THE WEEKLY TOP 10

THE WEEKLY TOP 10

Table of Contents:

1) Tech is too overbought to rally much further for a while.

2) However, AMZN could/should still outperform.

3) Chip stocks at key juncture with Taiwan Semi reporting this week.

4) Treasury yields are very likely to rise in the second half.

5) As yields rise, banks should outperform once again.

6) Moderating growth will not cause LT yield to fall further.

7) It’s going to be a different earnings reporting season this July.

8) Small-caps need to play catch-up…or it will raise a yellow flag.

9) We’re still cautious near-term on energy (but still bullish LT).

10) Summary of our current stance.

1) We got a bit of a hiccup in the stock market on Thursday, but it was able to bounce back later that day…and then recover the rest of the losses (and then some) on Friday. However, the bounce-back in the tech group was not quite as pronounced. There are reasons on both the fundamental and technical side of things that tell us that the tech groups is unlikely to continue its recent outperformance as we move through the month of July.

The stock market was able to rebound from its pull back on Thursday, however the XLK technology ETF was not able to bounce-back as strongly as the rest of the stock market. This underperformance is not major divergence yet by any stretch of the imagination, but there are some reasons on both the fundamental and technical side of things that lead us to believe that the tech group is likely going to have a tough time returning to the kind of outperformance is saw in the 6-7 weeks it did leading up to the July 4thweekend.

On the fundamental side of things, the White House announced that the President is going to sign an executive order that will increase regulatory scrutiny of the tech companies (and several other industries, like the drug companies). The consensus on Wall Street had become pretty complacent about the chances big tech would face serious regulatory challenges this year, so this news caught some people off guard. Well-known tech venture capitalist, Jason Calacanis, said last week that this was a “big turning point” in terms of regulation…and that the federal government was is now turning up the heat on the big tech companies that the government sees as becoming too big……..More regulation means higher costs…which means lower profits. Thus, this is certainly a negative development on the fundamental side.

