THE WEEKLY TOP 10

THE WEEKLY TOP 10

Table of Contents:

1) Our belief in a nice year-end rally remains intact.

2) However, next year will be much tougher for this very expensive market.

3) Many non-FAANG tech stocks actually have more momentum than the FAANG’s.

4) The dollar, euro and Aussi dollar continue to be KEY indicators for the stock market.

5) The trend towards higher rates might not be over. (That will be good for banks.)

6) Healthcare ETFs breaking out!

7) Great run for Bitcoin, but it’s getting very overbought near-term.

8) U.S./China relations will remain very tense...due to Taiwan.

9) Greg Abbott will be the GOP’s nominee in 2024. (They can’t lose Texas!)

10) Summary of our current stance.....and THANK YOU VETERANS!!!!!!

Short Version:

1) When the market rallies sharply over a very short-time frame like it did last week, it can frequently be wrong to say it will continue. However, although we do think the market could/should see a very-short-term breather soon, we’re sticking with our call for a strong year-end rally. The market tends to rally at the end of election years...and year-end rallies tend to feed on themselves. More importantly, the Fed should continue to provide plenty of liquidity as we go through the newest wave of the coronavirus pandemic.

2) Even though we’re looking for a nice year-end rally, we think the market is 2021 is going to be tougher than people expect...because growth will not be strong enough to fuel a further rally in this already expensive market. A return to pre-Covid levels of growth won’t be enough...because the economy wasn’t very strong back then (in 2019)...and earnings growth was zero! We also don’t think any new stimulus policies (that are in addition to the one being negotiated recently) will be back-end loaded, so it won’t kick-in soon enough to help the economy much next year.

3) There was a lot of talk last week about the rally in the mega-cap tech stocks. There’s no question that it was a strong rally, but quite a few other tech stocks saw very nice gains as well. In fact, many of those “other” tech stocks have broken to new highs...while only one FAANG stock did the same thing. Therefore, a lot less of the momentum money in the market place right now will go into the FAANGs...and more will go into those other tech names. Therefore, we think some “rotation” WITHIN the tech sector will be a good idea for the rest of this year.

4) The most important market to watch next week is going to be the currency market. Three different currencies are testing very important support or resistance levels...the dollar, the euro and the Aussi dollar. If they break their respective key technical levels, it will have important implications for several different asset classes...including the U.S. stock market.

5) Despite the midweek drop in long-term yields, the recent upward trajectory in those yields is still intact. If they continue to keep rising, it should be bullish for the bank stocks. In fact, we’re watching the $35 level on the KBE. If that is broken to the upside, it will be very bullish for the group on a technical basis. (We’re watching the $104 level on JPM for the same reason.)

6) Although the healthcare sector declined just before the election, it was really only falling along with the broad market. In other words, despite concerns about what a blue wave might do to the group, it acted quite well in the months leading to last week’s election. Now that it looks like we’ll have a divided government, it should help will the group fundamentally....It also looks great on a technical basis. If the XLV & IBB can see some upside follow-through anytime soon, it’s going to be very bullish for the sector on a technical basis as well.

7) Our bullish call on Bitcoin when it broke above 12,000 worked out very well...with an almost immediate 20% rally. However, we turned skeptical too early (when it move above 14,000). However, we’re not going to jump back on the bandwagon at these levels. There is just no question in our minds that Bitcoin is becoming quite overbought...with its daily RSI chart above 83...and its weekly RSI chart very near 80. We wouldn’t chase it up here.

8) Those who believe that a Biden victory will mean a substantial easing of tensions between the U.S. and China are out of their minds!!!! Sure, the “trade tensions” should ease, but that’s not the real issue between these two countries. The real issue is Taiwan! The tensions for this issue continued to rise last week...and if China continues on its current path vis-à-vis Taiwan going forward, a change in President will not change this situation.

9) The next Republican Nominee for President will likely be Governor Greg Abbott of Texas. This prediction is based solely on math (although we do admit that we like the Governor). Texas has become a purple state...and is likely become more of one in 2024. With California, NY & Illinois solidly blue, the GOP cannot afford to lose Texas in 2024. The best way to keep Texas in the GOP’s column at a time when the state as a whole is turning purple...is to nominate one of its favorite sons. (Without Texas, the GOP will have zero chance of winning the presidency in 2024.)

