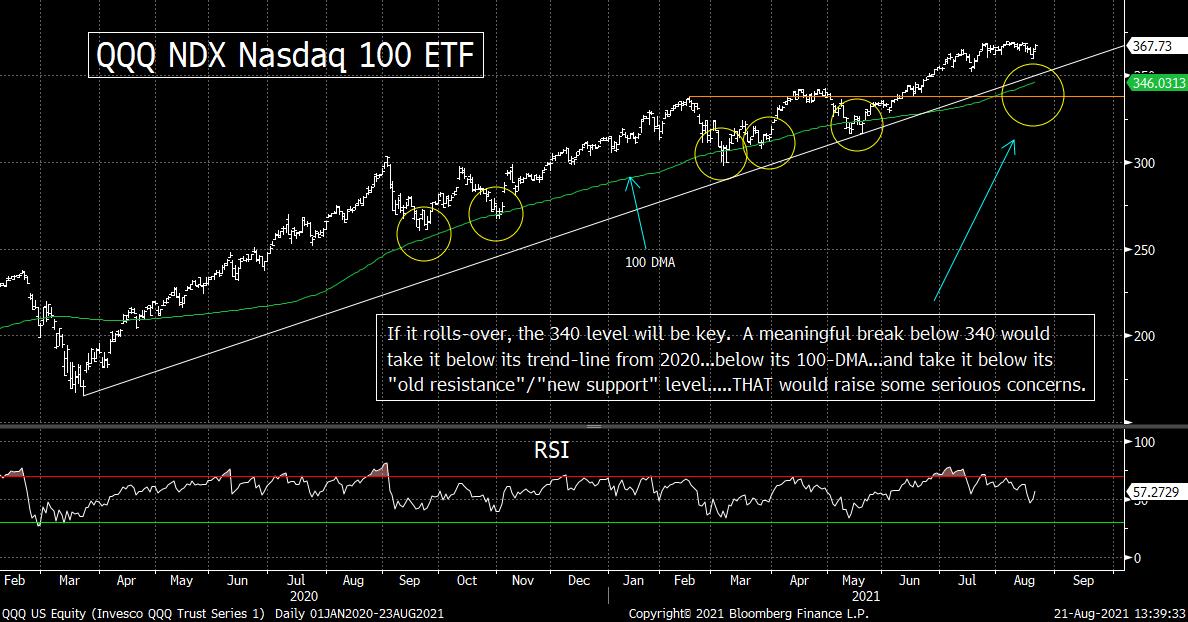

9) We haven’t looked at the charts on the major indices much recently. With the seasonally rough months of September and October just around the corner, we thought it would be a good time to update them. Instead of using the S&P 500, the Nasdaq and the Russell 2000, we’ll use their ETFs (the SPY, QQQ, and IWM). (Actually, we’re going to start with the QQQ.) The SPY and QQQ look quite good…with a string of “higher-lows/higher,” but the IWM looks a bit more problematic…..Of course, with EVERYBODY talking about Sept/Oct, we might not see any problems at all. However, if we do, there will be some key support levels to keep any eye on for all three of them:

The NDX Nasdaq 100 ETF (QQQ)…..The tech laden QQQ has been hovering near its all-time highs for about a month now, but it might have received the kiss of death over the weekend…as the cover story on Barron’s is titled, “The Unstoppable Rise of Big Tech.” (For those who don’t know the “Magazine Cover theory,” whenever anything makes the cover of a major magazine, the trend has already become quite mature…and tends to end shortly after making those cover stories.)

Anyway, unlike the SPY, the QQQ has actually seen a correction this year. It fell over 10% from mid-February into early March. It also saw a drop of over 7% in April/May. Thus, this part of the market has been more volatile that the S&P this year…but that should not be a surprise to anyone.

The QQQ got down to its 50-DMA on an intraday basis Friday morning, and it bounced off that line quite nicely. However, the 50-DMA has not been as important as the 100-DMA for the QQQ this year, so we’ll be watching that line more closely if the market pulls-back any time soon.

Actually, we’ll be watching the 340-350 range on the QQQ…because if it breaks below the 340 level in any meaningful way, it will mean that it has broken three different support levels. The 350 level is where the trend-line from March 2020 comes-in. The 346 level is where the above-mentioned 100-DMA comes-in. Finally, the 340 level was the high in both February and April, (so that “old resistance” level has become a “new support” level).

A break below the lowest of those three levels will only take the QQQ’s down by about 7%, so that 340 level is not some sort of major “line in the sand” for the NDX Nasdaq 100 ETF. However, a break of that level would definitely scare some of the more highly leveraged players…and the situation could snowball from there. Thus, we’ll be watching that level very closely if (repeat, IF) we see any pronounced weakness in the months ahead.

S&P 500 Index ETF (SPY)…&

Recent free content from Matt Maley

-

THE WEEKLY TOP 10

— 10/23/22

THE WEEKLY TOP 10

— 10/23/22

-

Morning Comment: Can the Treasury market actually give the stock market some relief soon?

— 10/21/22

-

What Do 2022 and 1987 Have in Common?

— 10/19/22

-

Morning Comment: Which is it? Is stimulus bullish or bearish for the stock market?

— 10/17/22

-

Morning Comment: Peak Inflation is Becoming a Process Instead of a Turning Point

— 10/13/22

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464