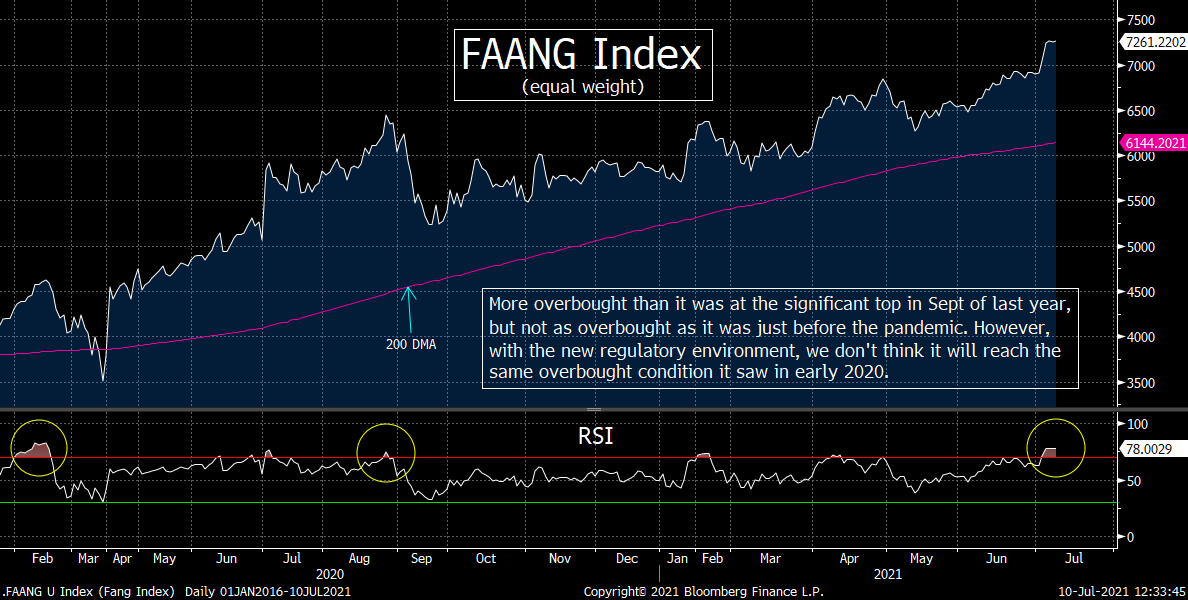

This new development could/should present some meaningful problems for the group over the near-term because on the technical side of things, the group had become quite overbought after its very nice rally during the previous several weeks. As we highlighted in recent pieces, stocks like NVDA, MSFT, AAPL, GOOGL, INTU, NET have all become quite overbought on a short-term basis. The Nasdaq Composite index and XLK technology ETF have also become overbought as well.

Of course, some are more overbought than others, but the broad XLK had certainly become quite overbought…and we could say that stocks like AAPL and NVDA had become boarder line extreme in their overbought conditions. (First 3 charts below.)

We have said many, many, many times that NDVA and many of the other overbought tech companies are GREAT companies. However, the stocks of these great companies can frequently get ahead of themselves on a short-term basis (and sometimes even on an intermediate-term basis). Therefore, we are not saying that long-term investors should dump these names in an aggressive manner. However, they should avoid getting overly aggressive on the buyside in these names over the near-term…and they should at least consider paring back the size of some of their holdings.

In other words, with the tech sector now facing headwinds on both the fundamental and technical side of things, we believe that FOMO should not be a big concern in many of these tech names over the near-term. We believe that no matter what happens in the broad stock market over the next few weeks, the tech stocks are so overbought that they’re very unlikely to run away from us at these current overbought levels. (4th chart below.)

Yes, we understand that this stance goes against what the consensus thinking is right now. The big cap tech names (especially the FAANGs) have regained a lot of the glimmer they held last summer. However, we are going to bet against the consensus right now…and suggest that people fade the “big tech” trade…as least for the next several weeks.

2) Ok, what does this all mean for AMZN? The stock broke out of the range it had been in for almost a full year recently. Do our concerns about new regulatory pressures lead us to think that AMZN will give up some of its recent gains soon? Well yes, but the there is a scenario that is still quite bullish for this particular stock. (The FAANGs don’t always trade in unison…as we have seen with GOOGL’s strong performance this year…while most of the other FAANGs were range-bound for so long.)

AMZN broke out of the sideways range it had been in since last summer this past week…and it did so in a meaningful way. Thus, this should be a very bullish development for AMZN’s stock on a longer-term basis (and even an intermediate-term one). However, the stock is getting quite overbought on a short-term basis. It is very close to the same reading on its RSI chart that was followed by pull-back over the past 16 months, so it could/should be due for a short-term pullback right now as well.

However, this would not be a big problem at all…given that the stock has rally 17% over just the past four weeks. In fact, it would be normal and healthy if it took a breather to work-off some of this overbought condition.

What we’ll be watching is to see if the stock can hold in the 3,500-3,550 range on any near-term pull back. That was the top end of its former sideways range, so if it does indeed pull-back and tests that level…but it able to hold it…it will be very bullish for AMZN. Of course, if it quickly falls back below the 3,500 level in a meaningful way, it’s going to tell us that the execuative order signed by President Biden is an important enough development to offset the recent positive technical move in the stock. However, it seems to us that no matter what happens to the rest of the tech group, AMZN should do quite well in the second half of the year. (The FAANGs don’t always trade in unison. GOOGL rallied VERY strongly from its late September lows of last year…while the rest of the FAANG names badly underperformed for many, many months.) Therefore, AMZN could easily rally further…even if the rest of tech underperforms going forward.

3) Of course, a big determinant for whether we’re correct in our cautious stance about the tech sector at this time will be the action in the semiconductor stocks. Even though the broad tech sector has made nice new highs in recent weeks, the chip stocks have not. Therefore, whether this important group within the tech sector can also breakout soon or not should be very important over the coming days and weeks.