10) Summary of our current stance......We believe that things like post election euphoria, performance fear by institutional investors, and especially Fed liquidity will fuel a year-end rally. However, we believe next year will be a tougher year. Rebounding to pre-pandemic levels of growth will not be enough to take this expensive stock market much higher in the New Year. Therefore, while investors are enjoying the late-year rally, they should also be preparing a plan...to change their portfolios late this year and (especially) early next year...for tougher year in 2021...........Finally, THANK YOU VETERANS!!!!

Long Version:

1) One of the things that we have we always have to guard against is to avoid getting sucked-in by a big short-term move in the market. We did expect the market to rally this past week after the previous week’s sell-off...and we suggested that investors should start nibbling on the buyside as we moved into this past week. However, we readily admit that we did not expect that this week’s advance would be anywhere near as strong as it turned out to be...and we were not so sure it would last through the entire week.

In other words, when the market rallies as strongly as it did last week, we are usually very careful about jumping on the band wagon...because that kind of move can sometimes be exactly the wrong thing to do...at exactly the wrong time. However, we are not as skeptical right now as we sometimes are after a sharp short-term decline. Sure we could easily see the stock market take a near-term “breather” at some point very soon, but we are not changing our call for a nice rally into the end of the year...for the reasons we will discuss below. A short-term “breather” after a more than 7% rally over just four days would be normal and healthy...so it’s not something that should worry investors if we see that early next week.

Therefore, investors should use a short-term “breather” (or any actual weakness)...to continue to add to their positions in their favorite names. (In the rest of this bullet point, we’d like to give you a rapid fire list of reasons why we think the market will rally further into the end of the year...after we see a probable short-term “breather.”)

---The market usually rallies over the last 6-7 weeks of a Presidential election year...no matter what the fundamental back-drop might be at that time. This might sound crazy, but overall sentiment (among investors and other members of the public alike) becomes much more positive right after an election. It’s just human nature. (Rather, we should probably say that is the nature of the American psyche.).........You won’t find this in any textbooks, but history DOES tell us that the market usually rallies at the end of election years.

---Whenever we get a year-end rally (in any year), it tends to feed on itself...due to the impact of institutional investors. At the end of every year, ALL institutional investors become focused on the short-term (no matter what they say publicly). Their year-end bonus (and sometimes their jobs) depend on the full year performance. If the market is running higher at the end of the year, the institutional investors who are behind HAVE to do whatever it takes to play catch-up. Similarly, even those who are ahead of the market NEED to keep buying. They want to STAY ahead of it (to insure a nice big fat bonus), so they always keep buying as well. Therefore, even if these people think the next year is going to be an economic disaster, they’re going to be buying in December...if the market is rallying strongly!

---Now-a-days...as those institutional investors keep buying, the aglos kick-in and push the market higher still. That gets individual investors to get more aggressive...and the whole thing feeds on itself.

