Investor Hell, Charles Bukowski and Low Hanging Fruit

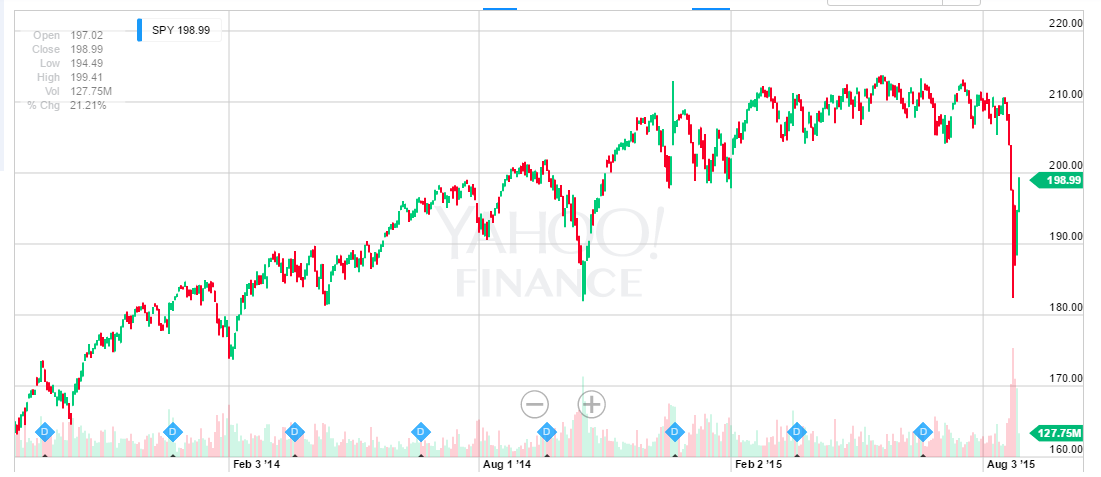

It appears the market panic of 2015 has come to an end. All is well, China is growing, they no longer need to buy stocks to prop up their broken market, oil has stabilized and the Saudis are going to reduce production to stop the carnage. That is not the case of course but the stock market sure seems to think so. It has been an interesting week but I may slap the next person who calls it a crash. It as a dip, a 3 day correction of sort but it’s a long way from a crash. Take a look at a market chart:

Looks horrible doesn’t it? But wait theres more:

A decent little decline to be sure but short lived. This is what a crash looks like for future reference:

This week was nothing to close to that. Nor did we create any great bargains. As I pointed out on Real Money today the market still trades at 19 times trialing earnings. The Schiller PE is over 23 and the market cap to GDP ratio is above 112 so the market is not cheap , although it si a bit more volatile than it has been in some time now. No significant new opportunities were created. It was more a betting opportunity than a buying opportunity. We bought a little more of stocks we like a lot and added a closed end energy fund at a discount to NAV but mostly this week has been much like the weeks prior. I screened, I read 10q filings, tracked insiders, read a bunch of 13Ds and Gs, walked the dog a lot and snuck in some baseball and books. I would have loved for this to have turned into a genuine inventory creation event buy alas it did not.

Our little banks never got the memo about volatility. They are basically flat on the week and up for the month. For the most part they do not react to short term market movements. The stocks tend to be in strong hands and are the least thing to be sold in a bad market. You will never meet a margin call by trying to sell 1000 shares of First Bank of Middle of Nowhere that last traded a week ago and is currently 18 bid and 21 offered for 100 shares a side. It is yet another reason I love the sector so much. They are hard to buy and harder to sell and very few people have the ability to invest with the required time frame. Investors seem to crave liquidity like junkies crave smack and it has about the same impact on long term gains as it junk does long term health.

One hallmark of the week for me was all the very confident predictions about where and what the market was going to do. Prices were going to bounce off this line or break out of this flag pattern. We were going to crash. We would rally sharply off the lows. Interestingly all of them were right and all of them were wrong at some point during the week. It is just the latest reaffirmation of Charles Bukowski’s claim that ““The problem with the world is that the intelligent people are full of doubts, while the stupid ones are full of confidence.” I have little doubt that a ton of money was lost on both sides of the market by undercapitalized trader who had too much confidence and too much leverage as the week developed.

I continue to think that most investors are better off approaching the financial market as investors in businesses and not traders of stocks. Buying a good business at a decent price and owning for years should prove much greater financial rewards that attempting to time the move so something as psychopathically schizophrenic as the stock market. Owning small banks that have to either find a way to grow or sell the bank due to regulatory conditions is almost arbitrage like when you can buy them for less than 90% of book value and the average takeover multiple is 1.25 or higher and a far better use of time and money than guessing where the market might close today or tomorrow.

I have no idea where markets will go today or tomorrow. I would love to see them fall but I am not sure they can while interest rates are this low. As a good friend recently suggested the broader stock market is a positive carry trade with rates at this level and will be until rates rise. A serious decline is going to require a serious catalyst or a rate increase. While geopolitical catalysts cannot be predicted I see no indication that there is enough economic strength to justify sustained interest rate increases. We are stuck in a special version of one of James Montiers investment hells and there is very little to do outside of the community bank space.

Therefore that’s where we continue to put most of our focus. I turn over the rocks looking for buyable situations but the layups and low hanging fruit and primarily in small banks that trade below book value and have activists involved. This will continue to be the most boring source of exciting profit for a long time to come.

It should be an interesting fall if the markets stay this volatile. We also have the fall publishers catalog to look forward to as well as pennant baseball and the return of football to keep us occupied until we get a real banking opportunity.

Have a great week

Tim

Right now searching for value is like https://www.youtube.com/watch?v=a9Bs4xhDyxw but thanks to small banks at least we are enjoying the ride

Recent free content from Tim Melvin

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464