The semiconductor stocks have been a VERY important leadership group for the tech sector over the years (and an important leadership group for the broad stock market as well). The SMH semiconductor ETF has been lagging the broader tech sector (and the broad stock market) in recent weeks. However, this is not a big concern yet. The SMH had outperformed the broader XLK tech ETF for many months leading into June, so one could say that the rest of “tech” is merely playing catch-up with the chip stocks.

However, if the underperformance of the past 5-6 weeks continues, it’s going to raise some warning flags. Let’s face it, even though the chip stocks had been outperforming for many months, the SMH has still not broken above its highs from February in any meaningful way. Therefore, the vast majority of its outperformance came late last year and very early this year! With this in mind, if the group fails to breakout once again…and rolls-over in any significant way, it’s going to strengthen our view that the tech sector’s recent outperformance is behind us for a while.

The catalyst for a move in either direction could very well come next week. Taiwan Semiconductor (TSM) reports earnings on Thursday. TSM has the largest weighted of any stock in the SMH…at 14.42%. Therefore, any outsized reaction to its earnings report should have an important impact on the entire group.

We will note, however, that the downside potential is likely higher than its upside potential. As we highlighted in point #1, NVDA has become extremely overbought…and it has the largest weighting in the SMH (14.42%). Since NVDA is ripe for a further decline, a negative reaction in TSM would leave 25% of the SMH falling in a meaningful way at the same time. THAT would not be good for this all-important leadership group. Thus, if TSM cannot rally off its earnings report…and cannot offset a likely further pull back in NVDA…a big warning flag could (repeat, COULD) be going up later this week.

4) The tech sector is not the only part of the market place that has become overbought…as the Treasury market became very overbought last week as well. The TLT Treasury ETF (which measures price, not yield) became the most overbought it had been since the March 2020 highs (when people were buying Treasuries hand over fist in a “flight to safety” move during the peak of the pandemic panic in the markets). Conversely, the RSI chart on the 10yr yield became the most oversold it had been since March 2020. Therefore, the pull-back in yields and the bounce in rates should last for more than just a few days.

There have been a lot of reasons sighted for why the yield on the 10yr note had fallen so much in recent weeks. This debate has been quite interesting because there haven’t been many signs of slowing growth or waning inflation to account for this move. Yes, there are growing concerns about the Delta variant of the coronavirus…and there have been some weaker than expected economic data points (like the ISM services number last week). However, now that a lot of the U.S. has been vaccinated, it’s way too early to draw many conclusions about another major economic lock-down…and the data has only been slightly weaker. Therefore, it’s hard to justify the recent big drop long-term interest rates on a fundamental basis. Instead, it seems like the “positioning” issue has been the culprit…as too many people were looking for a further steepening of the yield curve…and were forced to unwind those positions.

Since the outsized drop in long-term rates seems to be technical in nature, rather than fundamental, we believe that the recent move will be quite short-lived. In fact, we believe that the Treasury market will roll-over (and yields will rise). If you look at the TLT Treasury ETF (price), it became quite overbought last week on its RSI chart. It also got up to its 200-DMA and rolled over. We saw a very similar situation in the yield on the 10yr note…in the other direction. It became very oversold. No, it did not get all the way down and test its 200-DMA, but it did bounce off its oversold condition on Friday. (We’d also note that the bullishness among futures traders in the DSI data hit 90% for T-bonds on Thursday night, so extreme bullish sentiment is another reason to think that bond prices will decline soon and that bond yields will climb over the coming weeks.)

Of course, if the bounce in yields becomes pronounced…and it lasts for an extended period of time (which we believe is likely), it’s going to be yet another reason to think the tech group will not continue to rally to the same degree it has recently……

5) You don’t have to be a genius to know that any meaningful and lengthy rise in rates should be bullish for the bank stocks. The KBE bank ETF did break below its key support level mid-week last week, but it was able to regain that level by the close Friday. Since we think that rates will head higher over the rest of the year, this should be a good level to get more aggressive in the bank stocks right now.