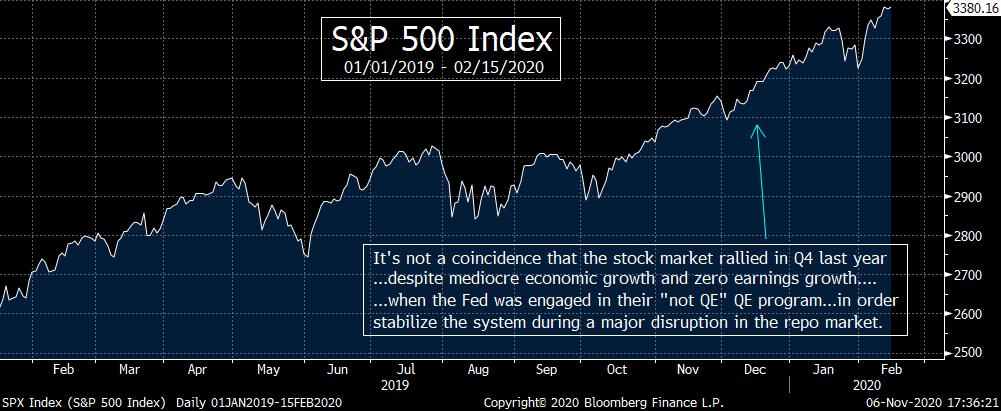

---Finally...and most importantly...this “feeding frenzy” can be particularly strong when the Fed is providing liquidity. (People forget that much of last year’s strong 4th quarter rally was fueled by Fed liquidity. That’s right. They were providing plenty of it last year with their “not QE” QE program! Remember, we had just gone through a crisis in the repo market at the end of Q3 last year...and the Fed provided extra liquidity throughout the 4th quarter...and into the New Year...to keep that repo market stable.) With another wave of the coronavirus just beginning, the Fed’s current stimulus program isn’t going to shrink. In fact, liquidity should remain plentiful for the rest of the year...in order to insure that the credit markets are not disrupted by any renewed lockdowns.

Given what we have said above, we think the year-end rally could surprise people to the upside...just like it did last year.

2) It’s funny, with all of this focus on the election, the state of the economy got lost in the sauce last week. Therefore, we’d like to cover that issue this weekend........Very simply, we are not particularly bullish on the economy for 2021. You might think that this should make us bearish for the stock market over the last two months of the year. However, after over 30 years working on Wall Street for some of the most dynamic trading desks in the business, we have learned that the market can frequently move in a different direction than the underlying economy (and a different direction than the future prospects for the economy)...for extended periods of time. That’s why were still looking for a year-end rally.

Don’t get us wrong, we’re NOT calling for a deep drop in economy growth. It should definitely grow nicely compared to the pandemic-influenced economy of 2020. However, we’re not convinced that it will rebound back to the pre-pandemic levels. More importantly, even if it does, the stock market is already pricing-in an economy that is growing at those 2019 levels (and then some)! This is why we’re not very excited about the stock market in 2021...even though we’re looking for a nice year-end rally over the next two months.

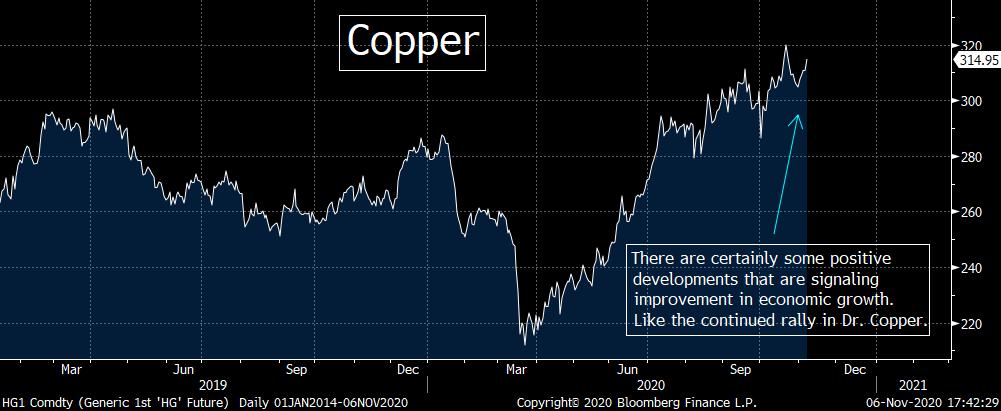

Before we talk about our concerns about economic growth, we do need to admit that there are certainly some signs that the economy is improving. First of all, Friday’s employment report was stronger than expected...with a higher non-farm payroll number and a lower unemployment rate than the consensus was looking for. We’ve also seen a nice rise in “Dr. Copper” to it’s a level that is very close to its highest level since 2018...and last week’s ISM manufacturing data came in much better than expected.

However, as we stated last weekend (and in many other pieces recently), we are quite concerned about what the economy will do next year. First of all, we have to remember that we were still going through the worst recovery in the post WWII era before the pandemic knocked the snot out of the global economy. So if next year’s economy is much better than 2020...or even if it is as strong as it was just before the pandemic shut things down...it will NOT make it a great economy. Let’s face it, the NY Yankees were a much better team this year, but they still didn’t get very far in the playoffs! We think the economy in 2021 will look a lot like the Yankees of 2020. It will be good, but not enough to take it far in the playoffs. (In other words, it won’t be strong enough to justify the levels that are at or near current levels in the broad averages.)

