Avoid the Crowds - March 16, 2016

Click Here for this Week's Letter

Greetings,

It seems like the best strategy for 2016 is to simply avoid crowded trades. Since July, Russell 3000 companies in which hedge funds have the highest ownership percentage have plunged -31%, compared with a -2.8% decline in the S&P 500. The same can be said of FX markets where long USD positions have backfired against JPY and EUR even as the BoJ and ECB ease policy while the Fed talks tightening.

EUR posted a 3.6% intraday swing last Thursday after Mario Draghi seemed to acknowledge that negative rates are a bad idea. And it seems the Japanese have come to the same conclusion. BoJ officials have been scurrying to commercial banks to explain and apologize for their surprise adoption of negative interest rates in January, while Prime Minister Shinzo Abe is distancing himself from a decision that is proving unpopular with the public.

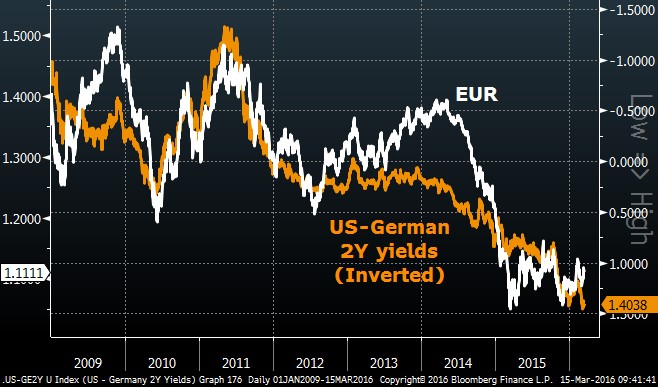

Taking negative rates off the table (for now) pushed 2-year German yields up +9bps on Thursday, the biggest spike since December 3 (+14bps) – the last time the ECB eased policy. These bonds ended December 3 yielding -0.30% and even after Thursday’s spike they’re now offering -0.45%. Long German bonds is a crowded trade and everyone gets spooked after catalysts, but the trend is still clearly higher.

2-year US Treasury yields have also climbed of late, and continue to rise relentlessly relative to German debt. It hard to imagine that trend changing with the expansion of QECB, TLTRO and other various acronyms from the ECB. From the other side, the Fed is surely more confident in its ability to resume hiking later this year with the stock market and economic data rebounding. The market is now pricing in a 53% chance the Fed pulls the trigger and moves rates higher in June. Short EUR was a very crowded trade and a solid chunk of those positions have now been covered, but rate differentials still suggest EUR should trade closer to 1.05 vs. USD.

These are all examples of crowded trades that have already reversed. But there’s a monster position in the market that almost no one is talking about: short 10Y US Treasury’s. Positions are so skewed to the downside that traders are willing to pay to lend cash to get their hands on the issue. The number of reported “failed trades” has spiked and the repo rate is -3%, equal to a “fails charge.” For those who are unfamiliar, a "Delivery Failure" occurs when one party fails to deliver a Treasury by the date previously agreed by both parties. The -3% repo rate means there is an unprecedented amount of shorts who would rather pay the fails charge than to cover their positions.

The rebound in stocks and data warrants higher Treasury yields, but there’s a decent chance this is just a bounce. If and when the data turns, or the Fed hikes prematurely (flattening the yield curve), this short 10Y position could unwind in a hurry. And, as we’ve learned in every other market this year, it’s best to stay away from the crowds.

With that I give you this week's letter:

March 16, 2016

The Cup & Handle Fund is up around +2.0% YTD, and +11.0% Y/Y. We’ve given back a chunk of our YTD gains, but our level of concern is not very high. I suspect we’ll see another bout of turbulence before July and that’s when we’ll shoot for a big score. In the meantime, we’re building positions and trying to capitalize on this buying opportunity in volatility. Our outlook is still bearish but these bounces can last several months, so we’ll keep doing our best to be patient. If you’d like to start receiving these letters click here.

As always, if you have any questions or comments or just want to vent, please send me an email at mike@cup-handle.com.

Until next time, tread lightly out there,

Michael Lingenheld

Managing Editor – Cup & Handle Macro

Recent free content from Michael Lingenheld

-

The Finale - April 21, 2016

— 4/20/16

The Finale - April 21, 2016

— 4/20/16

-

The Spring Freeze - April 6, 2016

— 4/05/16

-

Dependent on Friday's Data - March 30, 2016

— 3/29/16

-

Money For Less Than Nothing - March 23, 2016

— 3/22/16

-

The Fundamental Bounce - March 9, 2016

— 3/08/16

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464