As the decline in interest rates took place in recent months, the bank stocks began to underperform the market (after 6+ months of outperforming). Given that we believe that rates have bottom and will rise in the second half of the year, it should bode well for the bank stocks once again.

We’d note that the KBE bank ETF had become quite oversold on its RSI chart by this past Thursday…and it had become extremely oversold on its Bollinger Bands chart. Therefore, at the very least, the group should be ripe for a nice bounce over the near-term. However, since we believe that long-term rates are headed higher, we think the rally will have legs.

We’d also note that although the KBE broke below the key $50 support level that we’ve been harping on, it was able regain that line by the end of the week. Therefore, if it can continue to bounce, it will show that the mild and quick break below $50 was merely a head fake…and that the rally in the banks could/should have legs.

The one concern, however, is that the bank stocks have been notorious for selling off after their earnings are announced…in a “sell the news” reaction. With many key bank companies reporting next week, it does raise the odds that we’ll get another disappointing reaction to their earnings reports. That said, the KBE is coming off an oversold reading this time around…while it was overbought at the time when the last three earnings seasons began. Therefore, we are not overly concerned about their earnings reports…especially since they did well on their CCAR results just recently………So as you can see, it is our belief that we’ll see a return to the “value over growth” trade that had taken an hiatus recently.

6) It was really weird how the stock market went from moving in the opposite direction from long-term yields to the same direction so suddenly last week. However, we believe that this will not last very long and we’ll revert back to the correlation that has worked most of this year. Our stance on this issue derives from our belief that interest rates will not move due to economic factors going forward. Rates are artificially low…and thus they should head higher EVEN if growth expectations moderate as we move through the second half of this year and into next year.

It is amazing how the stock market’s reaction to the moves in Treasury yields have made a major 180 degree turn in the last week or so. The stock market went from rallying when yields went down and dropping when yields rose…to just the opposite. We’re afraid that this abrupt change is another sign that fundamentals matter very little in today markets (where the Fed has kept emergency levels of stimulus flowing…despite the fact that we are no longer in an emergency situation in neither the economy nor the markets).

The problem, in our opinion, is that too many pundits keep trying to identify fundamental reasons for many of the moves in the bond market. We think they are wasting too much time on this exercise. Don’t get us wrong, changes in the trajectory of growth DO have an impact on the Treasury market…but only on a very limited basis. The most important catalyst for any movements in bond yields (by far) is central bank intervention.

The bond market is manipulated. THIS IS NOT SOME SORT OF CONSPIRACY THEORY! The fact that the Fed and other central banks are engaged in QE programs is the definition of manipulation! These central banks buy the bonds in their QE programs every month with absolutely no regard for price. Most investors spend a lot of time deciding whether an asset is cheap or expensive when they’re deciding whether they’ll buy it or not. QE programs do not consider this issue at all. So it IS manipulation.

There is nothing wrong with this. They didn’t engage in this massive intervention so that the Fed could profit. The Fed & other central banks NEEDED to engage in this sort of manipulation because the global economy had basically shut-down entirely and the credit markets had frozen up. However, we are no longer in an emergency situation in the economy and the markets, so we no longer need emergency levels of stimulus (manipulation).

In other words, those who say that it looks like growth will moderate in the second half…and thus this means that interest rates will fall are WAY off base! Interest rates are at artificially low levels!!! Therefore, EVEN IF THE ECONOMY MODERATES GOING FORWARD, interest rates will rise if/when the “price insensitive” buyers become less aggressive!!!