Second, new presidents tend to back-end load their new simulative policies...so that they can get re-elected four years from now. We went into this issue extensively last weekend, so we won’t delve too far into it again this weekend. However we DO want to add one component to the argument. The odds are pretty good that Mr. Biden will create lockdowns that are more restrictive than President Trump’s once he is inaugurated (assuming the experts are right and the former VP does indeed win). This does not mean that he’s going to engage in a serious country wide lockdown, but there is no question that countries that HAVE been more serious about their lockdowns have done much better than the U.S. with the pandemic.

Think about it. Any economic slow-down that might come from a more strenuous lockdown policy will be blamed on President Trump! Besides, when people are voting four years from now, they won’t remember the any slowdown from 2021! How many people remembered the recessions of 1981/82 or 1992/93...when Reagan ran for re-election in 1984 and Clinton ran for re-election in 1996???

We could be dead wrong. The pandemic just might settle down in a major way by the time Inauguration Day comes around. However, as we said above, it will be difficult to justify a stock market in the 3,500-3,800 range based on an economy that is only as strong was it was in 2019. The market is just too expensive for that to take place. (Besides, if the pandemic has died down in a major way by Inauguration Day, those on the far right are going to go crazy with their conspiracy theories. That won’t impact the markets, but it will be fun to watch! Fox News will see another huge ratings boost!!!)

3) With the strong rally in the mega-cap tech stocks this past week, the debate has been renewed about whether investors should be sticking with the growth stocks...or should be rotating in to the value names. We believe that investors should indeed be “rotating” SOME (not all) of their exposure away the mega-cap tech/FAANG names and into value, BUT we want to reiterate our belief that they should also be “rotating” WITHIN the tech sector.

We have to separate the difference between a great company and a great stock sometimes. Through much of the past two years, the FAANGs have been BOTH great companies AND great stocks. However, even though they all remain great companies, they’re stocks have not been as great since their early September highs.

Given that they are still great companies, investors do not want to dump the entire exposure to them. Instead, we believe investors should pare-back the size of their holdings of each of these names. However, they definitely should consider lightening up on their exposure...especially on bounces over the rest of this year.

Even though most of these stocks are off of their highs, they’re still quite expensive. During the first round of lockdowns...when we had no idea how long the lockdowns would last...investors didn’t worry about these valuations. However, now that people are more confident that any new round of lockdowns will likely be the final lockdowns, they’re going to be a bit more careful about paying some lofty valuations. In other words, stocks are forward looking...and if the “stay at home” play is going to fade for good as the weather gets warmer this spring...these names will lose some of their allure. (We would all agree that AMZN is not solely a stay at home stock by any means, but this issue HAS given investors a willingness to ignore its lofty valuation...and that they might not be willing to do that going forward...as vaccines and treatments improve.)

HOWEVER, even though we think that investors should rotate SOME of their FAANG holdings towards value names, we do not believe that all of that money should be taken out of the broad technology sector. Instead, they should ALSO consider rotating WITHIN the broad tech sector! The chip sector still looks strong...and we believe that the Cloud Computing revolution is in the early innings. So some of that money should go into those names.

One name that looks VERY enticing on a technical basis in Micron (MU). While most of tech was rallying strongly in August, MU got hit hard. However, it has bounced-back very strongly and it is now testing its highs from both June & July. Therefore, if it can break above the $55 level in any meaningful way, it’s going to give the stock a very important “higher-high”...AND break it out of an “ascending triangle” pattern. That will attract A LOT of momentum money to the stock...and give it a very strong year-end rally.

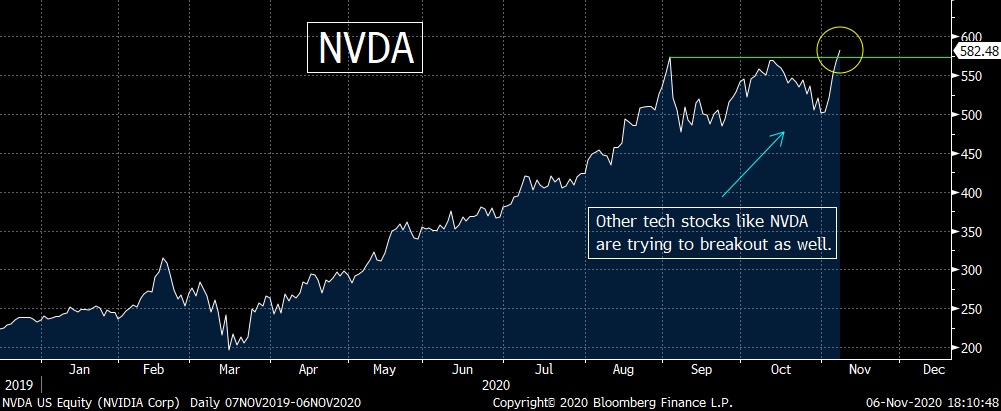

We’d also note that stocks like NVDA, TXN, AMD, TSM and the SMH semi ETF all saw nice breakouts late last week. Some of them are only slight breakouts so far, so they’ll need to see more upside follow-through to confirm their breakouts. However, in the FAANG stocks, only GOGGL is breaking out to new highs. So they don’t have the same kind of technical momentum than quite a few stocks that are not in that FAANG group. This does not mean that the FAANG names cannot rally further in a year-end rally. However, with other tech stocks making new highs while most of the FAANGs are not...and with the “momentum-driven” strategies becoming so prevalent recently...we believe that a lot of that momentum money no longer go solely into those small number of FAANG names. Instead, it will be more spread out. In fact, we think more of that money will likely go the names that are actually breaking to new all-time highs...something most FAANG stocks are not doing right now.

4) The most important market to watch next week is going to be the currency market. Three different currencies are testing very important support or resistance levels...the dollar, the euro and the Aussi dollar. If they break their respective key technical levels, it will have important implications for several different asset classes...including the U.S. stock market.

We’ll begin with the DXY dollar index. I was very, very weak following Election Day this past week...and it is now testing the KEY support level we’ve been harping on for some time: the 2020 lows of 92.00. Any meaningful break below that level will be very bearish for the dollar...and that will be bullish for U.S. stocks, emerging markets and commodities.

That said, we continue to believe that the dollar will hold that key level. The net short positions are still quite large in the COT data...and they almost certainly grew at the end of last week. (The COT data measures the positions from Tuesday to Tuesday...and then publish the data on Friday.) However, we have to guard about being stubborn, so if the DXY breaks below 92 and holds below that level it will be a definitive bearish signal for the greenback. (First chart below.)

The euro is the mirror image of the dollar. It is very close to its 2020 highs, so any meaningful break above that level will be very bullish for the euro on a technical basis. However, the COT data is also the mirror image of the dollar...with the net long positions very large (and they almost certainly grew over the last few days of last week as well). (Second chart below.)

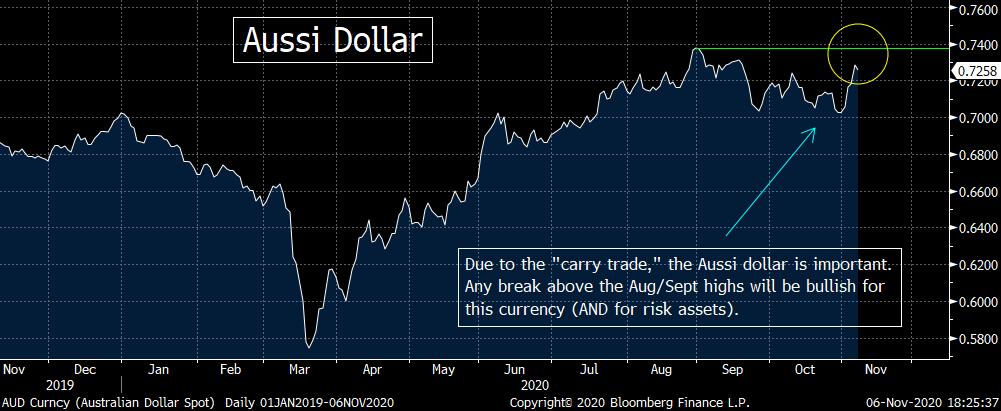

Finally, the Aussi dollar...which is important indicator for liquidity in the system due to the carry trade...is not far from its early September highs. Given how closely correlated the AUD and the stock market has been this year, there’s no surprise that the high for the AUD came at the exact same time as the S&P topped out in late August/early September (and bottomed at exactly the same time back in March). Therefore, if the AUD breaks above the 0.74 level in any material way, it’s going to be bullish for the U.S. stock market. (Third chart below.)