This is a long-winded way of saying we totally disagree with those who believe that interest rates will fall further because the economic growth is showing signs of stalling out. (Do these people really think that interest rates would be where they are today if the global central banks were not supporting the bond markets is a MAJOR way???) Heck, even the employment picture is MUCH, MUCH better than it was 12-15 months ago. So even though the Fed would like to see more improvement in this area, they are going to have to “taper” sooner rather than later. THAT is going to cause interest rates to rise from current levels as we move through the rest of the year and into next year in our humble.

Of course, this does not mean we cannot fall slightly below last week’s low at some point soon. Chairman Powell speaks in front of Congress next week and if he continues to follow the same script, he’ll be quite dovish once again. However, there is a very prominent article in Barron’s this weekend that involves an interview with Dallas Fed President Kaplan. He is very emphatic in saying that “we are going to achieve ‘substantial further progress’ sooner than people think”…and that they’ll taper “sooner rather than later.” That interview does not say anything new about Mr. Kaplan’s perspective, but anyone who thinks that he is strongly reiterating his stance without the knowledge of Chairman Powell is kidding themselves.

Therefore, we believe that the drop recent drop in interest rates is just noise (“positioning noise”)…and they’ll be heading higher soon. It might not happen next week, but it’s coming. In fact, we are confident that we’ll see 2% before we see 1%...and that the only way we’ll get to 1% again is in another emergency situation. (Thus, we hope it never happens.) In our opinion, the move from 1.5% to 1.3% was a major head fake. So when it comes to the bond market, caveat emptor.

7) We are headed into earnings season and this one is very different than we usually experience when we go through the Q2 earnings reports. It is our opinion that this earnings season will impact individual stocks much more than it impacts the broad market, but since it will such a different earnings season than usual, you never know what could happen.

The upcoming earnings season is going to be much different than we usually experience. In most years, earnings forecast for the year peak at the very beginning of the year…and then they are lowered as we go through the year. Therefore, when companies beat their (lowered) consensus estimates, investors do not get overly excited. They just say to themselves, “Great, XYZ beat their estimates, but they merely beat lowered estimates, so I’m not overly impressed.”

This time around, however, things are different. In fact, they’re A LOT different when it comes to the issue of earnings estimates. Instead of lowering estimates this year, analysts have been raising them (in aggregate) all year! They’ve risen by more than 15% since January (from $166 to $191). Therefore, if companies can beat their consensus estimates in any significant way, they should be rewarded in a more meaningful way this time around.

Second of all, this particular earnings season is going to be the first one in quite a while where we’re going to get a decent amount of forward guidance from a lot more companies. For over a year, many companies have refused to issue forward guidance…for the simple reason that they had no idea what their future prospects looked like due to the global lock-down. (This was a very legitimate excuse for the vast majority of companies.) However, now that the economy is re-opening, many companies will be able to provide at least some sort of guidance. If that is quite good as well, this will be another reason for an individual stock to rally nicely………We can take this thought one step further. If a very large number of companies beat their elevated consensus estimates AND provide bullish guidance, it could cause the entire stock market to rally further (even though it has become very expensive).

Of course, this situation is a double-edged sword. If estimates have been raised too much…and guidance is poor (OR if companies continue to avoid giving guidance due to the Delta variant), it could cause investors to cry foul and start to pair back some of their holdings. Again, it’s an expensive market…so if the second half starts to look more uncertain (or even downright gloomy)…the broad market could sell-off in a meaningful way due to concerns over earnings growth.

(Again, if economic growth or earnings growth moderates, it’s not going to impact the bond market much. However, it could still impact the stock market…due to the fact that it has become extremely expensive.)

In other words, this is going to be a different reporting season than we usually see in the month of July. Therefore, it’s not out of the question that some stocks (especially ones that have been lagging…and are thus not overbought on a technical basis) could see a lot more upside movement this summer. Thus, our thinking is that if we get any “summer doldrums” this year, it won’t be in July.