We’ll finish by saying that the currency markets will be something to watch very closely well past next week as well. These currencies might not break their key technical levels this coming week. However, that does not mean that they won’t break those levels at some later date. In fact, we think it is very likely that the dollar will indeed break-down again...once its extreme in positioning is worked-off...probably late this year or early next year.

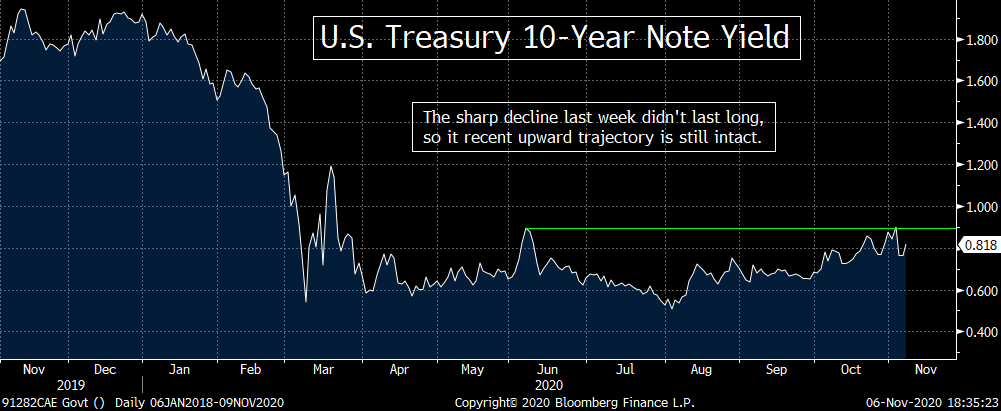

5) A lot was made of the huge decline in long-term bond yields right after the election this past week...as the yield on the 10yr note fell from 0.0% to 0.76% mid-week. However, those yields saw a sharp bounce on Friday...and finished the week at 0.82%. So the upward bias in long-term yields we’ve been seeing recently remains intact. Yes, it can be argued that the rise in the odds that the Democrats might still win the Senate had an impact on Friday, but the stronger than expected employment data...AND the extreme positioning in that asset...played a role as well in our opinion. Given that the Senate will likely not be settled until January, these other issues could easily cause the 10yr yield move back up and test that all-important 0.9% resistance level once again before long.

If (repeat, IF) that does indeed take place...and long-term rates creep higher, we’ll be watching the 35 level on the KBE bank ETF like a hawk. That was the high for the KBE in August, October and again this past week. Therefore, any break above that level will give take it out of the sideways range it has been in since late June...which will be very bullish for the bank group.

We like to highlight this because there is no better way for investors to play catch-up at the end of the year than to jump on board a group that has been lagging for a long time. Therefore, if the momentum gets going with a break of that 35 level in the KBE, its upside momentum into the end of the year could surprise everybody.

We’ll finish this bullet point by highlighting one of the most high profile stocks in the banks sector, JPM. Like the 35 level for the KBE, $104 has been very tough resistance for JPM for many months. Therefore, if it can break above that level in any significant way over the coming days or weeks, it’s going to be very bullish for this all-important stock in the banking sector.

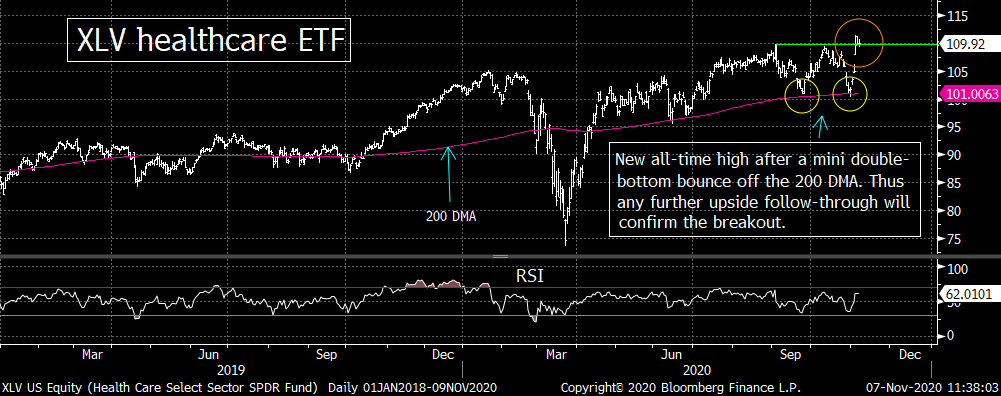

6) Even though there was a lot of talk about the concerns investors had about a Biden victory and/or a possible “blue wave,” the healthcare stocks acted quite well before the election......Yes, the XLV healthcare ETF and the IBB biotech ETF both sold-off just before the election...but so did the rest of the stock market. In other words, their weakness only came immediately before the election...it was not a multi-week/month decline. Also, the sector fell in the week before the election due to a broad market decline, not a group-specific move.

The fact of the matter is that the action in both of these ETFs before that very-late October decline was quite good. In fact both of these ETFs were trading very near to their all-time highs in mid-October. Thus it’s incorrect to say that investors were overly worried about this sector if there was a blue wave...even though many of them were talking about this sector in a cautious way.

Of course, it does not look like we’re going to get a blue wave. The GOP looks like they’re going to hold the Senate (although that is certainly not a lock quite yet). Therefore, a divided government over the next two years should provide a much more positive fundamental backdrop for the healthcare and biotech stocks than people were thinking just a week ago. However, after last week’s rally in the broad market...which included a nice rally in the XLV and the IBB as well...it has ALSO left this sector in FABULOUS shape on a technical basis as well!

Let’s look at the chart on the XLV first. The 8% jump in this ETF took it to a new all-time high! We do need to point out that it was only a very mild new high, so it’s going to have to see more upside follow-through to confirm the breakout. However, we’d also note that the XLV was able to bounce off its 200 DMA a second time at the very beginning of the month. That gave it a nice “double-bottom”...so if it can indeed see more upside follow-through any time over the coming days and weeks, this group is going run, run, run...until her daddy takes the T-bird away. (No worries if you’re too young to be familiar with that line from an old song. It just means it’s going to rally a lot!)

As for the IBB, it bounced off of its 200 DMA for a second time recently as well. However, since the 200 DMA is not flat like it is with the XLV, the IBB did not make a “double-bottom.” That said, it’s recent bounce is still taking it up to a key resistance level. The chart could be seen as an “ascending triangle,” but we think it would be better labeled as a “symmetrical triangle.” It did pull-back from the top line of that pattern on Friday. However, if it can bounce-back...and take out that line any time soon, it’s going to be positive. If it goes one step further...and breaks meaningfully above its all-time highs from July (which is less than 2% above that first resistance line), it will confirm the breakout for the IBB. Needless to say, THAT will be very bullish for this sub-sector of the healthcare group.