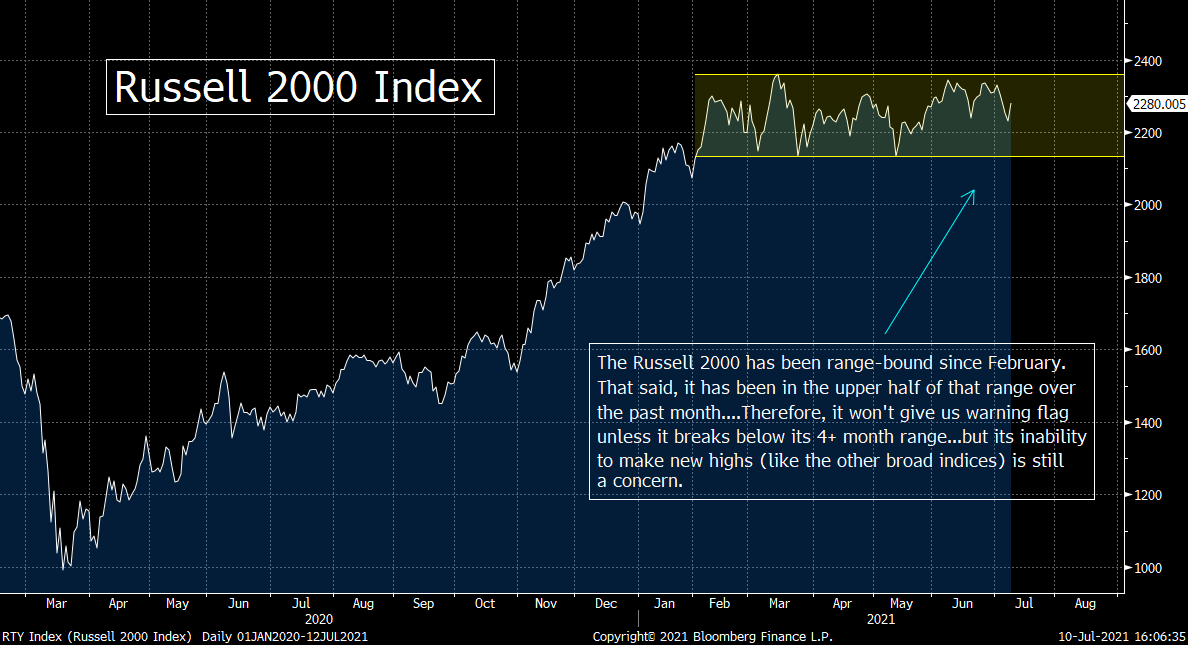

8) We spent a lot of time last week answer questions about whether we thought the recent drop in interest rates means that the economy and earnings are going to slow-down in the second half. As we just said above, we don’t think that’s why long-term rates fell so much recently (and why they won’t fall much further), but there is another reason to think that things might moderate in the second half. We’re talking about the action in the small-cap Russell 2000 Index.

As we highlighted in a previous point, we think the outsized rally in the Treasury market (and thus the outsized decline in long-term interest rates) was due to technical reasons. (Investors were caught offsides on the steepening trade in our opinion.) However, the continued malaise in the small-cap (domestically focused) Russell 2000 Index DOES add at least some validity to the argument that Q2 is going to give us “peak growth” and “peak earnings.” (We’re just saying that if it does, it will have a bigger impact on the stock market than on the bond market.)

Of course, even if we do experience “peak” anything, it does not mean that the second half of the year is going to be horrible. We’ve been saying for some time that we believe that whatever the high is for inflation this summer will likely be the high for the year, but we still believe inflation will stabilize at a level than was higher before the pandemic. Similarly, even if we see an economic/earnings “peak” this summer, it does not mean that the growth will not continue at a solid pace.

However, the fact that the Russell 2000 index has done absolutely nothing sine the middle of February is definitely a yellow warning flag on domestic growth. We do admit that the Russell has been able to stay in the upper half of its five-month range over the past four weeks or so, but it is well behind the rest of the major indices since the middle of the second month of the year! To be more specific, since February 8th, the Russell 2000 has fallen0.42%....while the S&P 500 has rallied 11.5%, the DJIA has tacked-on 12% and the Nasdaq Composite has risen more than 5%!