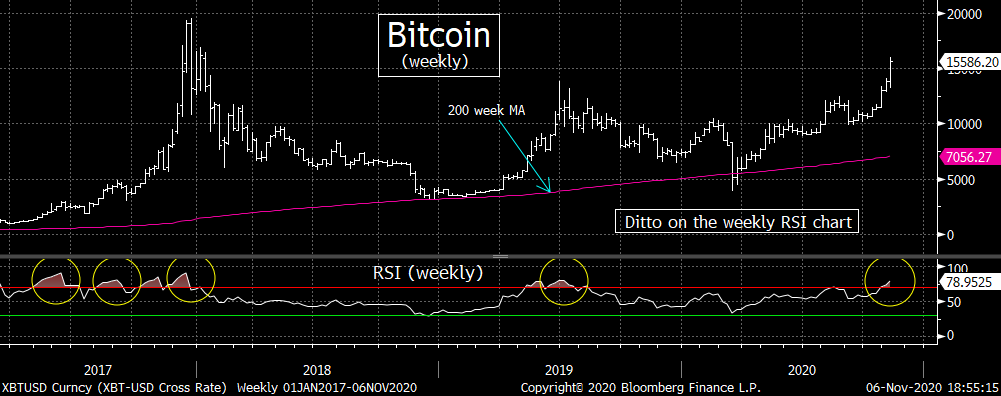

7) Bitcoin had another good week. In fact, its action at the end of the week was spectacular. We turned bullish on this asset class again when it broke above 12,000, but we also said that it should not be chased above 14,000. In other words, it was great that we captured the 20% rally that took place over a very short time frame, we readily admit that we did turn skeptical too early.

The question is whether we should shift our stance and turn bullish once again...or should we remain skeptical/cautious up at these levels. Well, there are certainly reasons to think that this cryptocurrency will rally further. At the top of the list the fact that we’re not going to know who wins the two senate seats from Georgia until January...thus we probably won’t know who will control the Senate in the next congress until then.

However, there is not question that Bitcoin is becoming quite overbought. In fact, both its daily RSI and its weekly RSI charts are reaching levels that have been followed by pull-backs in Bitcoing over the past years. The RSI on the daily chart is now above 83...and it’s very close to 80 on its weekly RSI chart.

We do admit that both of those RSI charts have become even more overbought than they are right now a couple of times before they have topped out in the last two years, but not much more overbought. So although Bitcoin could reach 16,000 before it rolls over, we still think that chasing Bitcoin up at these levels could pose problems before long...especially for short-term and intermediate-term traders. With this in mind, we would look to buy this asset class after a decline from current prices. We wouldn’t chase it up here.

8) Those who believe that a Biden victory will mean a substantial easing of tensions between the U.S. and China are out of their minds!!!! Sure, the trade tensions should ease, but that’s not the real issue between these two countries. The real issue is Taiwan!

You might be getting tired of hearing me harp on this issue, but I think it is ESSENTIAL to keep repeating it again and again. The situation keeps escalating. This past week, China said that they are not ruling out a stern response to the U.S. sales of drones to Taiwan. China said that the situation “seriously undermines China’s sovereignty and security interests”...and that China will take “legitimate and necessary reactions to firmly safeguard their national sovereignty and security interests.”

These newest provocative comments from China are on top of the other comments and actions we have highlighted on many occasions in our weekend piece over the past six months. However, we just want to add that China continues to breach the Taiwan Straights median line. In fact, they have done it on 25 separate days during the month of October.

Mr. Biden can do whatever he wants on the trade issue, but if he comes across as weak on this issue, his presidency will be doomed from the start. For all practical purposes, China has already taken full control of Hong Kong. However, the people of Taiwan are not going to give-in anywhere as easily. They are preparing to defend any military action from China in a very, very serious manner. So even if the U.S. and others do not help them, there will be a military conflict if China tries move on Taiwan.

Now that Intel (INTC) has stopped producing chips, Taiwan is the focal point for chip production for the world. Therefore, if it falls into China’s hands, it will put the U.S. and Europe at a tremendous disadvantage. We do not think it is too much to say that access to the major producer of chips in the world right now is very comparable to Japan’s need to access to oil in the 1940s. The only (big) difference is that the U.S. wants chips for (mostly) peaceful reasons and Japan wanted the oil to expand their empire.

We still believe that Taiwan could easily become the dominant issue of this decade...and we believe a Biden Administration will be ready to take it on. They will not bend over to China like the U.S. and others did did on Hong Kong. Theref

Recent free content from Matt Maley

-

THE WEEKLY TOP 10

— 10/23/22

THE WEEKLY TOP 10

— 10/23/22

-

Morning Comment: Can the Treasury market actually give the stock market some relief soon?

— 10/21/22

-

What Do 2022 and 1987 Have in Common?

— 10/19/22

-

Morning Comment: Which is it? Is stimulus bullish or bearish for the stock market?

— 10/17/22

-

Morning Comment: Peak Inflation is Becoming a Process Instead of a Turning Point

— 10/13/22

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464