Again, since the companies in this index do most/all of their business domestically, the underperformance of the group can frequently give us an advance warning that the U.S. economy is going to slow and that the broad market is going to decline. That is what happened in 2018…when the Russell 2000 turned down about three weeks before the S&P did…just before the 19% correction in the stock market took place in the 4th quarter of that year.

That said, the Russell 2000 does not always lead the rest of the stock market lower. There are plenty of examples over the decades where the Russell turned lower at the same time the rest of the market durned lower. Besides, although the Russell has not done anything over the past five months, it has not broken down. In fact, as we just said, it has been in the upper half of its sideways range for a while now. Therefore, we’re going to have to see this small-cap index break below its sideways range (below 2135 on the Russell and $212 on the IWM Russell 2000 ETF) before we start raising any caution flags.

However, there is no question that the action in the Russell 2000 belongs on the bearish side of the bull/bear ledger right now.

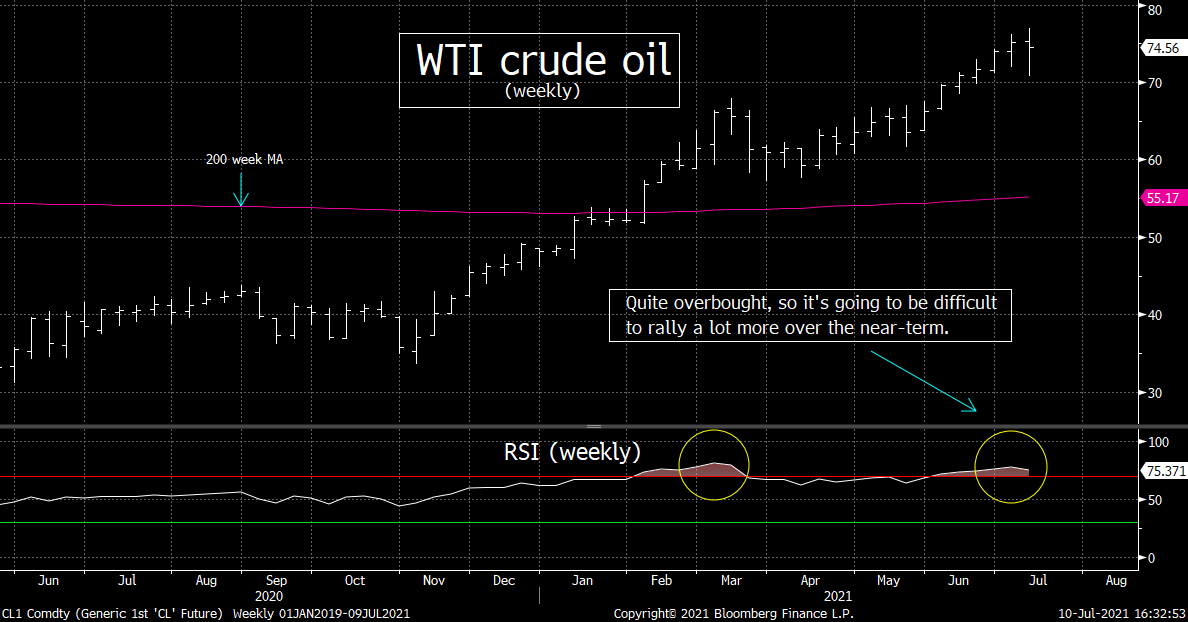

9) We just want to reiterate our stance on the energy stocks. We love them longer-term, but we still believe they will continue to take a breather over the shorter-term. We’re basing this belief on the technical condition of WTI crude oil…as well as the technical condition of the XLE and XLP energy ETF’s. With this in mind, we believe investors should continue avoid chasing the energy stocks at current levels and look to buy them on weakness later this summer.

In mid-June, we changed our stance on the energy stocks to a more cautious one…and we reiterated that stance last weekend. Since mid-June, the group has been stuck in a sideways range and has actually pulled-back by about 4%-5% in the past week…even though WTI crude oil has continued to rally since mid-June.

Therefore, this call has worked out quite well, but we still want to stay cautious/neutral on this group over the near-term. Crude oil remains very overbought…and although the XLE energy stock ETF and the XOP oil & gas ETF have both worked off SOME of their overbought conditions, we believe they have more work to do before they can break above their next key resistance levels (their 200-week MA’s).

First of all, the fact that the energy stocks have not rallied along with the price of crude oil is a warning signal. More importantly, however, crude oil has become quite overbought on its weekly RSI chart (much like it did in mid-March). Therefore, it’s becoming ripe for at least some sort of pull-back (just like it saw in the second half of March).

Second of all, both the XLE and XOP had become overbought on their weekly RSI charts…and began to roll-over last week. The fact that they got right up to their 200-week MA’s at a time they became overbought is another reason to think they’ll see a little more weakness going forward. (Many assets need to digest their rallies when they test a key resistance level for the first time. Once that takes place, the second or third rally is the one that finally lets it breakout in a significant way. In fact, that is the more bullish development. If it breaks out at a time it is also overbought, it frequently makes the breakout a less powerful one.)

Finally, we’re seeing the weekly MACD charts on these two energy stock ETFs are seeing negative crosses, so this is yet another reason to think that they’ll have to decline more before they continue on the great bull run that started last October…….Again, we believe the energy sector make higher-highs this year, but we just think that it could/should see more of a pull back before the higher-highs are made.

10) Summary of our current stance……We’ll start by saying that we did not get a chance to talk about the situation with China this weekend, but we’ll touch on it in one of our “Morning Comments” early next week……Anyway, the strong bounce off of its Thursday morning hiccup was very impressive for the stock market. Although Friday’s bounce came on very low volume, the breadth was excellent (8 to 1 positive on the S&P 500 and 10 to 1 positive on the NYSE Composite Index). Besides, Friday’s in July are days when the volume is pretty much always quite low. Therefore, given that the DJIA, the S&P 500 and the Nasdaq Composite were all able to close at new daily AND weekly highs last week, it looks like any correction in the stock market is not in our immediate future.

Having said this, our thinking is that the most important moves over the next few weeks are not going to be in the broad market indices. Instead, with earnings season beginning next week, the big moves will likely come in the individual stocks. We also believe that it will come in the movements of the groups.

We also believe that the recent drop in long-term interest rates is likely over…or at the very least, in the process of bottoming. The technical condition has become quite extreme (overbought on price…oversold on yield) and sentiment has become quite extreme as well. Therefore, since we think interest rates are very likely to spend more time rising than falling in the 3rd quarter (and through most of the entire second half of the year), we believe we’ll see a return of the outperformance of the banks/financials and an underperformance of the tech stocks. (The fact that the tech stocks became very overbought in the last week adds to our confidence on this argument.)

On top of all this, the stock market has become very expensive once again. It’s great that full-year earnings estimates have improved materially so far this year, but the P/E ratio on the S&P 500 is back up to 23x consensus forward estimates of $191. (Even if you use a $200 number for S&P 500 earnings, the ma

Recent free content from Matt Maley

-

THE WEEKLY TOP 10

— 10/23/22

THE WEEKLY TOP 10

— 10/23/22

-

Morning Comment: Can the Treasury market actually give the stock market some relief soon?

— 10/21/22

-

What Do 2022 and 1987 Have in Common?

— 10/19/22

-

Morning Comment: Which is it? Is stimulus bullish or bearish for the stock market?

— 10/17/22

-

Morning Comment: Peak Inflation is Becoming a Process Instead of a Turning Point

— 10/13/22

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464